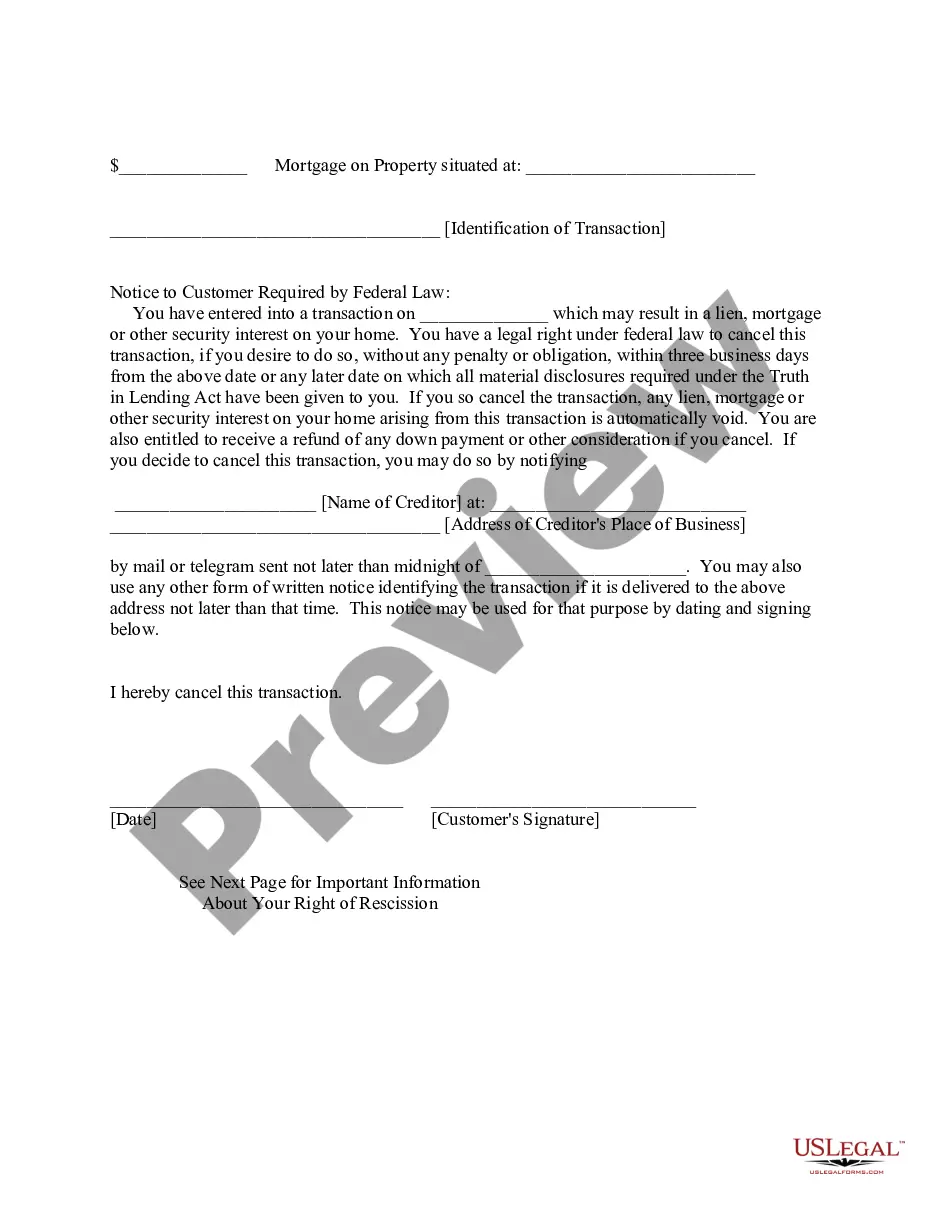

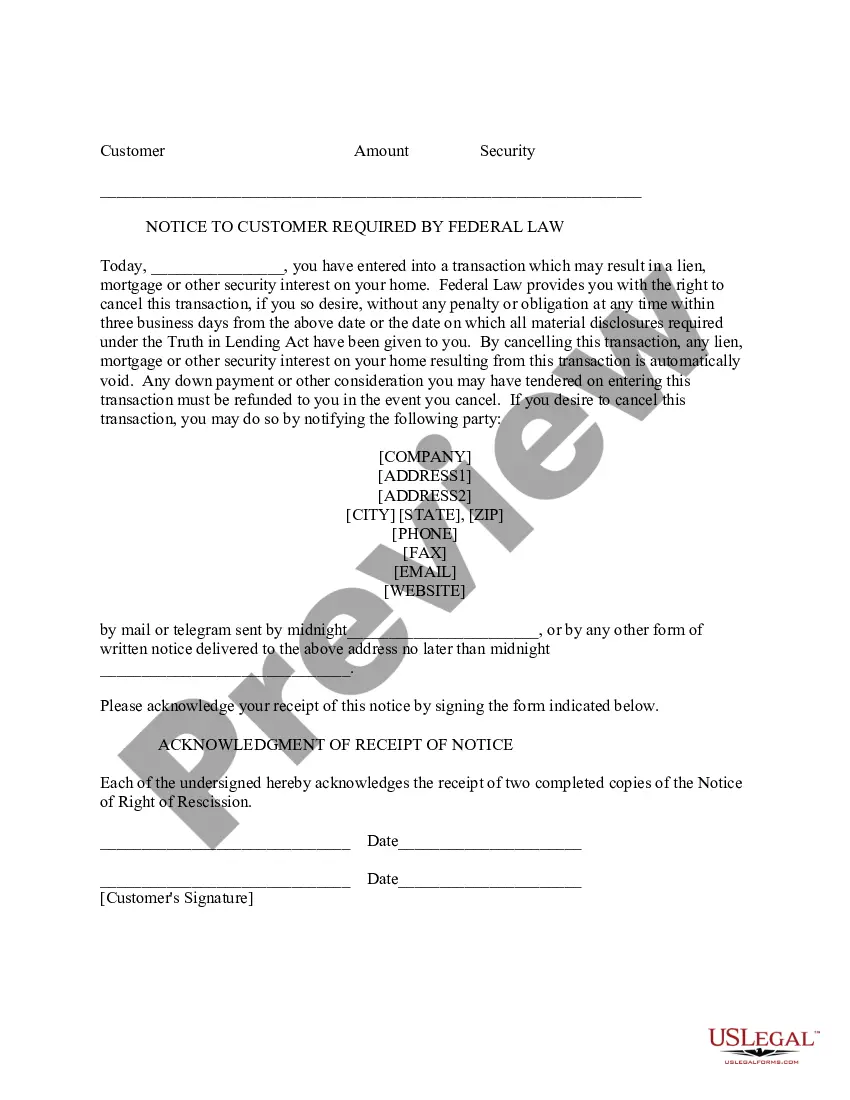

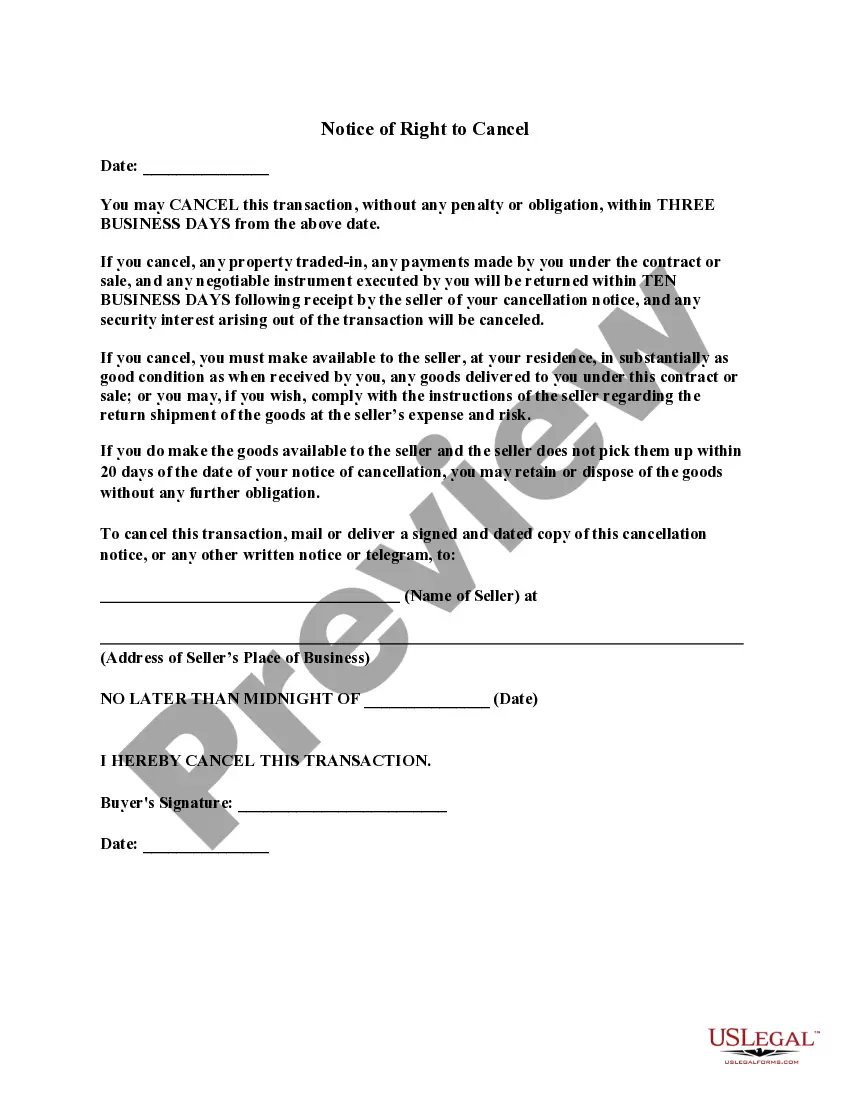

According to 12 CFR 226.23, in a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership interest is or will be subject to the security interest shall have the right to rescind the transaction, with some exceptions. To exercise the right to rescind, the consumer shall notify the creditor of the rescission by mail, telegram or other means of written communication. Notice is considered given when mailed, when filed for telegraphic transmission or, if sent by other means, when delivered to the creditor's designated place of business. The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice

required by paragraph (b) of this section, or delivery of all material disclosures, whichever occurs last.

Minnesota Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien or Security Interest on Borrowers' Residence

Description

How to fill out Notice Of Right Of Rescission Or Right To Cancel Regarding Mortgage, Lien Or Security Interest On Borrowers' Residence?

If you wish to complete, obtain, or print legal file layouts, use US Legal Forms, the largest variety of legal forms, which can be found on the Internet. Utilize the site`s basic and practical research to discover the paperwork you will need. Different layouts for enterprise and specific functions are categorized by groups and suggests, or search phrases. Use US Legal Forms to discover the Minnesota Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien or Security Interest on Borrowers' Residence in just a handful of clicks.

In case you are currently a US Legal Forms client, log in to your accounts and click on the Download key to find the Minnesota Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien or Security Interest on Borrowers' Residence. Also you can entry forms you in the past downloaded from the My Forms tab of your own accounts.

