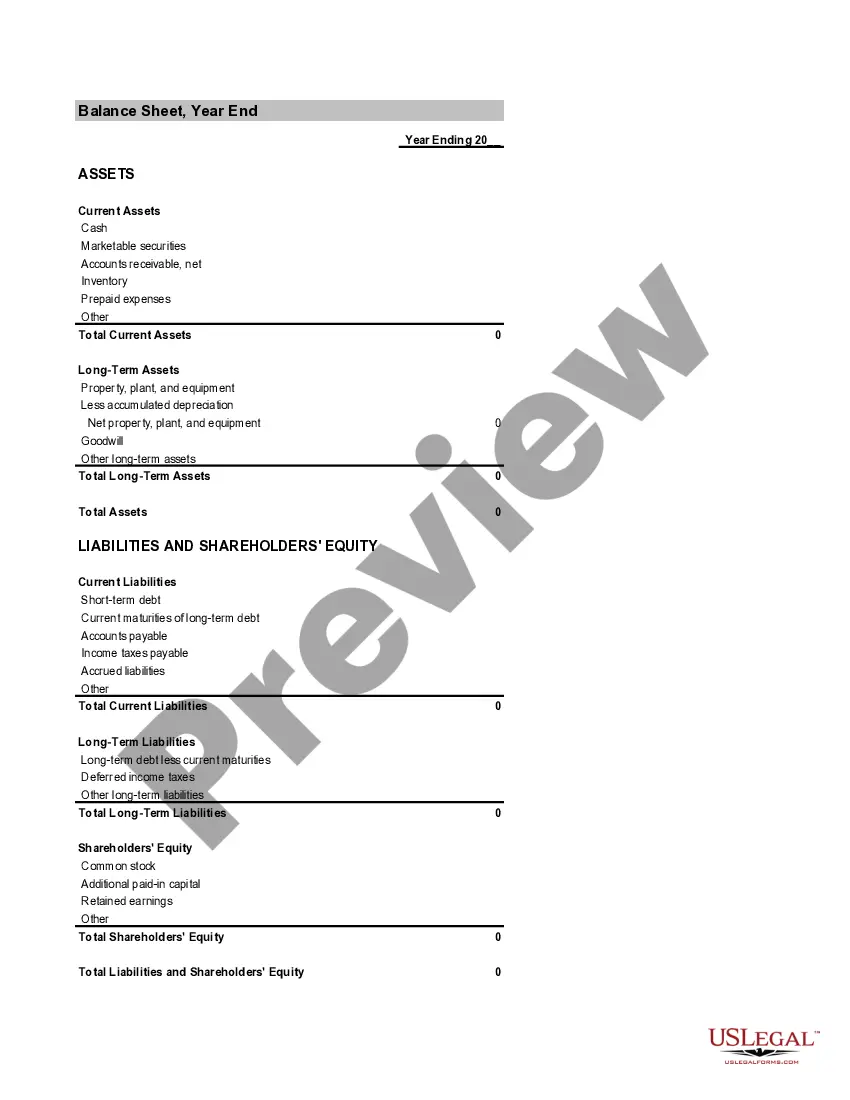

Minnesota Summary of Account for Inventory of Business

Description

How to fill out Summary Of Account For Inventory Of Business?

You may devote hours on the web trying to find the legitimate file format that fits the state and federal demands you require. US Legal Forms offers a large number of legitimate kinds which are analyzed by pros. You can easily download or print the Minnesota Summary of Account for Inventory of Business from the assistance.

If you have a US Legal Forms profile, you may log in and click the Down load key. Afterward, you may full, change, print, or indicator the Minnesota Summary of Account for Inventory of Business. Every legitimate file format you purchase is your own property forever. To acquire an additional copy of the purchased type, visit the My Forms tab and click the related key.

If you are using the US Legal Forms site initially, adhere to the easy instructions beneath:

- First, make sure that you have selected the right file format for the state/town that you pick. See the type outline to make sure you have chosen the appropriate type. If offered, use the Review key to look throughout the file format too.

- If you want to locate an additional model in the type, use the Look for field to obtain the format that suits you and demands.

- Once you have discovered the format you need, click on Purchase now to carry on.

- Choose the pricing strategy you need, type in your accreditations, and register for a free account on US Legal Forms.

- Total the financial transaction. You can utilize your bank card or PayPal profile to fund the legitimate type.

- Choose the structure in the file and download it to the device.

- Make adjustments to the file if needed. You may full, change and indicator and print Minnesota Summary of Account for Inventory of Business.

Down load and print a large number of file web templates making use of the US Legal Forms website, which provides the biggest assortment of legitimate kinds. Use skilled and express-distinct web templates to tackle your small business or personal demands.

Form popularity

FAQ

An inventory write down is an accounting process that records the reduction of an inventory's value. This is required when the inventory's market value drops below its book value on the balance sheet. The write down will reduce the balance sheet value of inventory and create an expense on the income statement.

Impairment is the condition that exists when the carrying amount of an asset is higher than the sum of its estimated future cash flows. The accounting standards require that all assets be tested for impairment regularly, and this includes the inventory asset.

Debit the cost of goods sold (COGS) account and credit the inventory write-off expense account. If you don't have frequently damaged inventory, you can choose to debit the cost of goods sold account and credit the inventory account to write off the loss.

Inventory initially is considered an asset to a company because it has economic value and the potential for future benefit. When inventory is written off, that process is acknowledging that the item no longer has economic value and will not provide future value to the company, thus rendering it an expense.

The journal entry would be to debit cost of good sold (a specific damage account) and the credit would be to inventory (reduce the inventory). Universal CPA is the only course that has visual learning and bite-sized video explanations for every single MCQ and simulation.

Inventory is an asset and its ending balance is reported in the current asset section of a company's balance sheet. Inventory is not an income statement account. However, the change in inventory is a component in the calculation of the Cost of Goods Sold, which is often presented on a company's income statement.

This is done by comparing the carrying amount of each item of inventory (or group of similar items) with its selling price less costs to complete and sell. Where an item of inventory (or a group of inventories) is impaired, the entity must reduce the carrying amount to its selling price less costs to complete and sell.

An inventory write-off may be recorded in one of two ways. It may be expensed directly to the cost of goods sold (COGS) account, or it may offset the inventory asset account in a contra asset account, commonly referred to as the allowance for obsolete inventory or inventory reserve.