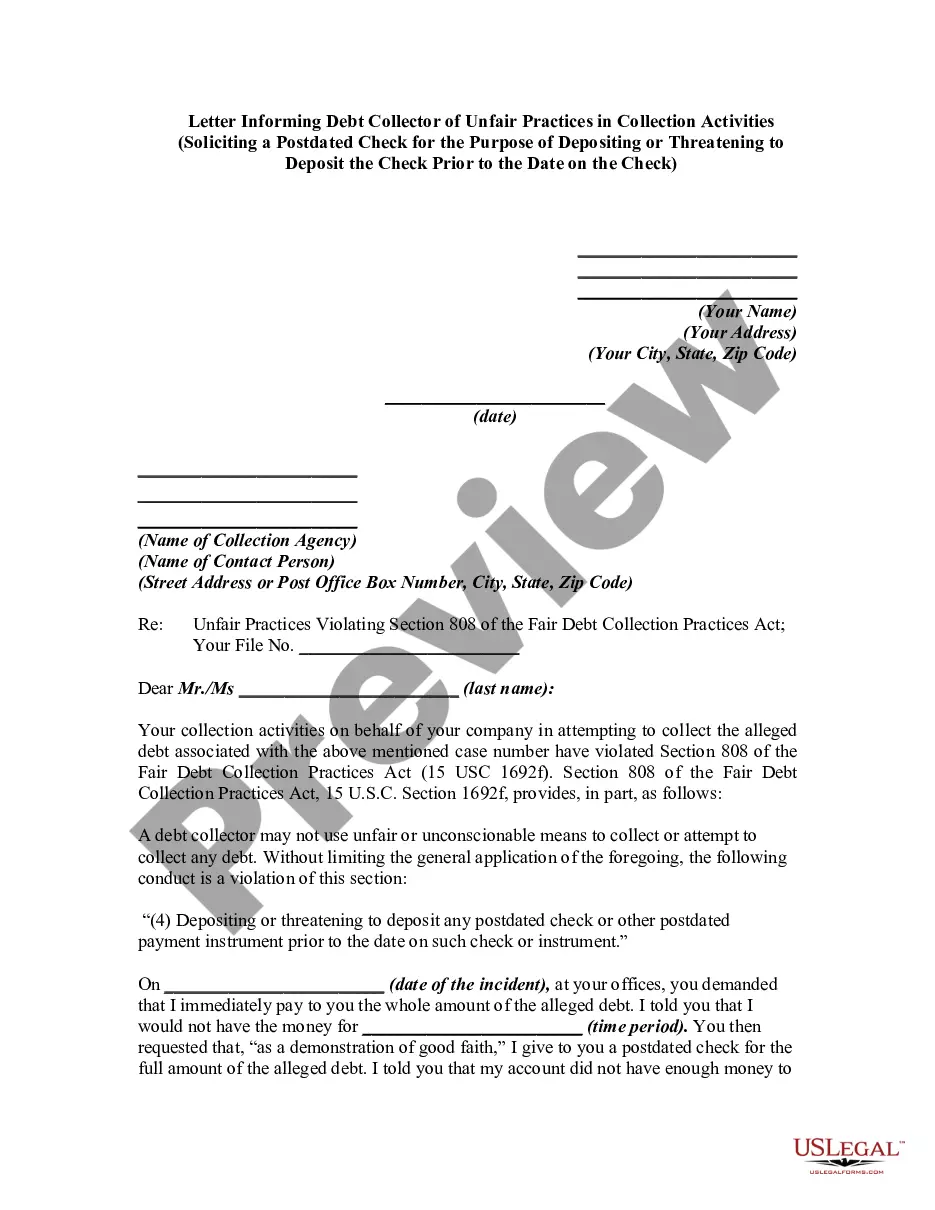

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

Nebraska Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

Selecting the appropriate legal document template can be challenging. Clearly, there are many designs available online, but how can you locate the legal form you need? Utilize the US Legal Forms website.

The platform offers a vast array of templates, such as the Nebraska Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check, which can be used for business and personal purposes. All forms are reviewed by professionals and comply with state and federal requirements.

If you are already registered, Log In to your account and then click the Acquire button to access the Nebraska Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check. Use your account to search for the legal forms you have previously ordered. Go to the My documents tab of your account and download another copy of the document you need.

US Legal Forms is the premier repository of legal forms where you can find various document templates. Utilize the service to download professionally crafted files that adhere to state requirements.

- First, ensure you have selected the correct form for your city/region. You can review the form using the Preview button and examine the form details to confirm this is indeed the right one for you.

- If the form does not meet your needs, utilize the Search field to find the suitable form.

- When you are certain that the form is correct, click the Acquire now button to obtain the form.

- Choose the pricing plan you desire and provide the necessary information. Create your account and pay for your order using your PayPal account or credit card.

- Select the file format and download the legal document template to your device.

- Complete, revise, and print, then sign the received Nebraska Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check.

Form popularity

FAQ

Several banks now offer a service where your paycheck is available one or two days before the regular payday if your employer uses direct deposit. This early direct deposit of your paycheck could help you keep up with bills and avoid late fees, especially on bills due around the time you receive your salary.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

A signed check immediately becomes legal tender that a bank can deposit or cash before the indicated date on the check. Therefore, a bank will be able to accept a check if it is dated and signed. Ask your bank or credit union for their specific policy for postdated checks in their account disclosures.

In most cases, when you receive a postdated check, you can deposit or cash a postdated check at any time. Debt collectors may be prohibited from processing a check before the date on the check, but most individuals are free to take postdated checks to the bank immediately.

Can a bank or credit union cash a post-dated check before the date on the check? Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice.

According to UCC § 3-113, if a financial instrument, such as a check, is undated, its official date is the date on which it first came into the possession of the person or business listed on it. Since banks follow the UCC, your undated check will be deposited.

Post-dated checks are perfectly legal. If they weren't, pay day lenders, and other crude forms of credit, couldn't exist. Only properly payable checks are supposed to be cashed by banks. But just about anything with the right signature on it is properly payable, including post-dated and overdrawn checks.

Yes. Banks and credit unions generally don't have to wait until the date you put on a check to cash it. However, state law may require the bank or credit union to wait to cash the check if you give it reasonable notice. Contact your bank or credit union to learn what its policies are.

Depositing a postdated check a day early may cause the check writer's bank to attempt to pay the check immediately. If the check writer does not yet have the funds in his bank account, this will cause the check to "bounce," or be returned for nonsufficient funds.