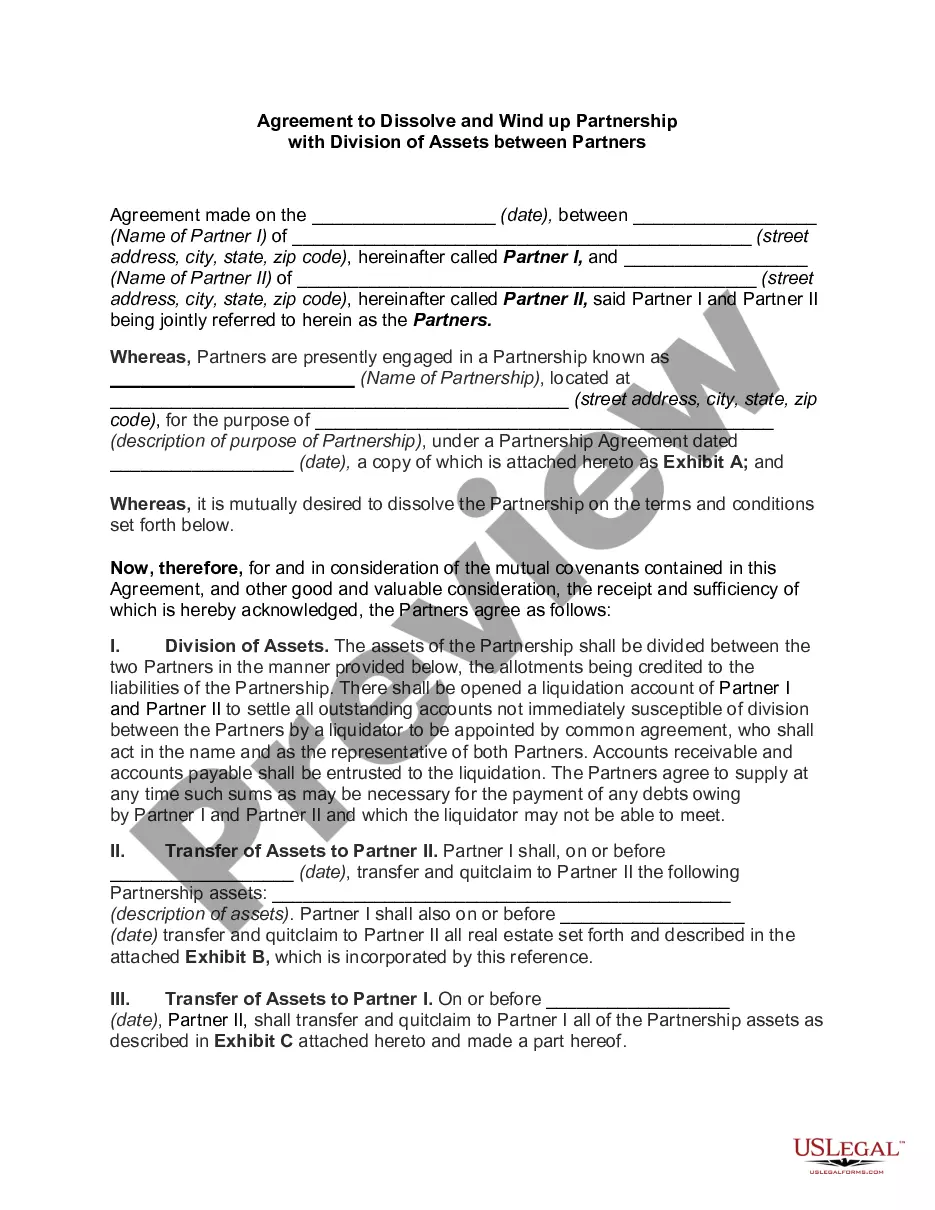

Mississippi Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner

Description

How to fill out Agreement To Dissolve And Wind Up Partnership Between Surviving Partners And Estate Of Deceased Partner?

US Legal Forms - one of the largest collections of legal documents in the USA - provides an extensive selection of legal document templates that you can download or create.

Through the website, you can access thousands of forms for business and personal use, organized by categories, states, or keywords. You can find the latest versions of documents similar to the Mississippi Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner in just a few seconds.

If you already have a subscription, Log In and download the Mississippi Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner from the US Legal Forms library. The Download button will appear on every form you view. You can access all previously obtained forms from the My documents tab of your account.

Process the transaction. Use your credit card or PayPal account to complete the transaction.

Select the format and download the form to your system. Make edits. Fill out, modify, print, and sign the obtained Mississippi Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner. Each template you added to your account has no expiration date and belongs to you forever. So, if you wish to download or print another copy, simply visit the My documents section and click on the form you need. Access the Mississippi Agreement to Dissolve and Wind up Partnership between Surviving Partners and Estate of Deceased Partner with US Legal Forms, which is the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and requirements.

- To start using US Legal Forms for the first time, here are simple steps to get started.

- Ensure that you have selected the correct form for your city/county.

- Click the Preview button to view the content of the form.

- Read the form description to confirm that you have chosen the right form.

- If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button.

- Then, choose your preferred pricing plan and provide your credentials to register for an account.

Form popularity

FAQ

A general partnership is an unincorporated business with two or more owners who share business responsibilities. Each general partner has unlimited personal liability for the debts and obligations of the business. Each partner reports their share of business profits and losses on their personal tax return.

Keeping it successful is even harder, and coping with the death of a partner may be the hardest situation of all. When that happens, your deceased partner's share in the business usually passes to a surviving spouse, either by terms of a will or simply by default as the primary heir.

The death of a partner in a two-person partnership will terminate the partnership for federal tax purposes if it results in the partnership's immediately winding up its business (Sec. 708(b)(1)(A)). If this occurs, the partnership's tax year closes on the partner's date of death.

In a general partnership, all parties share legal and financial liability equally. The individuals are personally responsible for the debts the partnership takes on. Profits are also shared equally. The specifics of profit sharing will almost certainly be laid out in writing in a partnership agreement.

In a general partnership, each partner has unlimited personal liability. Partnership rules usually dictate that whatever debts are incurred by the business, it is the legal responsibility of all partners to pay them off.

Partners are personally liable for the business obligations of the partnership. This means that if the partnership can't afford to pay creditors or the business fails, the partners are individually responsible to pay for the debts and creditors can go after personal assets such as bank accounts, cars, and even homes.

In a general partnership: all partners (called general partners) are personally liable for all business debts, including court judgments. each individual partner can be sued for the full amount of any business debt (though that partner can in turn sue the other partners for their share of the debt), and.

Partners owe general duties and responsibilities to the partnership....These responsibilities include:a duty of loyalty and care,equal profit sharing (unless there's an agreement that says otherwise), and.equal control and no salary (unless there's an agreement).

In return for giving up management power, limited partners get the benefit of protection from personal liability. This means that a limited partner can't be forced to pay off business debts or claims with personal assets. A limited partner, however, can lose his or her financial investment in the business.

The retirement, death, or insanity of a general partner dissolves the partnership, unless the business is continued by the remaining partners under a right to do so stated in the certificate, or with the consent of all members.