Minnesota Collection Letter

Understanding this form

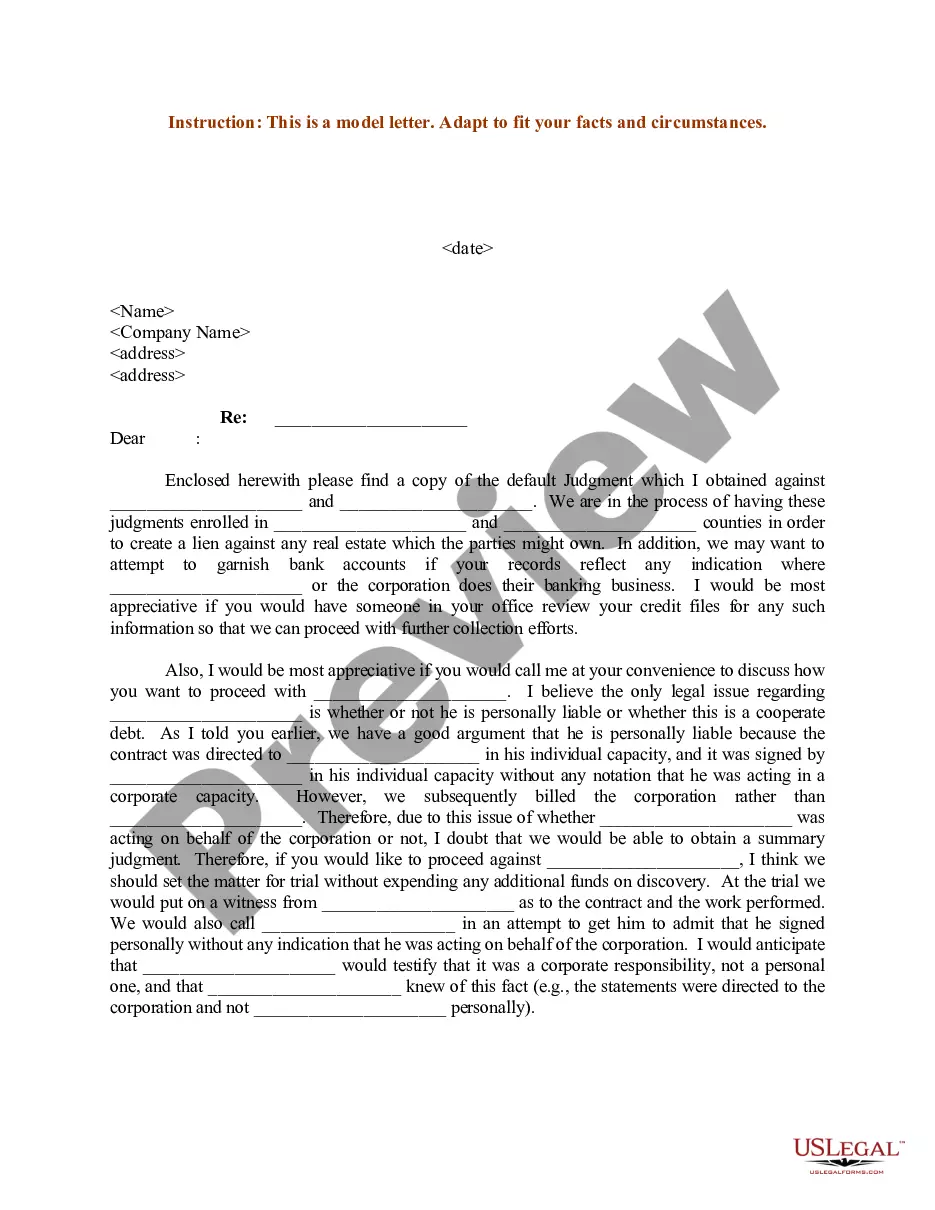

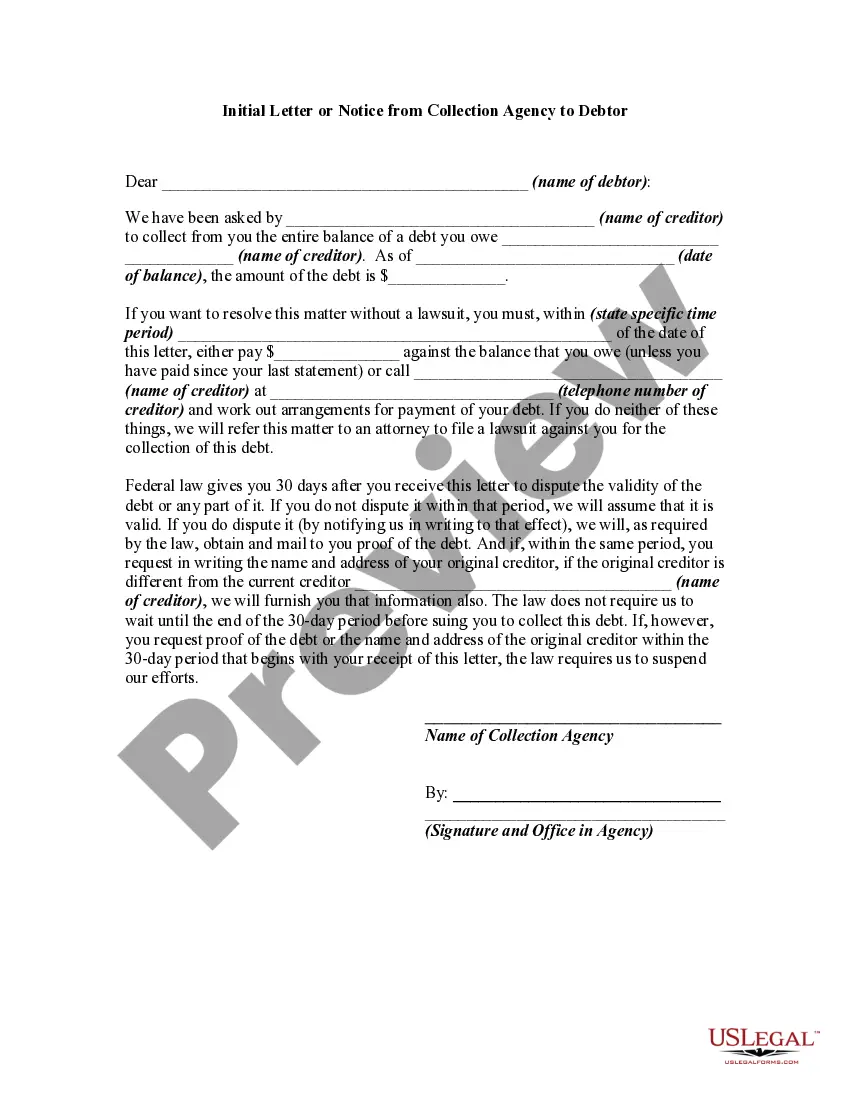

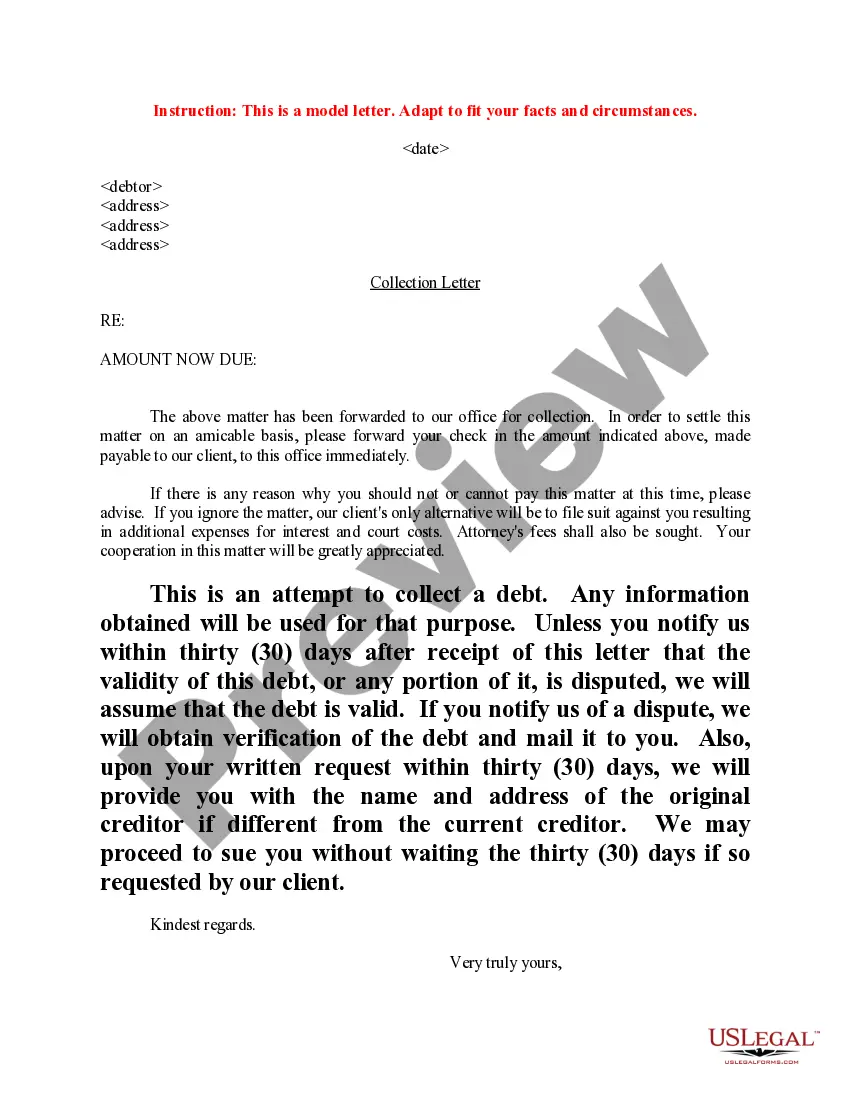

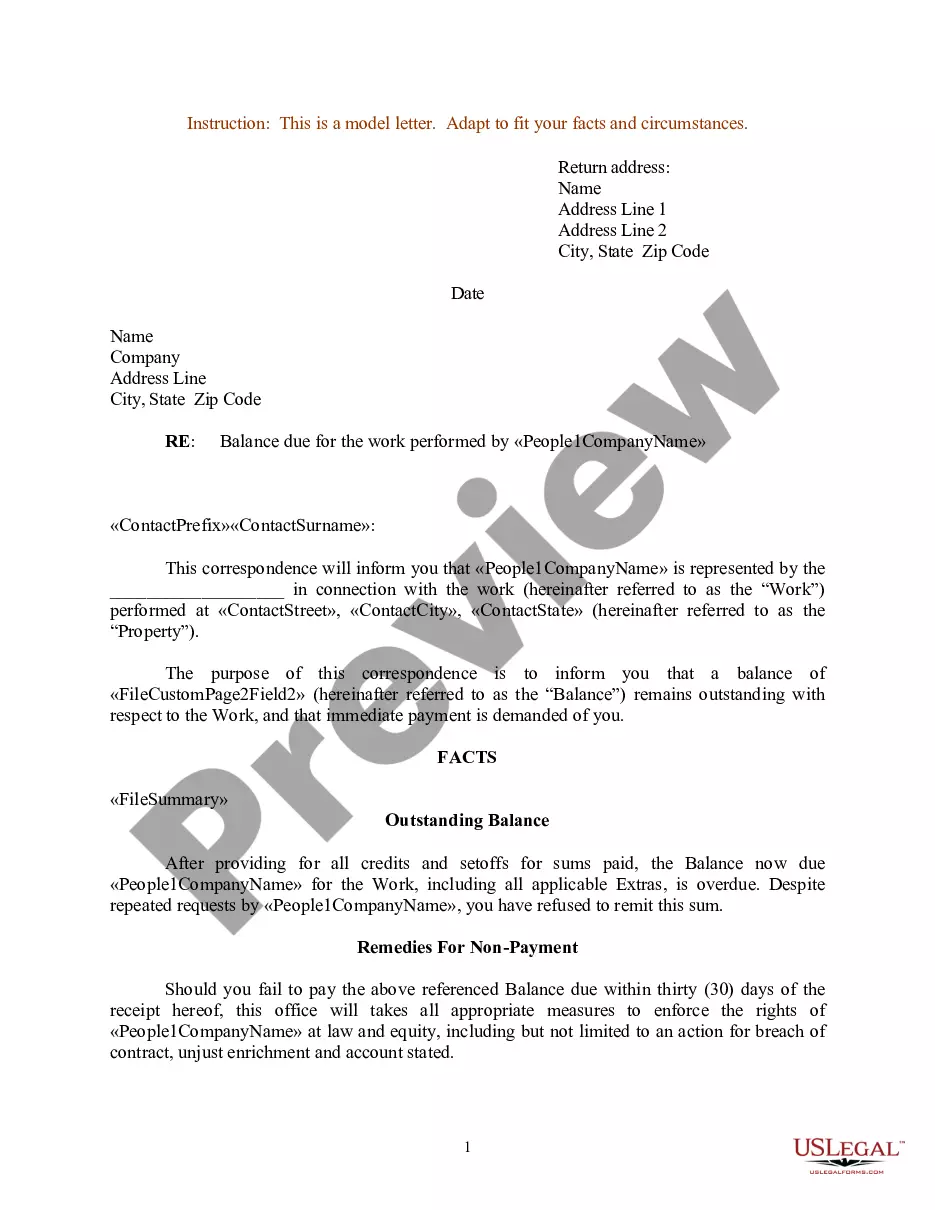

The Collection Letter is a formal communication from an attorney's office to a debtor, requesting payment for an outstanding debt. This letter serves to assert the creditor's rights while adhering to the Fair Debt Collection Act, ensuring the debtor is informed of their obligations and rights. Unlike informal reminders or calls, a Collection Letter carries legal weight and outlines possible actions if the debt is not settled promptly.

