North Carolina Owner Financing Contract for Vehicle

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Owner Financing Contract For Vehicle?

Selecting the optimal legal document format can be a challenge. Clearly, there are numerous templates accessible online, but how do you identify the legal form you require.

Utilize the US Legal Forms website. The platform provides a vast array of templates, such as the North Carolina Owner Financing Contract for Vehicle, which can be utilized for business and personal purposes. All of the forms are reviewed by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Acquire button to locate the North Carolina Owner Financing Contract for Vehicle. Use your account to browse through the legal forms you have previously purchased. Navigate to the My documents tab in your account to retrieve another copy of the document you need.

Choose the document format and download the legal file format to your device. Complete, modify, and print and sign the acquired North Carolina Owner Financing Contract for Vehicle. US Legal Forms is the largest collection of legal forms where you can access various document templates. Use the service to obtain professionally crafted documents that comply with state regulations.

- First, make sure you have selected the correct form for your region/area.

- You can view the form using the Preview button and read the form description to ensure it is appropriate for you.

- If the form does not meet your criteria, use the Search field to find the suitable form.

- Once you are confident the form is correct, click the Purchase now button to obtain the form.

- Select the pricing plan you prefer and enter the required information.

- Create your account and process the payment using your PayPal account or credit card.

Form popularity

FAQ

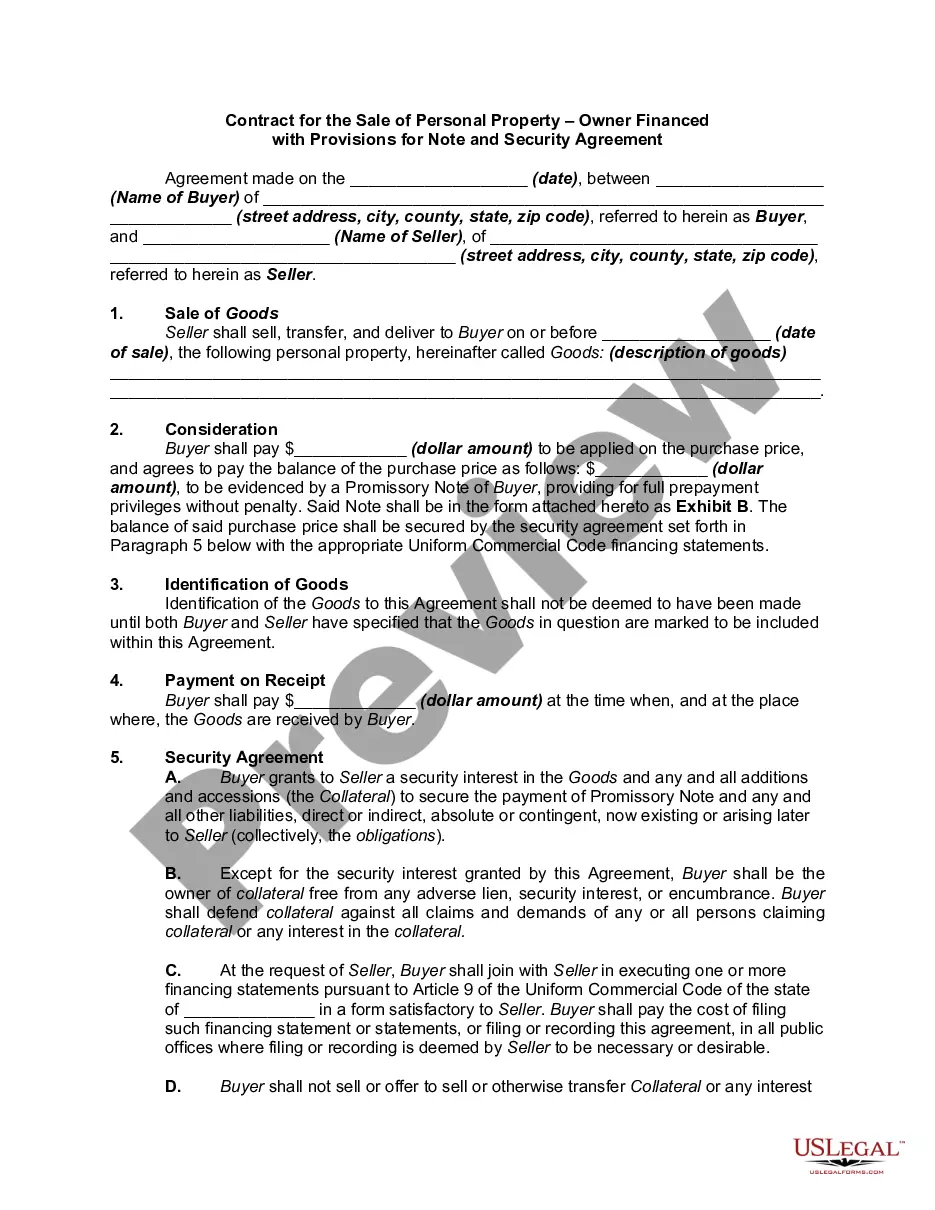

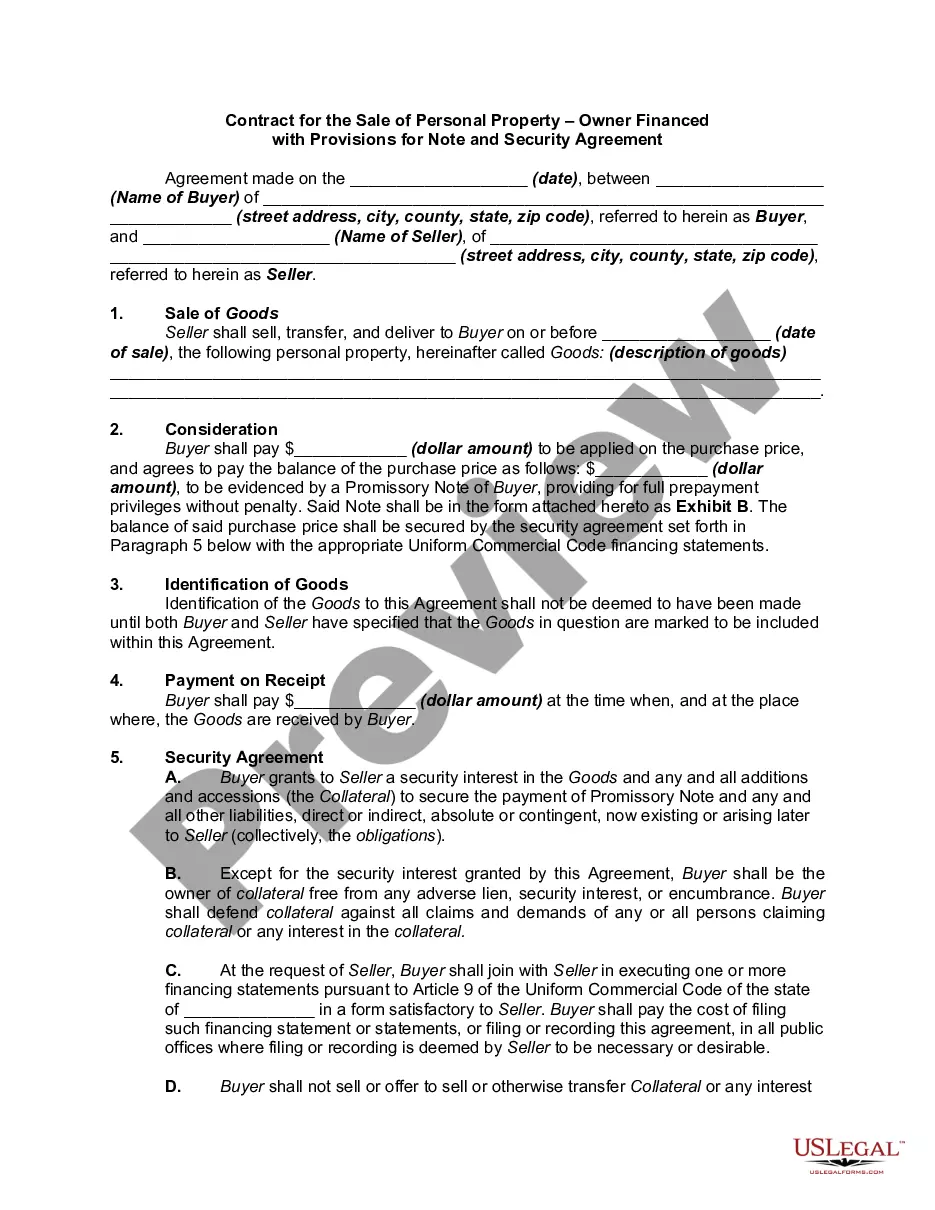

Writing up a North Carolina Owner Financing Contract for Vehicle involves drafting a comprehensive document that covers essential terms like the buyer’s name, vehicle specifics, and financing details. Ensure to specify the down payment, monthly payments, and any penalties for late payment. Using a well-designed template from platforms like uSlegalforms helps ensure you're following state requirements.

Typical terms for a North Carolina Owner Financing Contract for Vehicle include a down payment of 10% to 30%, a repayment period ranging from one to five years, and an interest rate that is usually between 5% and 10%. Buyers and sellers can negotiate these terms, allowing them to find a solution that works for both parties. Ensure you document these terms clearly in your contract.