Should you use US Legal Forms initially, follow the instructions under:

- Step 1. Be sure you have selected the form to the right area/nation.

- Step 2. Utilize the Preview solution to examine the form`s articles. Do not overlook to read the information.

- Step 3. In case you are not satisfied with all the develop, use the Lookup area near the top of the monitor to get other variations of your legal develop format.

- Step 4. Once you have found the form you will need, go through the Purchase now key. Pick the pricing plan you like and add your accreditations to register on an accounts.

- Step 5. Approach the deal. You can use your bank card or PayPal accounts to finish the deal.

- Step 6. Choose the formatting of your legal develop and obtain it on your own device.

- Step 7. Complete, change and print or signal the Minnesota Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien or Security Interest on Borrowers' Residence.

Each and every legal file format you purchase is yours permanently. You possess acces to every develop you downloaded inside your acccount. Click the My Forms portion and pick a develop to print or obtain again.

Contend and obtain, and print the Minnesota Notice of Right of Rescission or Right to Cancel regarding Mortgage, Lien or Security Interest on Borrowers' Residence with US Legal Forms. There are many professional and condition-distinct forms you can utilize for the enterprise or specific demands.

Form popularity

FAQ

What is the purpose of a Notice of Right to Cancel form? Under federal law, some ? but not all ? mortgages include a right of rescission, which gives the borrower 3 business days following the signing of a loan document package to review the terms of the transaction and cancel the transaction.

