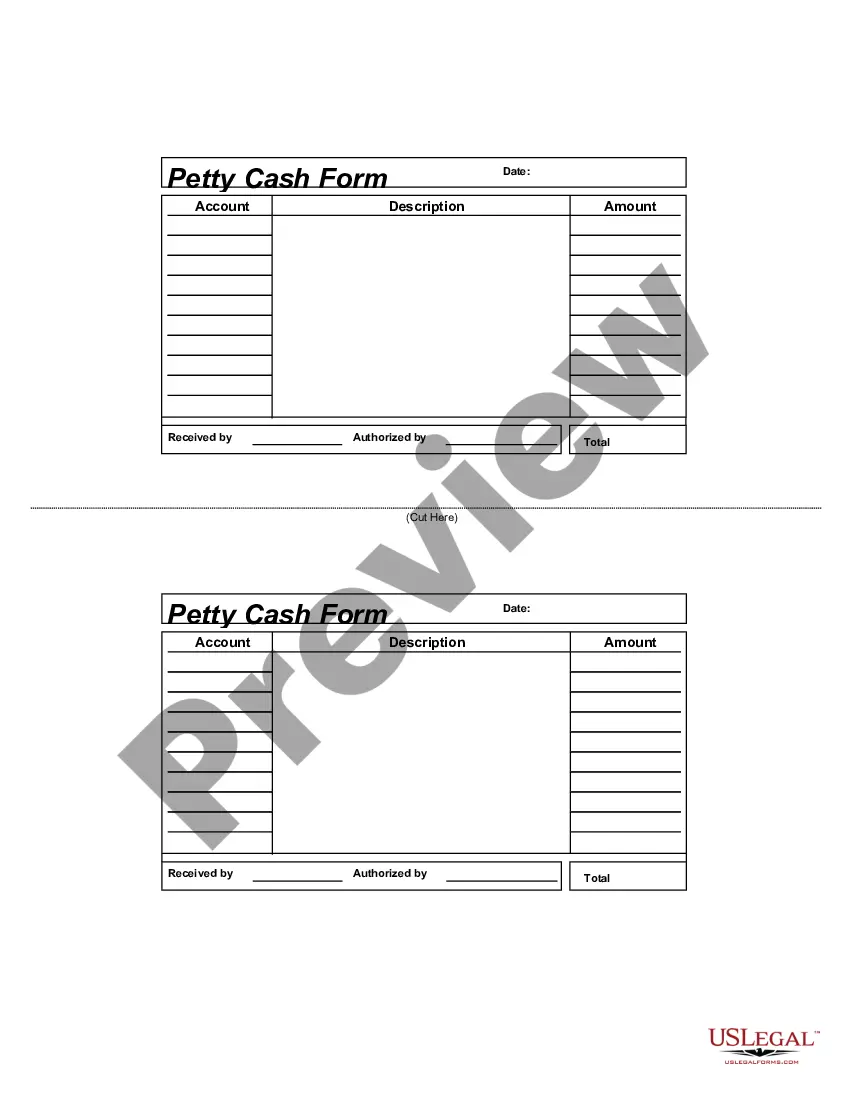

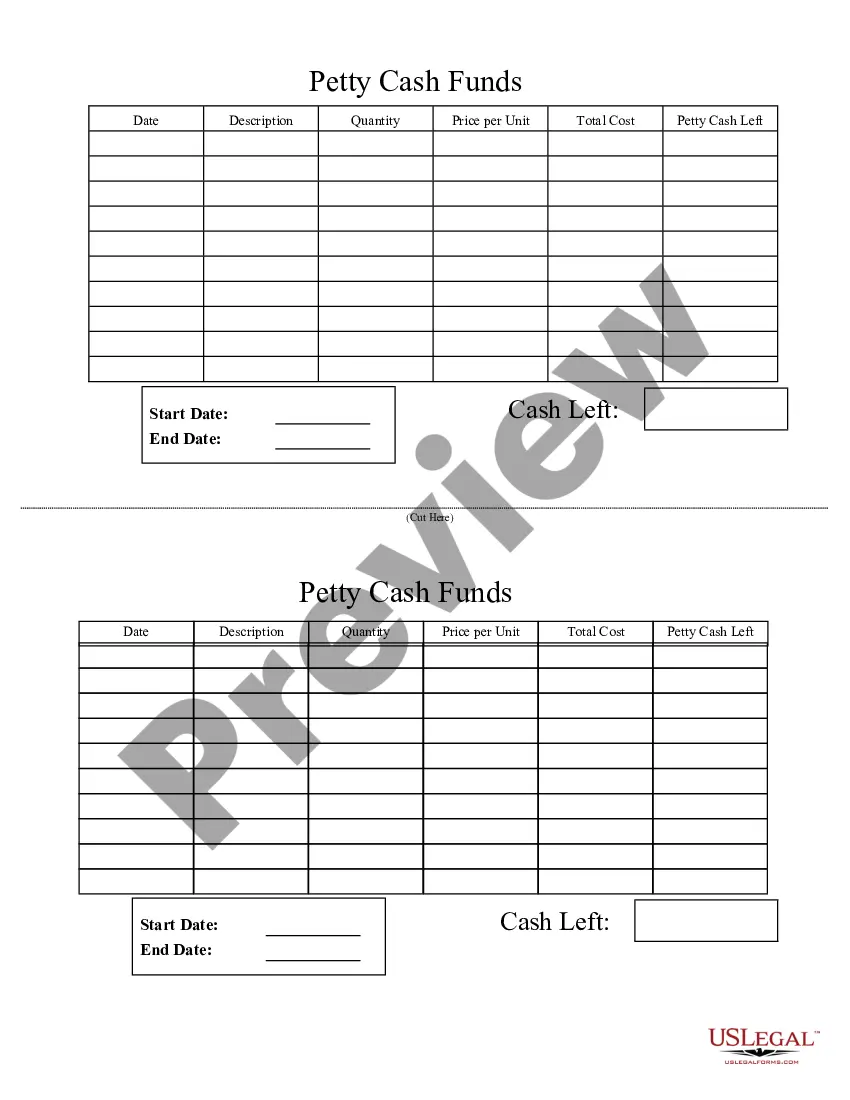

Missouri Petty Cash Journal

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Petty Cash Journal?

If you wish to be thorough, acquire, or create official document templates, utilize US Legal Forms, the largest selection of legal forms available online.

Leverage the site's intuitive search to find the documents you require.

Various templates for business and individual purposes are organized by categories and states, or search terms. Utilize US Legal Forms to obtain the Missouri Petty Cash Journal in just a few clicks.

Every legal document template you obtain is yours permanently. You have access to each form you acquired in your account. Select the My documents section and choose a form to print or download again.

Complete and acquire, and print the Missouri Petty Cash Journal with US Legal Forms. There are numerous professional and state-specific forms you can utilize for your business or personal needs.

- If you are already a US Legal Forms customer, Log In to your account and click on the Acquire button to locate the Missouri Petty Cash Journal.

- You can also access forms you have previously obtained in the My documents tab of your account.

- If this is your first time using US Legal Forms, follow the steps below.

- Step 1. Ensure you have selected the form for your appropriate city/region.

- Step 2. Use the Review function to go through the form's content. Be sure to read the details.

- Step 3. If you are not satisfied with the form, utilize the Lookup field at the top of the screen to find alternative forms in the legal document template.

- Step 4. Once you have located the form you need, select the Acquire now button. Choose the pricing plan you prefer and input your information to register for an account.

- Step 5. Process the payment. You can use your credit card or PayPal account to complete the transaction.

- Step 6. Choose the format of the legal document and download it to your device.

- Step 7. Complete, modify, and print or sign the Missouri Petty Cash Journal.

