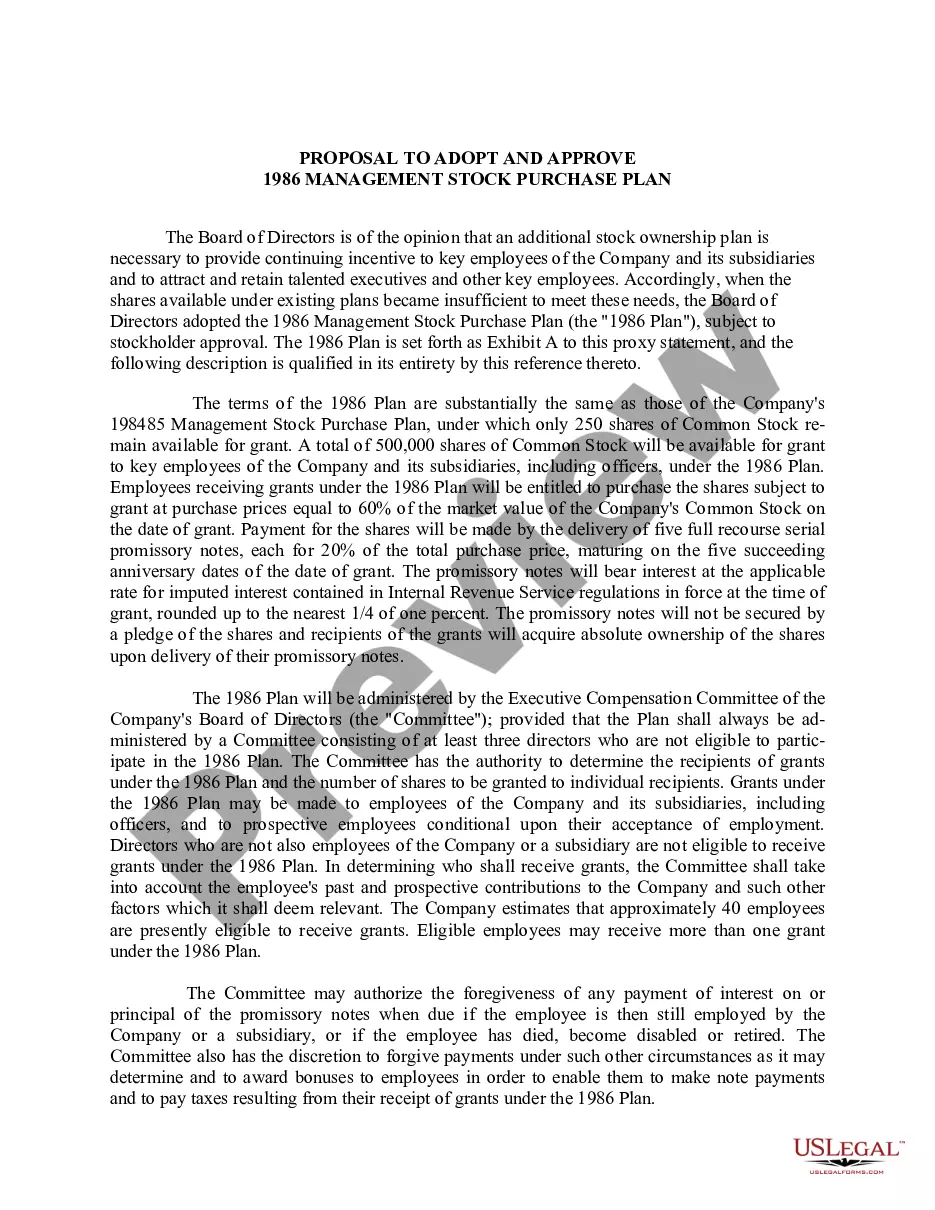

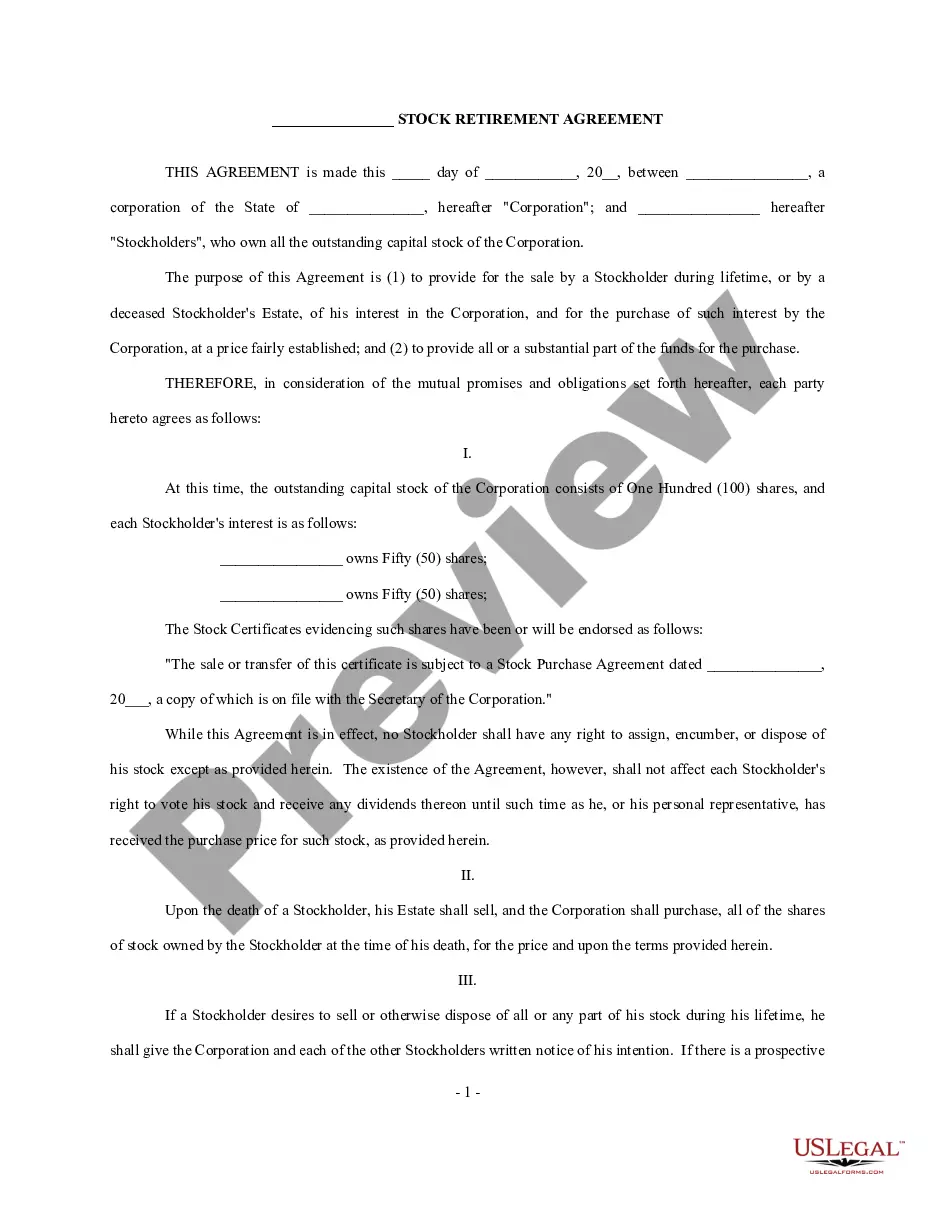

19-223D 19-223D . . . Management Stock Purchase Plan under which Executive Compensation Committee can grant options to key employees (including officers) at prices equal to 60% of market value. Payment is made by delivery of five full recourse interest-bearing serial promissory notes, each for 20% of total purchase price, which mature on five succeeding anniversary dates of date of grant. Committee may forgive any payment of interest or principal on promissory notes if employee is then still employed by Company, has died, or become disabled or retired

Nebraska Management Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-223D

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Management Stock Purchase Plan?

If you wish to full, obtain, or print out legal record themes, use US Legal Forms, the biggest selection of legal varieties, that can be found on-line. Take advantage of the site`s easy and convenient lookup to find the documents you want. Numerous themes for business and specific uses are sorted by types and suggests, or keywords and phrases. Use US Legal Forms to find the Nebraska Management Stock Purchase Plan with a few clicks.

If you are previously a US Legal Forms consumer, log in to the account and click on the Down load key to have the Nebraska Management Stock Purchase Plan. You may also access varieties you earlier delivered electronically inside the My Forms tab of your own account.

If you are using US Legal Forms initially, refer to the instructions listed below:

- Step 1. Ensure you have chosen the form for the correct area/country.

- Step 2. Take advantage of the Preview option to look over the form`s content. Never neglect to learn the description.

- Step 3. If you are not happy together with the develop, make use of the Look for industry at the top of the monitor to get other variations of the legal develop template.

- Step 4. After you have located the form you want, select the Buy now key. Choose the costs plan you like and put your qualifications to sign up for the account.

- Step 5. Procedure the transaction. You may use your bank card or PayPal account to perform the transaction.

- Step 6. Pick the formatting of the legal develop and obtain it on the device.

- Step 7. Full, edit and print out or signal the Nebraska Management Stock Purchase Plan.

Each legal record template you get is your own eternally. You might have acces to each and every develop you delivered electronically in your acccount. Go through the My Forms section and choose a develop to print out or obtain once again.

