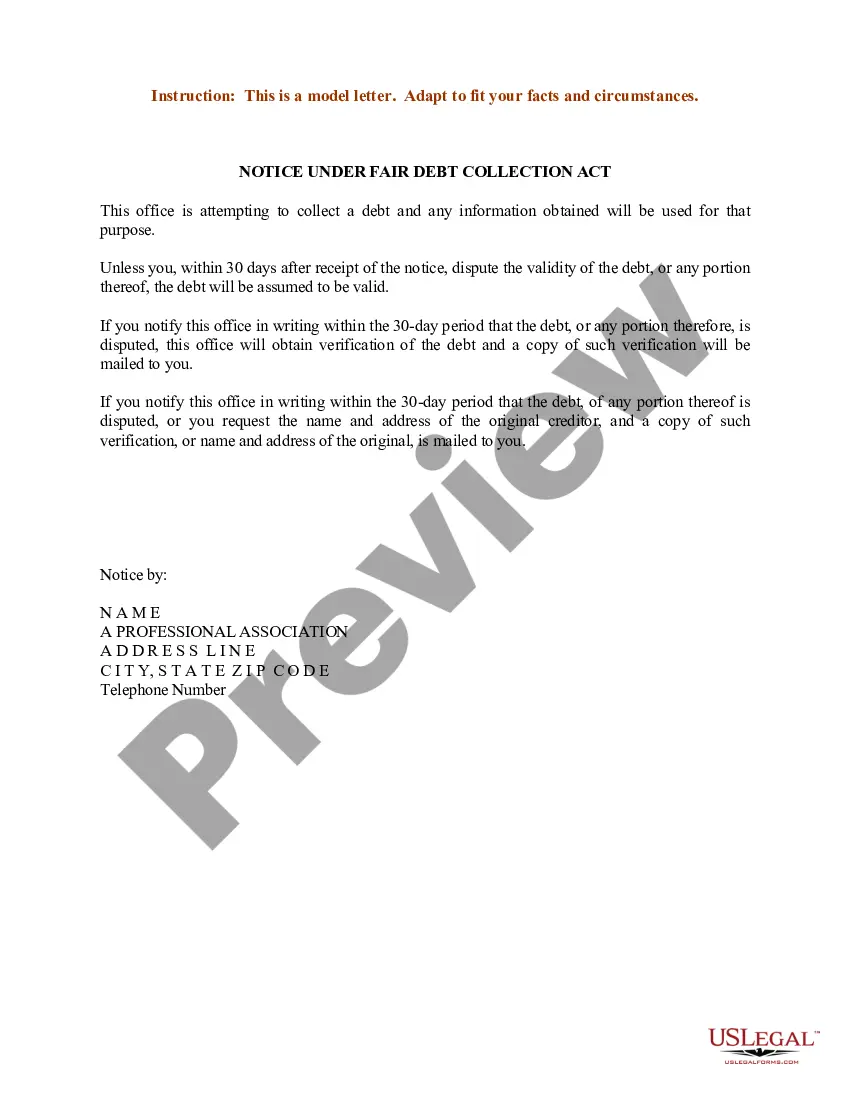

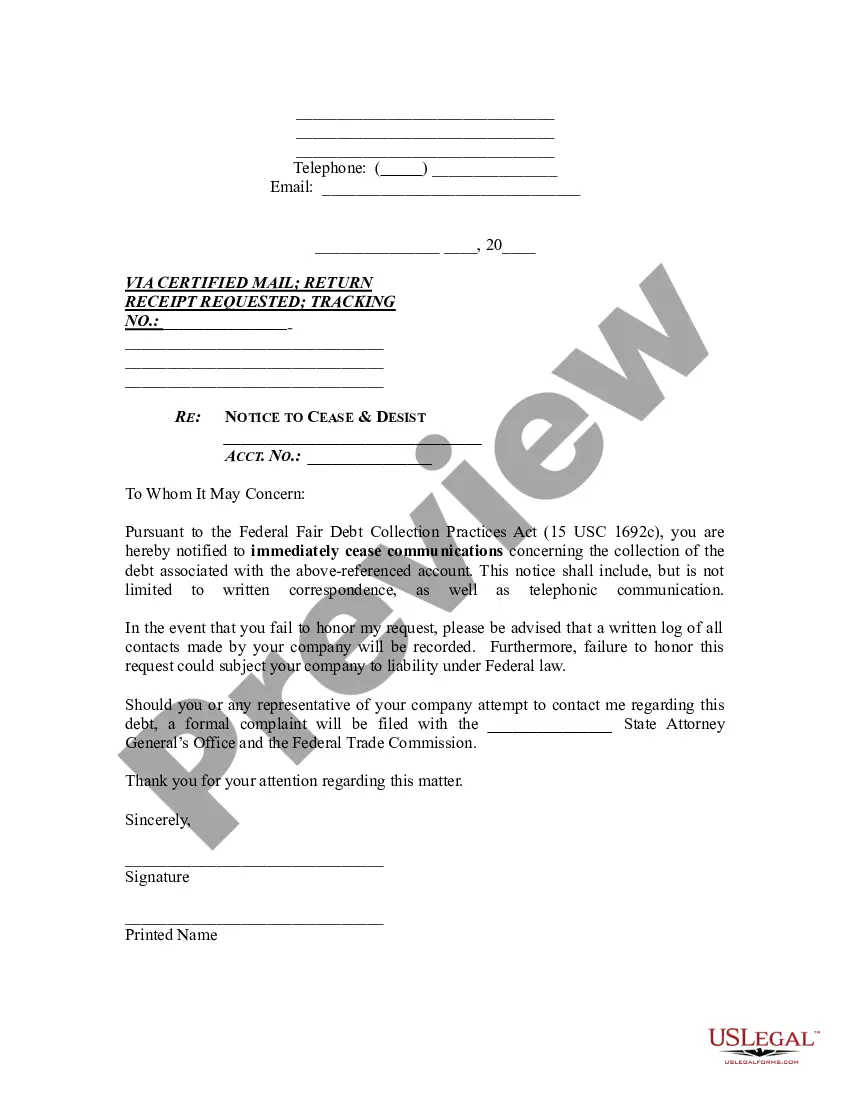

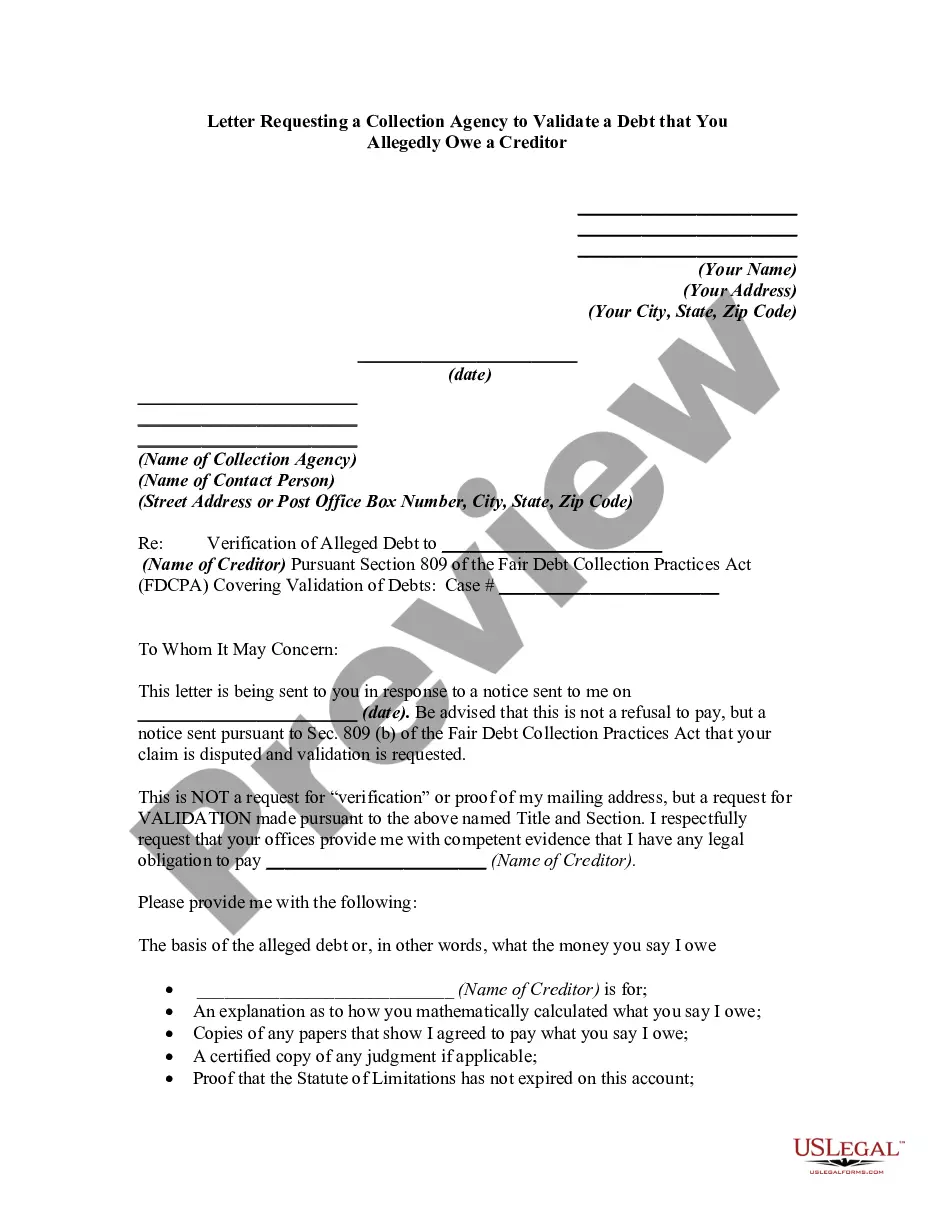

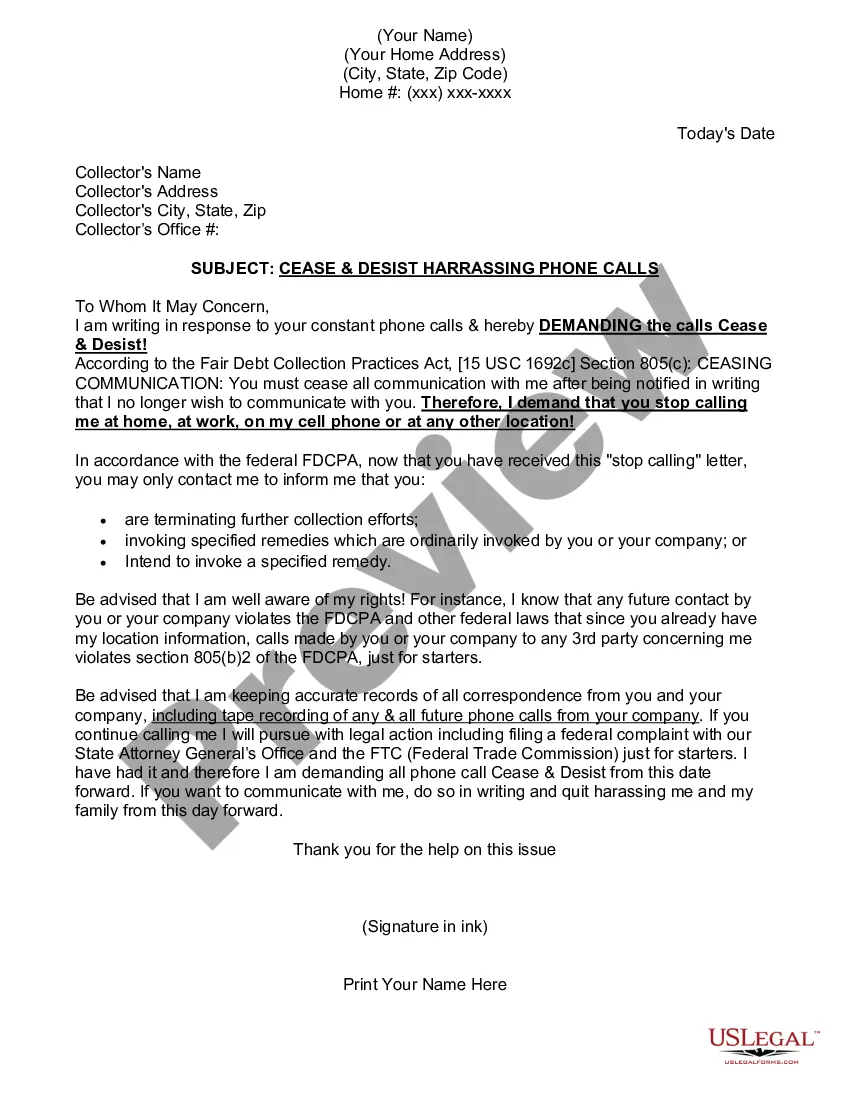

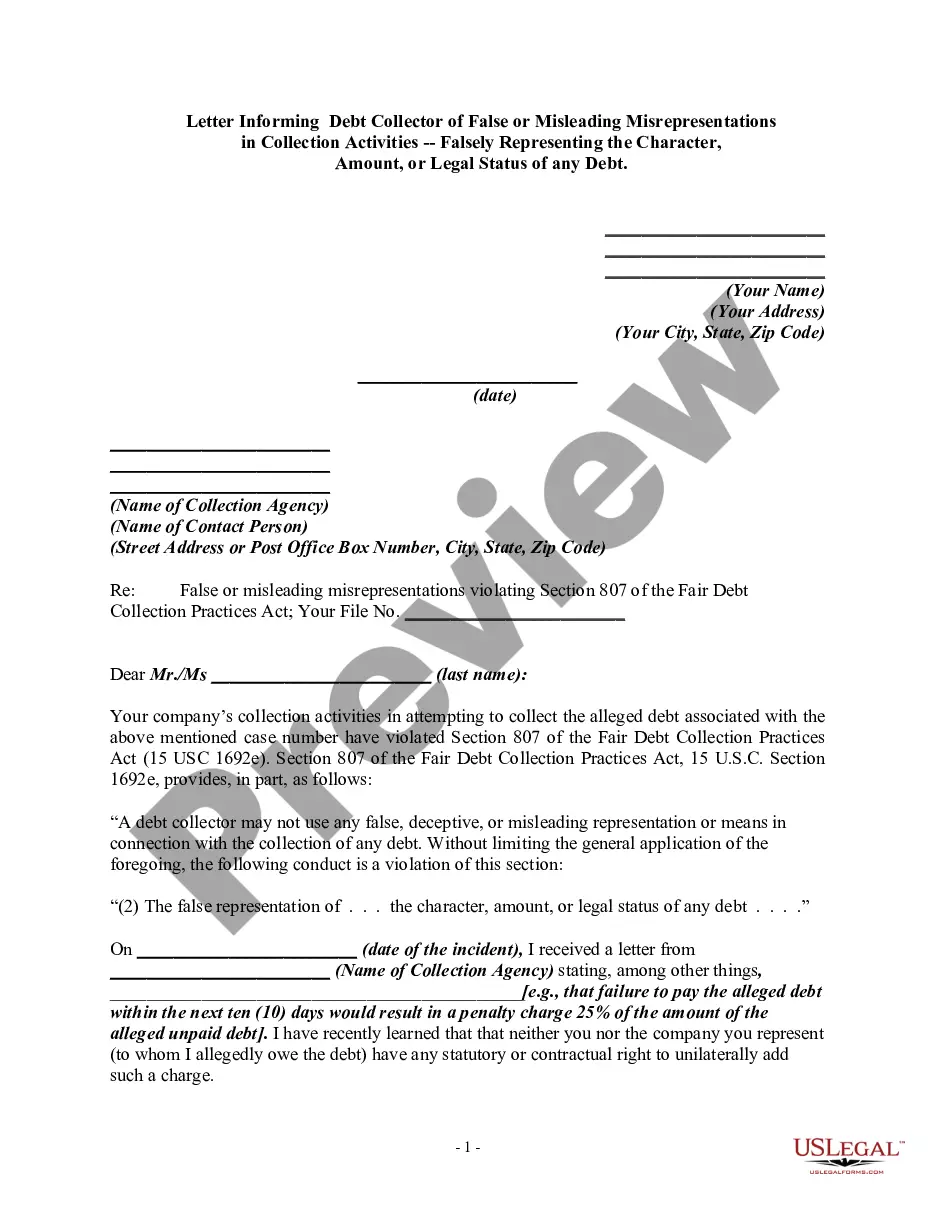

This NOTICE OF HARRASSMENT & VALIDATION OF DEBT is to be used when creditors call you repeatedly and mail you letters too. This form includes a cease and desist and a validation of debt, 2 letters in one.

Mississippi Notice of Harassment and Validation of Debt

Instant download

Description

How to fill out Notice Of Harassment And Validation Of Debt?

You might spend time online looking for the legal document template that meets both state and federal requirements you need.

US Legal Forms provides thousands of legal forms that have been reviewed by experts.

