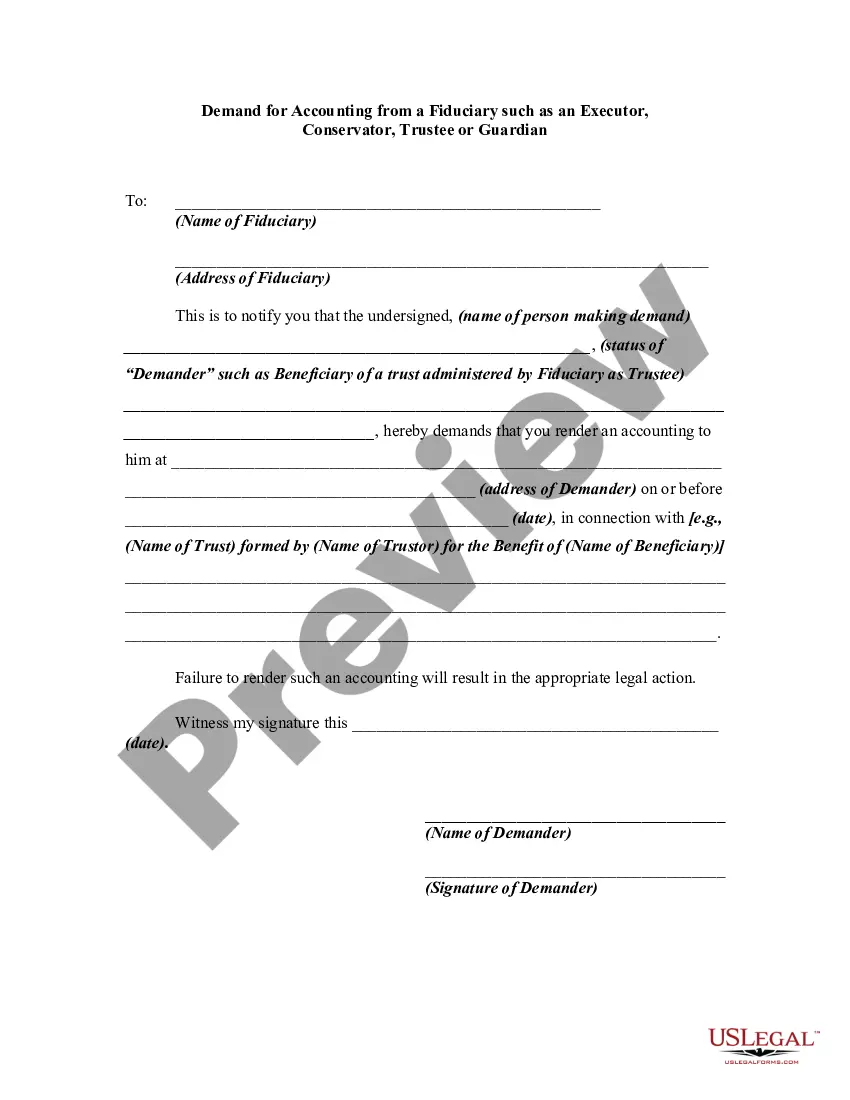

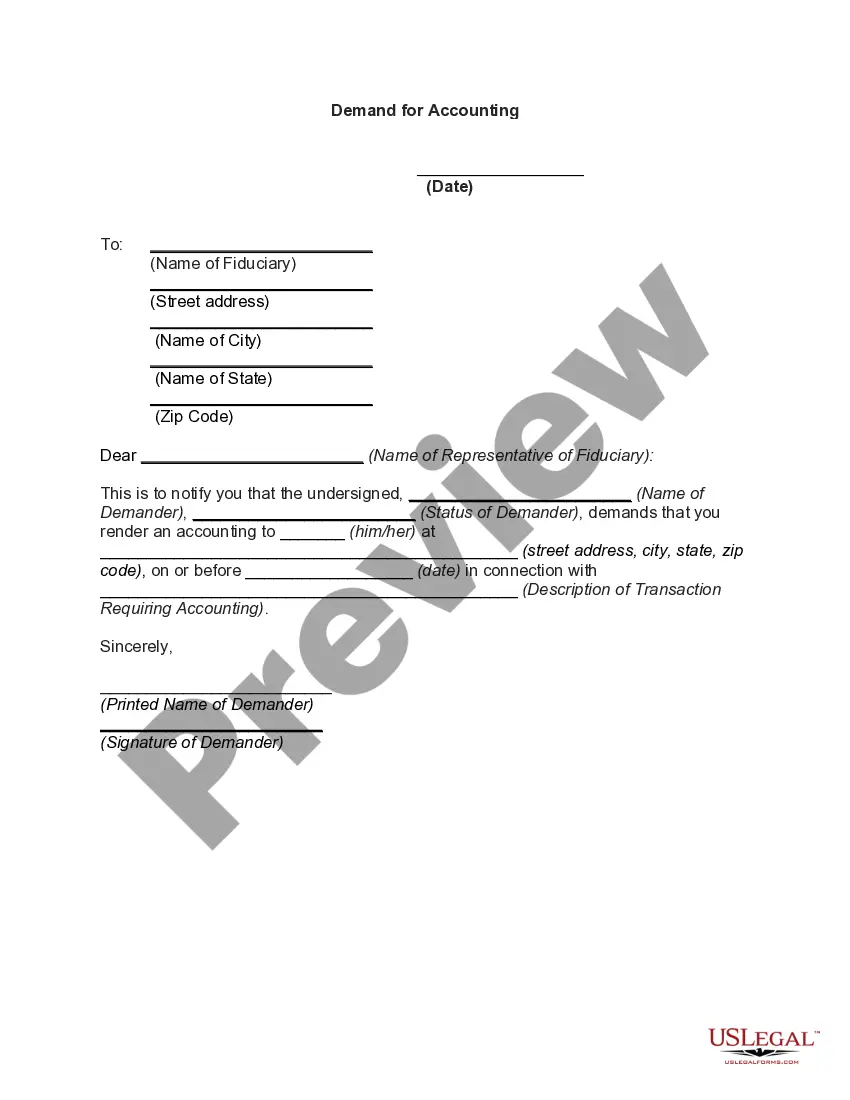

Sometimes, a prior demand by a potential plaintiff for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Montana Demand for Accounting from a Fiduciary

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary?

Locating the appropriate legal document template may be challenging.

Of course, there are numerous designs accessible online, but how can you secure the legal document you need.

Utilize the US Legal Forms platform. The service offers a vast array of templates, such as the Montana Demand for Accounting from a Fiduciary, that can be utilized for business and personal purposes.

If the document does not meet your requirements, use the Search field to find the correct form.

- All the documents are verified by experts and comply with state and federal regulations.

- If you are currently registered, Log In to your account and click on the Acquire button to obtain the Montana Demand for Accounting from a Fiduciary.

- Use your account to search for the legal documents you have previously acquired.

- Go to the My documents section of your account and retrieve another copy of the document you need.

- If you are a new user of US Legal Forms, here are easy steps for you to follow.

- First, make sure you have selected the correct document for your locality. You can review the document using the Preview button and read the document description to ensure it is the right one for you.

Form popularity

FAQ

Fiduciary accounting involves keeping detailed records of all financial activities concerning a fiduciary relationship. An example would be a guardian managing a minor's inherited estate, where they must provide a clear account of income, expenses, and distributions. The guardian must adhere to strict accounting standards to prove they are fulfilling their duties. If you seek support, the Montana Demand for Accounting from a Fiduciary ensures proper compliance and transparency.

A fiduciary account is a bank account established for managing funds on behalf of another individual or entity. This type of account is designed to ensure that funds are used solely for the intended beneficiary. It is important to understand that fiduciary accounts can include trust accounts, estate accounts, and conservatorship accounts. If you face issues, a Montana Demand for Accounting from a Fiduciary can clarify the account's management.

On a 1041 for an estate, you can generally deduct expenses related to the management of the estate, including fees for fiduciaries and administrative costs. Also, deductible debts or losses associated with estate property may apply. Understanding these deductions is crucial for compliance with the Montana Demand for Accounting from a Fiduciary.