Key parts of this document

- Debtor's name and address

- Amount due, including any applicable fees

- Instructions for payment to the creditor

- Details on disputing the debt within thirty days

- Consequences for non-payment, such as legal action

When this form is needed

This form should be utilized when a creditor wishes to formally request payment from a debtor who has failed to meet financial obligations. It is appropriate in scenarios where prior attempts at informal collection have been unsuccessful, or when the creditor seeks to initiate more serious collection efforts while remaining compliant with legal requirements.

Who should use this form

- Creditors seeking to collect outstanding debts

- Attorneys representing clients in debt collection cases

- Businesses with unpaid invoices from clients

- Individuals attempting to recover personal loans or debts

How to prepare this document

- Identify the debtor by including their full name and address.

- Clearly state the amount owed, including any interest or additional fees.

- Provide payment instructions, specifying how and where to send payment.

- Include a statement regarding the debtor's rights to dispute the debt.

- Sign the letter, ensuring proper representation from the attorney or law firm.

Does this form need to be notarized?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include all necessary contact information for the creditor.

- Not clearly stating the total amount owed.

- Neglecting to inform the debtor of their rights to dispute the debt.

- Using aggressive language that may violate the Fair Debt Collection Act.

Advantages of online completion

- Easy access to legally vetted templates prepared by licensed attorneys.

- Convenient downloading options that allow for immediate use.

- Editable fields to personalize the document to specific situations.

- Assurance of compliance with legal standards for debt collection letters.

Legal use & context

- The Collection Letter is an important tool in the debt collection process.

- It is necessary to adhere to the Fair Debt Collection Act to avoid legal repercussions.

- This form can be a precursor to further collection actions, such as filing a lawsuit.

Main things to remember

- The Collection Letter formally requests payment and outlines debtor rights.

- It serves as a warning of potential legal action for unresolved debts.

- Understanding the proper completion process is crucial for effectiveness.

Looking for another form?

Form popularity

FAQ

In Minnesota, a debt generally becomes uncollectible after six years, depending on the type of debt. This means that creditors can no longer pursue legal action to collect it. By understanding this timeline, you can better strategize your financial plans and debt management.

To obtain a debt letter, you can request a Minnesota Collection Letter directly from the creditor or collection agency handling your account. It's important to ask for this letter if you have not received one, as it contains valuable information about the debt. Having this documentation can assist you in managing your obligations and making informed decisions.

Yes, collection agencies must send you a debt validation letter after they contact you about an unpaid debt. This letter, often referred to as a Minnesota Collection Letter, provides essential details about the debt, including the amount owed and the original creditor. Receiving this information helps you verify the debt and understand your options.

In Minnesota, the statute of limitations typically allows creditors six years to collect most debts. After this period, the debt becomes uncollectible, meaning creditors cannot take legal action. It's essential to understand this timeframe, as it can influence how you manage your finances and any outstanding debts.

Collection laws in Minnesota regulate how creditors can collect debts. These laws protect consumers from unfair practices and require lenders to provide written notification, often in the form of a Minnesota Collection Letter. Understanding these laws can help you navigate your rights and responsibilities when dealing with debt.

The statute of limitations for bringing a lawsuit for breach of contract under Minnesota law is six (6) years. This means that a creditor or debt collector can sue you anytime within six (6) years from the date of your last purchase or last payment, whichever was later.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

You'll get notices and possibly calls seeking payment. At some point, usually after 180 days, the creditor such as a credit card company, bank or medical provider gives up on trying to collect. The original creditor may then sell the debt to a collections agency to recoup losses.

In most cases, the statute of limitations for a debt will have passed after 10 years. This means that a debt collector may still attempt to pursue it, but they can't typically take legal action against you.

The time limits for civil claims and other actions in Minnesota vary from two years for personal injury claims to 10 years for judgments. Fraud, injury to personal property, and trespassing claims have a six-year statute of limitations, as do both written and oral contracts.