Form popularity

FAQ

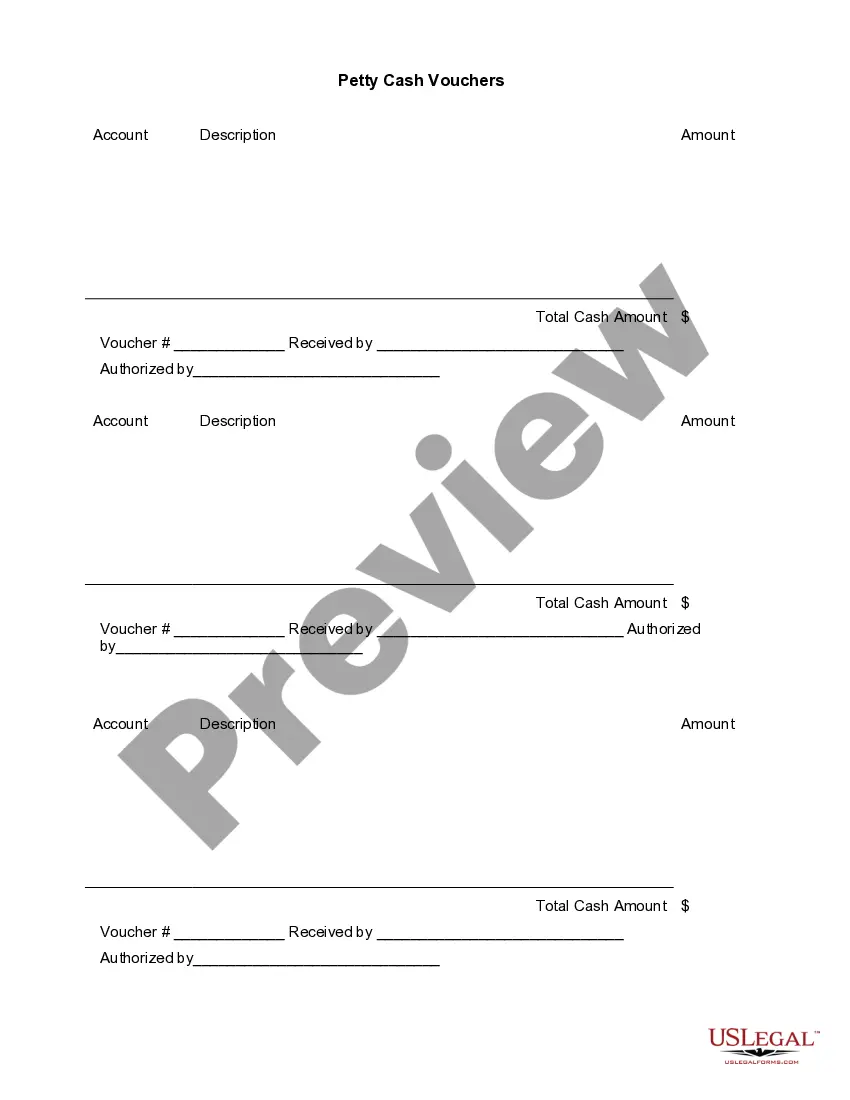

The journal entry that needs to be recorded is a debit (increase) to the petty cash fund and a credit (decrease) to the business checking account. Withdrawals made to the petty cash fund will be recorded as expenses.

A petty cash account is an imprest account, so it is only debited when the fund is initially established or increased in amount. Transactions to replenish the account involve a debit to the expenses and a credit to the cash account (e.g., bank account).

Journal entry for putting money into the petty cash fund The entry must show an increase in your Petty Cash account and a decrease in your Cash account. To show this, debit your Petty Cash account and credit your Cash account. When the petty cash fund gets too low, you must refill it to its set amount.

Recording petty cash transactionsCreate new a bank account to represent your petty cash balance.Enter an opening balance to show the current balance of your petty cash.Record payments made from your petty cash.Record a transfer of money to top up the petty cash account.

Replenishing Petty Cash To determine which accounts to debit, an employee summarizes the petty cash vouchers according to the reasons for expenditure. The journal entry to record replenishing the fund would debit the various accounts indicated by the summary and credit Cash.

When a petty cash fund is in use, petty cash transactions are still recorded on financial statements. No accounting journal entries are made when purchases are made using petty cash, it's only when the custodian needs more cashand in exchange for the receipts, receives new fundsthat the journal entries are recorded.