If you are buying a home with a mortgage, you do not have a right to cancel the loan once the closing documents are signed. If you are refinancing a mortgage, you have until midnight of the third business day after the transaction to rescind (cancel) the mortgage contract.

In general, a lender cannot cancel a loan after closing unless there are specific circumstances outlined in the loan agreement or if fraud or misrepresentation is discovered. Once the loan has been closed and funded, the lender has typically committed the funds and established the mortgage lien on the property.

A purchaser has an unconditional right to rescind any contract, agreement, or other evidence of indebtedness, or revoke any offer, at any time prior to or within five days after the date the purchaser actually receives a legible copy of the binding contract, agreement, or other evidence of indebtedness or offer and the ...

Each consumer entitled to rescind must be given two copies of the rescission notice and the material disclosures.

The right of rescission doesn't apply when you're buying a home, and it only applies to a loan against your primary residence. So, for instance, you won't be able to rescind your mortgage if you're buying or refinancing a second home, vacation home, or investment property.

If you are buying a home with a mortgage, you do not have a right to cancel the loan once the closing documents are signed. If you are refinancing a mortgage, you have until midnight of the third business day after the transaction to rescind (cancel) the mortgage contract.

If you're taking out a home equity loan, home equity line of credit (HELOC), or refinancing your home loan with a different lender, you have three days from when you sign the contract to rescind the deal. This is known as the right of rescission.