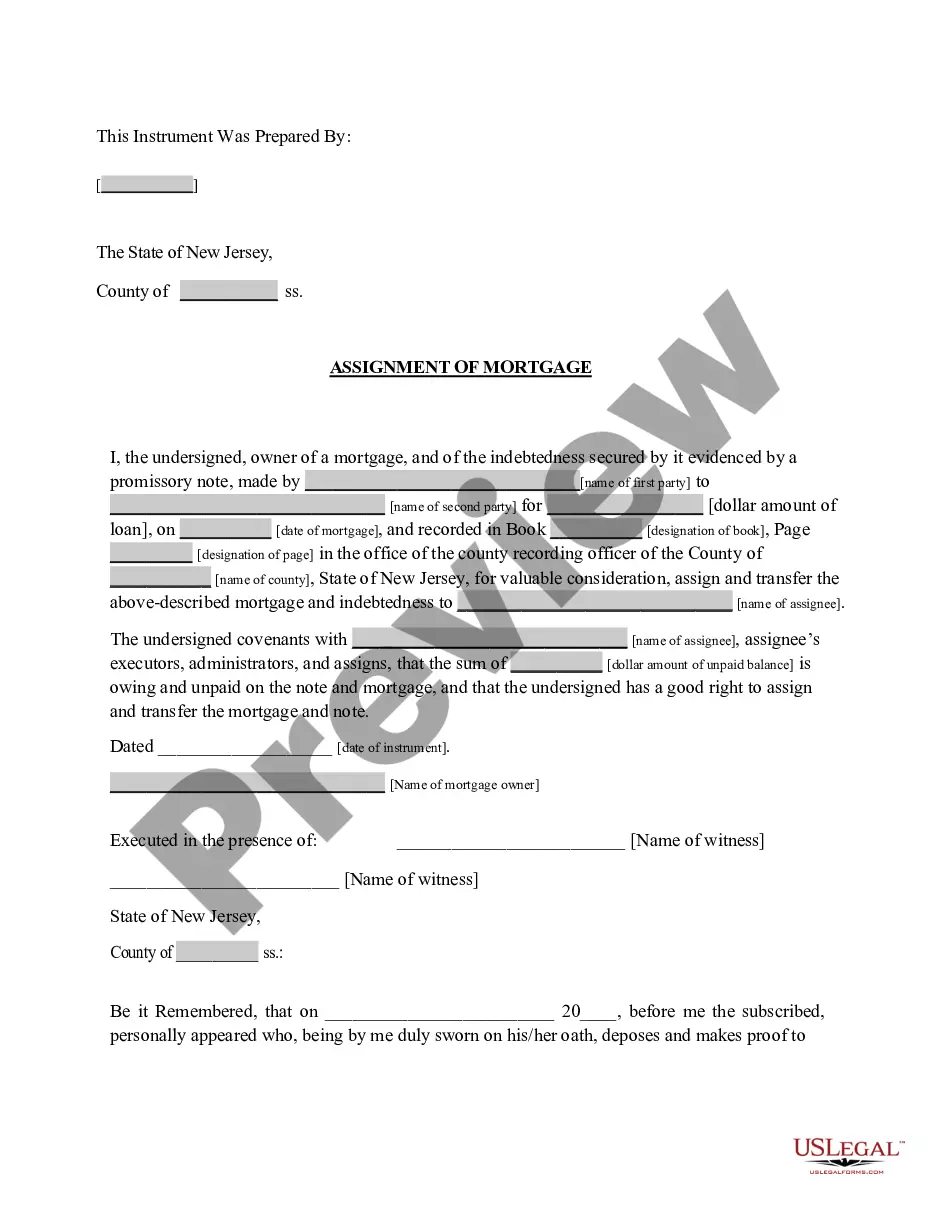

New Jersey Assignment of Mortgage is a legal document that is used to transfer a mortgage from one lender to another. This process is used to facilitate the sale of a mortgage from the original lender to another lender. The new lender then becomes the new owner of the mortgage and is responsible for collecting payments from the borrower. There are two types of New Jersey Assignment of Mortgage: voluntary assignment and involuntary assignment. A voluntary assignment is when the mortgagee (original lender) willingly transfers the mortgage to a new lender. An involuntary assignment is when the mortgagee is forced to transfer the mortgage due to a default on the loan by the borrower. The New Jersey Assignment of Mortgage must contain the names of both the original lender and the new lender, the date of the assignment, and the address of the mortgaged property. A notarized signature from both parties is also required for the document to be valid.

New Jersey Assignment of Mortgage

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out New Jersey Assignment Of Mortgage?