You can easily obtain or create the Mississippi Notice of Harassment and Validation of Debt from the service.

If available, utilize the Review option to look through the document template as well. If you wish to find another version of your form, use the Search field to discover the template that fits your needs and requirements. Once you’ve found the template you want, click Purchase now to proceed. Select the pricing plan you prefer, input your details, and register for an account on US Legal Forms. Complete the transaction. You can use your Visa or Mastercard or PayPal account to purchase the legal document. Choose the format of your document and download it to your device. Make edits to your document if necessary. You can fill out, amend, sign, and print the Mississippi Notice of Harassment and Validation of Debt. Download and print thousands of document templates using the US Legal Forms Website, which offers the largest collection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you already possess a US Legal Forms account, you can Log In and select the Download option.

- Then, you can fill out, modify, print, or sign the Mississippi Notice of Harassment and Validation of Debt.

- Every legal document template you purchase is yours indefinitely.

- To obtain another copy of any purchased form, navigate to the My documents section and click the appropriate option.

- If you are using the US Legal Forms website for the first time, follow the straightforward instructions below.

- First, ensure you have selected the correct document template for the county/region you choose.

- Review the form outline to confirm you have chosen the right document.

Form popularity

FAQ

Receiving a debt validation letter indicates that a creditor is requesting you to confirm a debt they claim you owe. Under the Mississippi Notice of Harassment and Validation of Debt, this letter serves as your opportunity to verify the debt's legitimacy. It is important to respond promptly and professionally, ensuring your rights as a consumer are upheld. If you need assistance, platforms like USLegalForms can provide you with the tools to navigate this process effectively.

A debt validation notice is typically sent to inform you that a collector is attempting to collect a debt. This notice is required under the Mississippi Notice of Harassment and Validation of Debt, which mandates that you receive information about the debt and your rights. Understanding why you received this notice can help you take the necessary steps to verify the debt and respond appropriately. Always review the notice carefully to ensure the information is accurate.

When you receive a debt validation letter, it is crucial to review the information provided carefully. You should respond in writing, asking for specific details about the debt, such as the original creditor's name and the amount owed. Utilize the provisions of the Mississippi Notice of Harassment and Validation of Debt to ensure your response is clear and assertive. This step helps protect your rights and ensures that you are dealing with legitimate debt claims.

Debt collection becomes harassment when collectors use aggressive tactics, such as threatening legal action or repeatedly calling you at unreasonable hours. Under the Mississippi Notice of Harassment and Validation of Debt, you have the right to report these practices. It is essential to recognize your rights and take action if you feel that a collector is crossing the line. Keeping detailed records of communications can also help if you need to file a complaint.

In the United States, you generally do not go to jail for having debt. However, if you fail to respond to a court summons related to a debt, you may face legal consequences. It is important to understand your rights under the Mississippi Notice of Harassment and Validation of Debt, as it protects you from unfair treatment by creditors. Staying informed can help you navigate any legal challenges effectively.

An example of a debt validation letter includes your personal information at the top, followed by a greeting to the creditor. In the body, request validation of the debt, specify the amount, and reference the Mississippi Notice of Harassment and Validation of Debt. You can find examples on various legal websites, including uslegalforms, to tailor your letter effectively.

To fill out a debt validation letter, start with your contact information, the date, and the creditor's details. Clearly state your request for validation and include any relevant account numbers. Utilize the Mississippi Notice of Harassment and Validation of Debt as a guideline to ensure your letter meets legal standards, and keep a copy for your records.

Yes, debt validation letters can be effective. They compel creditors to provide proof of the debt under the Mississippi Notice of Harassment and Validation of Debt. By sending a validation letter, you may be able to halt collection activities while the creditor verifies the debt, giving you time to assess your situation.

When answering a summons for debt collection in Mississippi, first read the summons carefully and note the response deadline. Prepare a written response that addresses each claim made by the creditor, referencing the Mississippi Notice of Harassment and Validation of Debt. You may want to seek legal advice or use resources from uslegalforms to ensure your answer is complete and accurate.

To prepare a debt validation letter, start by clearly stating your name, address, and the date. Include the creditor's details and specify that you are requesting validation of the debt under the Mississippi Notice of Harassment and Validation of Debt. Be concise, polite, and request all necessary documentation to support the claim. This approach ensures you remain organized and informed.