The filing requirement for a fiduciary return typically arises when the trust generates more than $600 in gross income or has a beneficiary who is a nonresident alien. Timely filing is essential to meet state and federal obligations. This diligence is particularly important in fulfilling the Montana Demand for Accounting from a Fiduciary responsibly.

Filling out a 1041 estate tax return involves gathering all trust income and deductible expenses, then accurately reporting them on the form. Use reliable software or resources to ensure each line is correctly completed, as errors can lead to complications. Seeking assistance with this form can be crucial for navigating the complexities of the Montana Demand for Accounting from a Fiduciary.

IRS Form 1041 is the U.S. Income Tax Return for Estates and Trusts. It allows fiduciaries to report the income generated by a trust or estate for tax purposes. Simplifying this process can help in addressing the Montana Demand for Accounting from a Fiduciary, making compliant reporting much easier.

A fiduciary return primarily focuses on the income generated by a trust, while an estate tax return deals with the overall estate value and any applicable taxes after the individual’s passing. Each return serves distinct purposes, and understanding these differences is fundamental for accurate financial reporting. Addressing the Montana Demand for Accounting from a Fiduciary often requires clear distinctions between these two types of returns.

To calculate accounting income for a trust, begin by accumulating all income sources, including interest, dividends, and capital gains. Then, deduct any expenses related to the trust’s administration, like fees or taxes. Accurate calculations play a crucial role in fulfilling the Montana Demand for Accounting from a Fiduciary, ensuring fair distribution to beneficiaries.

The exemption amount for an estate on a 1041 can vary over time, but it generally follows the federal guidelines. For many estates, this exemption significantly reduces the taxable income and provides relief during the settlement process. Understanding these exemptions helps in managing your obligations, particularly when addressing the Montana Demand for Accounting from a Fiduciary.

Fiduciary accounting income typically includes all income earned from the trust assets, such as interest, dividends, and rental income. When you evaluate fiduciary accounting, it's vital to consider the income that is generated during the trust administration. Accurate accounting is essential to meet the Montana Demand for Accounting from a Fiduciary and ensure transparency in asset management.