How much time and resources do you often spend on drafting formal documentation? There’s a greater way to get such forms than hiring legal experts or spending hours browsing the web for a proper blank. US Legal Forms is the premier online library that offers professionally drafted and verified state-specific legal documents for any purpose, including the New Jersey Assignment of Mortgage.

To obtain and complete an appropriate New Jersey Assignment of Mortgage blank, follow these simple steps:

- Examine the form content to ensure it complies with your state regulations. To do so, check the form description or take advantage of the Preview option.

- If your legal template doesn’t meet your requirements, locate another one using the search tab at the top of the page.

- If you are already registered with our service, log in and download the New Jersey Assignment of Mortgage. Otherwise, proceed to the next steps.

- Click Buy now once you find the correct blank. Select the subscription plan that suits you best to access our library’s full service.

- Register for an account and pay for your subscription. You can make a payment with your credit card or through PayPal - our service is totally reliable for that.

- Download your New Jersey Assignment of Mortgage on your device and fill it out on a printed-out hard copy or electronically.

Another advantage of our service is that you can access previously purchased documents that you securely keep in your profile in the My Forms tab. Get them at any moment and re-complete your paperwork as often as you need.

Save time and effort preparing legal paperwork with US Legal Forms, one of the most trusted web services. Sign up for us now!

Form popularity

FAQ

Once a loan has been assigned to MERS, it can be bought and sold any number of times later without recording assignments. Don't be surprised if you find out that your mortgage was assigned to MERS at some point. In most cases, the loan will have to be assigned out of MERS' name before a foreclosure can begin.

