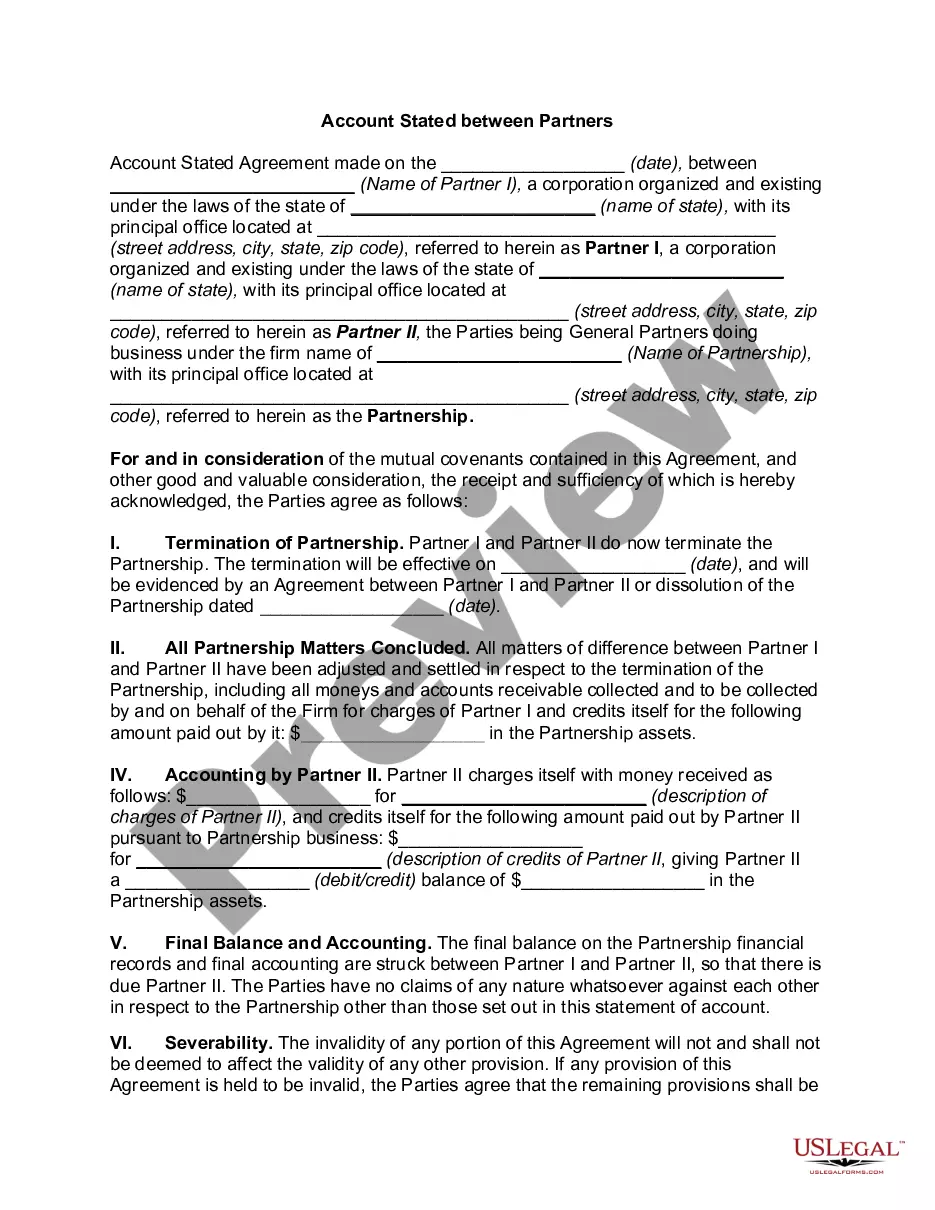

New Jersey Account Stated Between Partners and Termination of Partnership

Description

How to fill out Account Stated Between Partners And Termination Of Partnership?

US Legal Forms - one of many largest libraries of lawful varieties in America - gives a wide range of lawful record layouts it is possible to download or print out. Making use of the site, you can get thousands of varieties for enterprise and individual uses, categorized by classes, says, or key phrases.You will discover the newest models of varieties like the New Jersey Account Stated Between Partners and Termination of Partnership in seconds.

If you currently have a monthly subscription, log in and download New Jersey Account Stated Between Partners and Termination of Partnership through the US Legal Forms catalogue. The Acquire option will show up on each and every form you look at. You get access to all earlier acquired varieties from the My Forms tab of the account.

If you want to use US Legal Forms the very first time, here are easy directions to help you began:

- Be sure you have picked the proper form for your town/state. Select the Preview option to analyze the form`s content. Read the form description to ensure that you have selected the right form.

- In case the form doesn`t match your demands, utilize the Look for discipline near the top of the monitor to obtain the one which does.

- In case you are happy with the form, verify your decision by clicking on the Buy now option. Then, select the rates program you prefer and supply your accreditations to register for the account.

- Process the purchase. Make use of your Visa or Mastercard or PayPal account to complete the purchase.

- Pick the format and download the form on the system.

- Make adjustments. Fill out, modify and print out and sign the acquired New Jersey Account Stated Between Partners and Termination of Partnership.

Every single template you added to your bank account lacks an expiry time which is the one you have permanently. So, in order to download or print out an additional backup, just check out the My Forms segment and click on on the form you will need.

Obtain access to the New Jersey Account Stated Between Partners and Termination of Partnership with US Legal Forms, one of the most comprehensive catalogue of lawful record layouts. Use thousands of professional and status-particular layouts that meet your company or individual needs and demands.

Form popularity

FAQ

A Certificate of Cancellation must be signed by all General Partners. List the name as it appears on the records of the State Treasurer. Provide the 10-digit business entity identification number issued by the State of New Jersey. Enter the date of formation or authorization in New Jersey.

Your LLC must file an IRS Form 1065 and a New Jersey Partnership Return (Form NJ-1065). LLC taxed as a Corporation: Yes. Your LLC must file tax returns with the IRS and the New Jersey Division of Taxation to pay your New Jersey income tax. Check with your accountant to make sure you file all the correct documents.

A partnership must file even if its principal place of busi- ness is outside the State of New Jersey. The NJ-1065 is not solely an information return. A filing fee and tax may be imposed on the partnership. Partners subject to the Gross Income Tax must report and pay tax on their share of partnership income or loss.

FILING FEE EXCEPTIONS: No New Jersey source income. To qualify for this exception, all operations and facilities must be located outside New Jersey. Generally, if the partnership has New Jersey source expenses, deductions or losses, it will not qualify for this exception.

All domestic business partnerships headquartered in the United States must file Form 1065 each year, including general partnerships, limited partnerships, and limited liability companies (LLCs) classified as partnerships with at least two members.

For taxpayers with Entire Net Income greater than $100,000, the tax rate is 9% (. 09) on adjusted entire net income or such portion thereof as may be allocable to New Jersey. For taxpayers with Entire Net Income greater than $50,000 and less than or equal to $100,000, the tax rate is 7.5% (.

Amounts entered on this line will automatically flow to an Unrecaptured Section 1250 Gain Worksheet and then to Schedule D (Form 1040), Line 19. Line 10 - Net Gain/Loss under Section 1231 - Enter the amount reported in Box 10 of the K-1.

Every partnership that has income or loss derived from sources in the State of New Jersey, or has any type of New Jersey resident partner, must file Form NJ-1065. Form NJ-CBT-1065 must be filed when the entity is re- quired to calculate a tax on its nonresident partner(s).