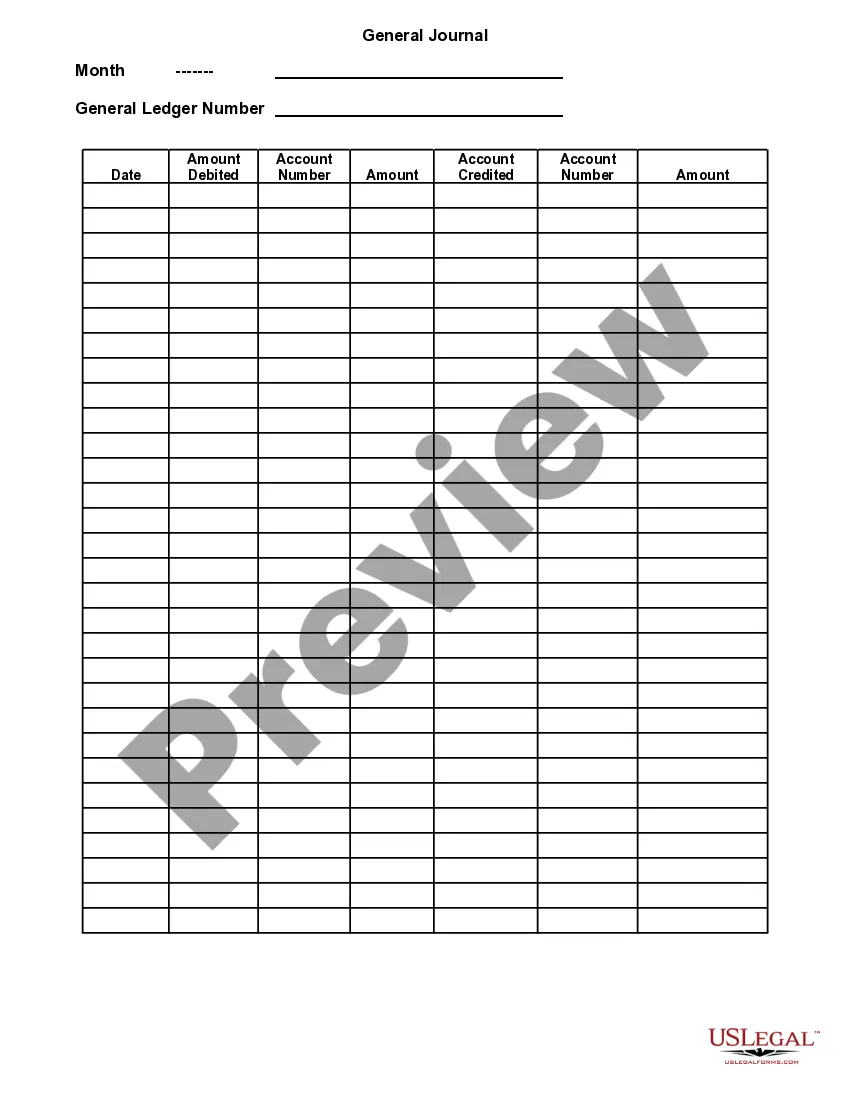

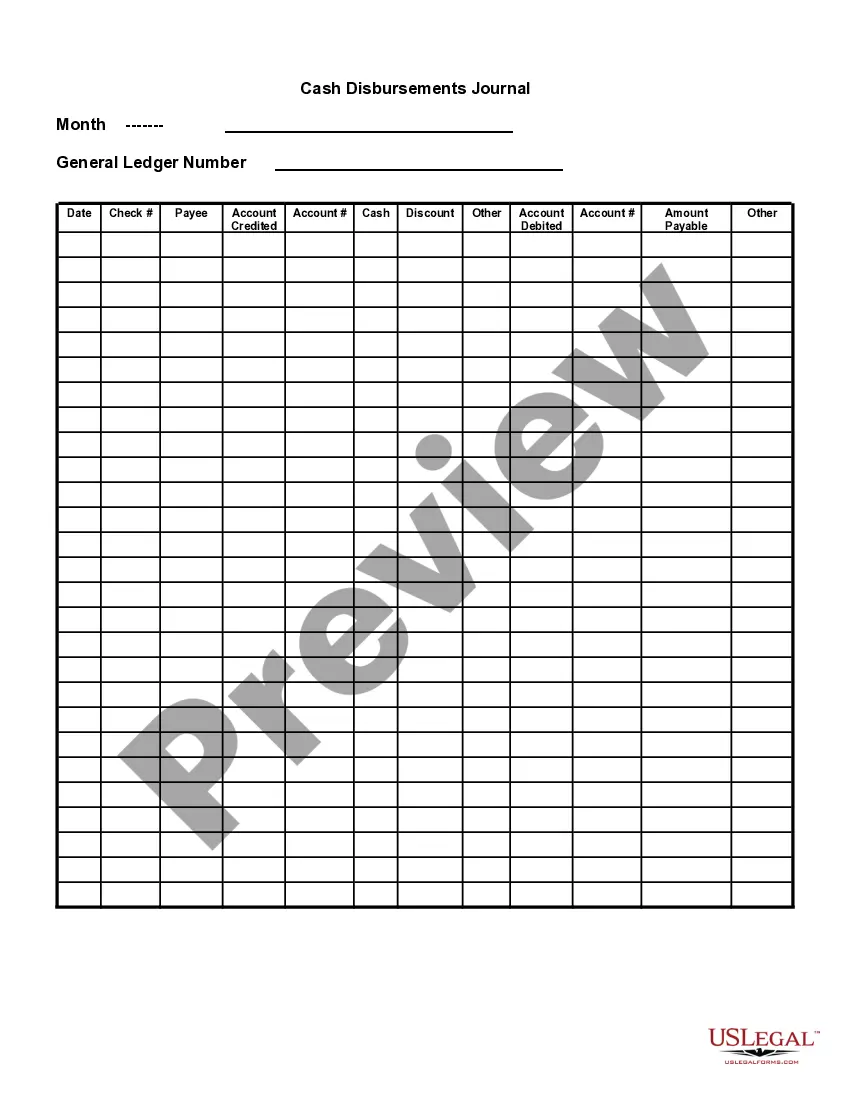

The petty cash journal contains a summarization of the payments from a petty cash fund. The totals in the journal are then used as the basis for a journal entry into a company's general ledger. This journal entry lists petty cash expenditures by expense type.

A simple petty cash book is just like the main cash book. Cash received by the petty cashier is recorded on the debit side, and all payments for petty expenses are recorded on the credit side in one column.

The petty cash journal entry is a debit to the petty cash account and a credit to the cash account. The petty cash custodian refills the petty cash drawer or box, which should now contain the original amount of cash that was designated for the fund. The cashier creates a journal entry to record the petty cash receipts.

Petty cash is a current asset and should be listed as a debit on the company balance sheet. To initially fund a petty cash account, the accountant should write a check made out to "Petty Cash" for the desired amount of cash to keep on hand and then cash the check at the company's bank.