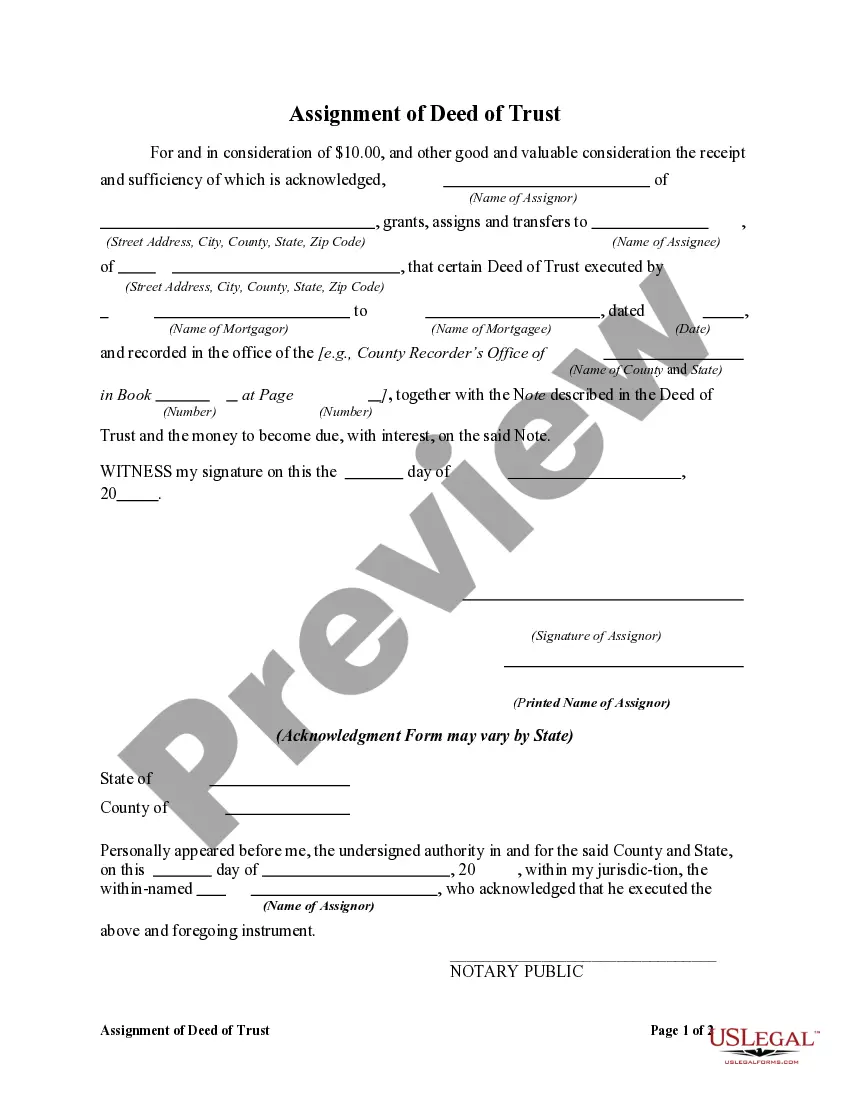

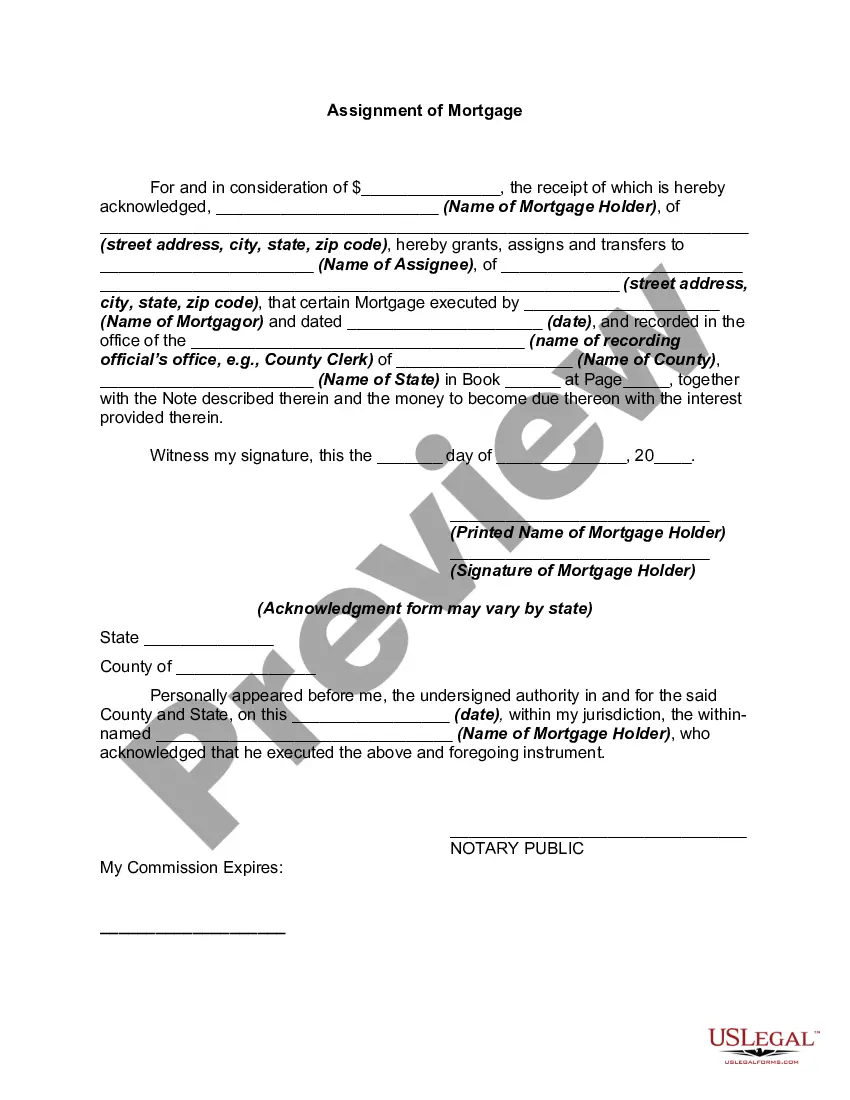

Assignment of Mortgage ? The Basics. When your original lender transfers your mortgage account and their interests in it to a new lender, that's called an assignment of mortgage. To do this, your lender must use an assignment of mortgage document. This document ensures the loan is legally transferred to the new owner.

A disadvantage of a mortgage assignment is the consequences of failing to record it. Under most state laws, an entity seeking to institute foreclosure proceedings must record the assignment before it can do so. If a mortgage is not recorded, the judge will dismiss the foreclosure proceeding.

An assignment of mortgage is a legal term that refers to the transfer of the security instrument that underlies your mortgage loan ? aka your home. When a lender sells the mortgage on, an investor effectively buys the note, and the mortgage is assigned to them at this time.

An assignment transfers all the original mortgagee's interest under the mortgage or deed of trust to the new bank. Generally, the mortgage or deed of trust is recorded shortly after the mortgagors sign it, and, if the mortgage is subsequently transferred, each assignment is recorded in the county land records.

An assignment of mortgage is a legal term that refers to the transfer of the security instrument that underlies your mortgage loan ? aka your home. When a lender sells the mortgage on, an investor effectively buys the note, and the mortgage is assigned to them at this time.

If the mortgagee fails to execute and record a Satisfaction of Mortgage within the 60-day period afforded by statute, the mortgagor (property owner) may file suit and seek a court order directing the mortgagee to execute a satisfaction of mortgage or an order extinguishing the lien against the property.