Contend and obtain, and print out the Nebraska Management Stock Purchase Plan with US Legal Forms. There are many expert and condition-certain varieties you can use for your business or specific requires.

Form popularity

FAQ

Taxes on your ESPP transaction will depend on whether the sale is a qualifying disposition or not. The sale will be considered a qualifying disposition if it meets both of these criteria: You held the stocks for at least one year from the PURCHASE date. You held the stocks for at least two years from the OFFERING date.

They can only report the unadjusted basis ? what the employee actually paid. To avoid double taxation, the employee must use Form 8949. The information needed to make this adjustment will probably be in supplemental materials that come with your 1099-B.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.

Under a Section 423 plan, the IRS limits purchases to $25,000 worth of stock value (based on the FMV on the offering date) for each calendar year.

How is the $25,000 limit calculated? The basic rule is that each employee cannot purchase more than $25,000 per year, valued using the fair market value on the date he/she enrolled in the current offering.

$25,000 Limit . Under all ESPPs of the employer company and its parent and subsidiary corporations, an employee may not purchase more than $25,000 worth of stock (determined based on the fair market value on the first day of the offering period) for each calendar year in which the offering period is in effect.

An employee stock purchase plan (or ESPP) can be a very valuable benefit. In general, if your employer offers an ESPP, we think you should participate at the level you can comfortably afford and then sell the shares as soon as you can.

If you choose to withdraw, you must do so at least 15 days before the purchase date. For example, if the purchase date is June 30, you must make this change prior to June 15. After withdrawing from the plan, if you choose to participate again, you will need to re-enroll during an enrollment period.

How is the $25,000 limit calculated? The basic rule is that each employee cannot purchase more than $25,000 per year, valued using the fair market value on the date he/she enrolled in the current offering.

Qualifying disposition: You sold the stock at least two years after the offering (grant date) and at least one year after the exercise (purchase date). If so, a portion of the profit (the ?bargain element?) is considered compensation income (taxed at regular rates) on your Form 1040.