In a North Carolina Owner Financing Contract for Vehicle, the seller typically holds the title of the vehicle until the buyer fulfills all payment obligations. This means that the buyer has possession of the vehicle, but the seller retains legal ownership. This arrangement protects the seller's interests while providing the buyer the opportunity to own the vehicle over time. It’s crucial to have a clear contract to outline each party's rights and responsibilities.

One primary downside of owner financing is that sellers carry the risk of default. In the case of a default, you might face difficulties in regaining possession of the vehicle. Additionally, if the buyer fails to meet payment obligations, you may find it harder to sell the vehicle again in the future. Therefore, it’s essential to use a well-structured North Carolina Owner Financing Contract for Vehicle to outline the terms and protect both parties involved.

A payment plan agreement, also known as an installment agreement, is a written legal document that allows one party to make smaller payments over time to payoff a larger debt.

Follow these six easy steps to set up a debt repayment plan.Make a List of All Your Debts.Rank Your Debts.Find Extra Money To Pay Your Debts.Focus on One Debt at a Time.Move On to the Next Debt on Your List.Build Up Your Savings.Other Tips.

Outline the Terms. Write the terms of payment. Include the full amount, any deposit amount, the date or dates of payments and what types of payment were agreed upon. If you give a deposit or down payment for the car, ask the seller to provide you with a receipt.

With an AFS, title remains in the Seller's name and the Seller continues to make the mortgage payments to the bank. The bank's records do not change. Title changes only once the Seller's equity is paid in full which occurs, usually, when the Purchaser is in a position to arrange bank financing.

With owner financing (aka seller financing), the seller doesn't hand over any money to the buyer as a mortgage lender would. Instead, the seller extends enough credit to the buyer to cover the purchase price of the home, less any down payment. Then, the buyer makes regular payments until the amount is paid in full.

Here are three main ways to structure a seller-financed deal:Use a Promissory Note and Mortgage or Deed of Trust. If you're familiar with traditional mortgages, this model will sound familiar.Draft a Contract for Deed.Create a Lease-purchase Agreement.