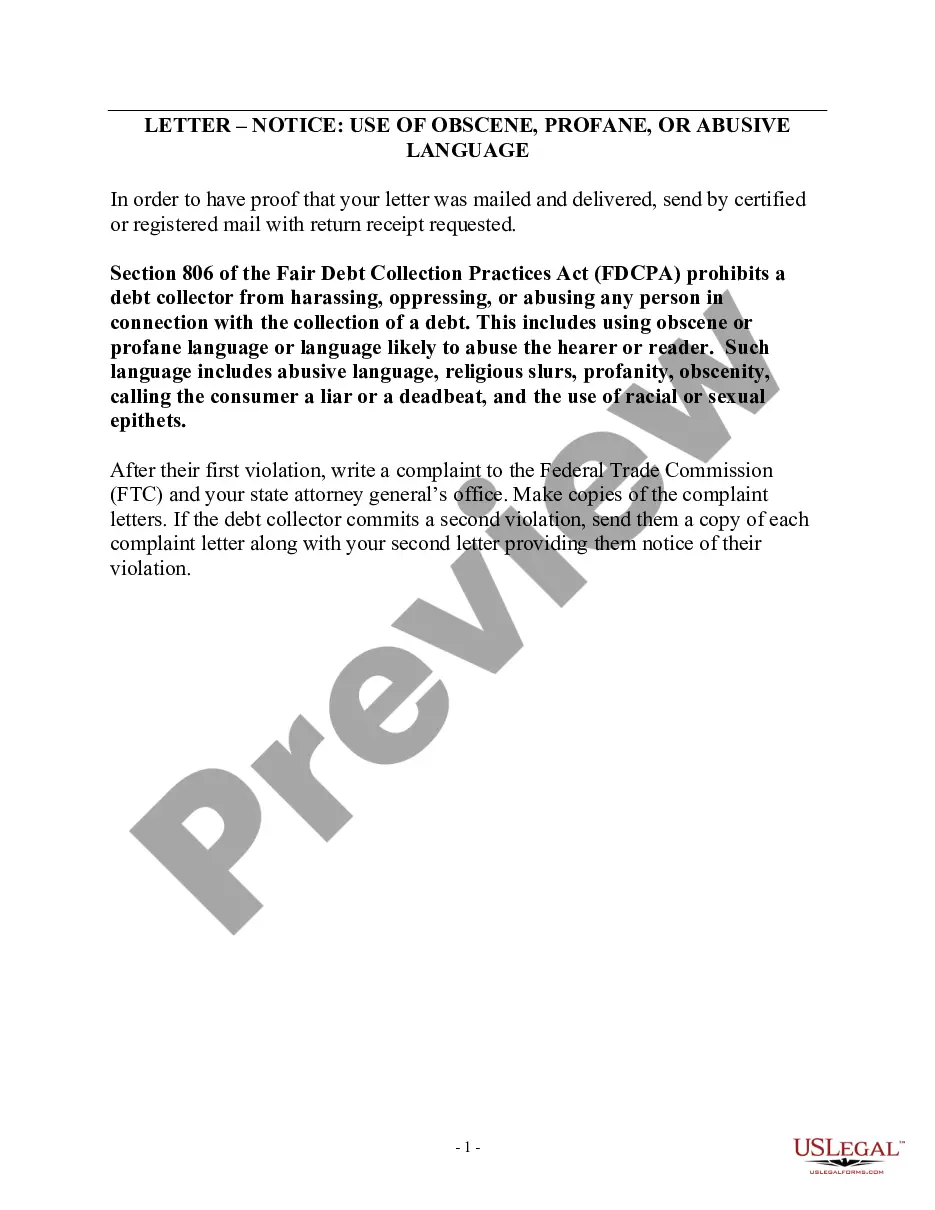

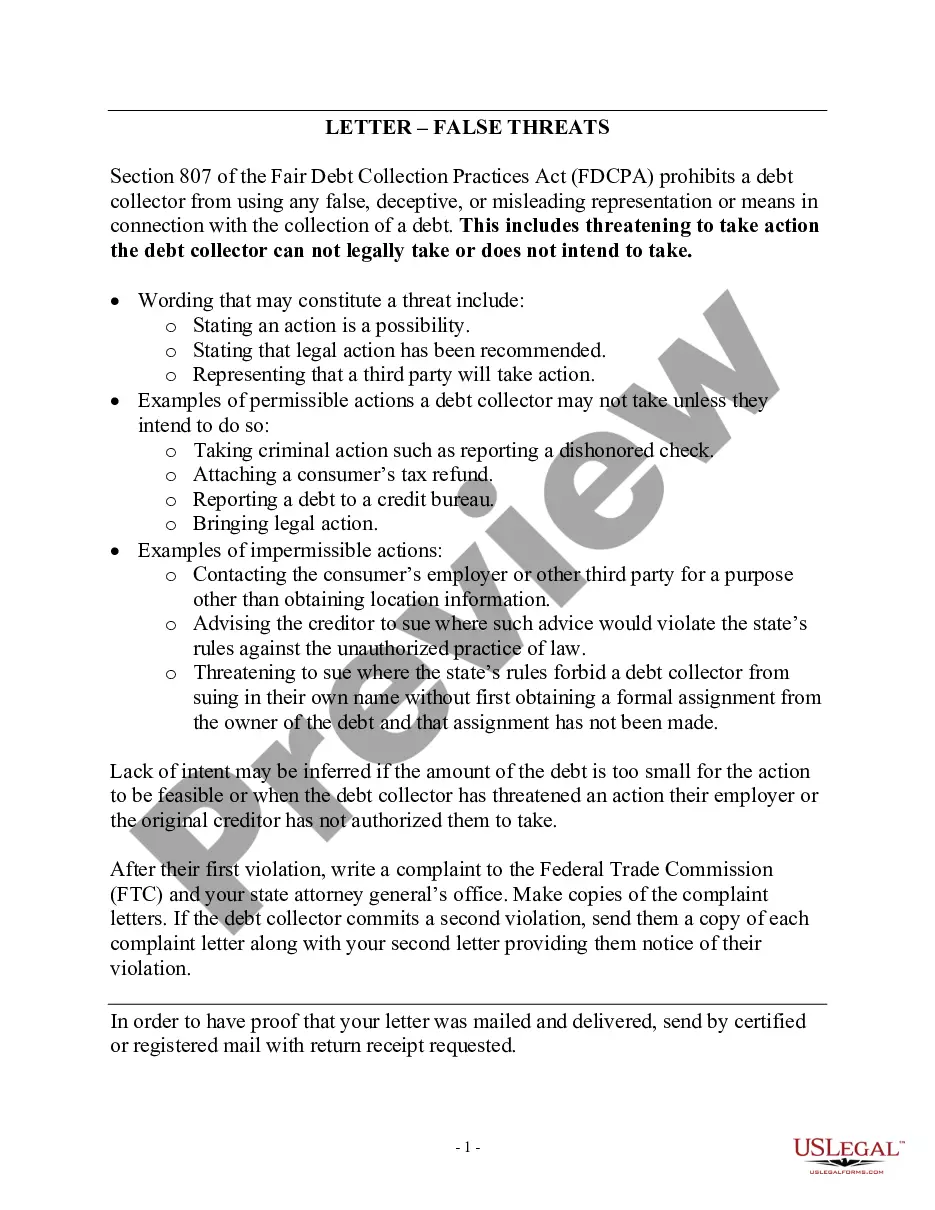

This form is a follow-up letter containing a warning that the debt collector's continued violation of the Fair Debt Collection Practices Act may result in a law suit being filed against the debt collector.

Maryland Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor

Category:

State:

Multi-State

Control #:

US-DCPA-18.2BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Second Notice To Debt Collector Of Harassment Or Abuse In Collection Activities Involving Threats To Use Violence Or Other Criminal Means To Harm The Physical Person, Reputation, And/or Property Of The Debtor?

It is feasible to devote hours online searching for the legal document format that meets the federal and state requirements you have.

US Legal Forms offers a wide array of legal documents that are reviewed by experts.

You can effortlessly download or print the Maryland Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor from my service.

- If you already possess a US Legal Forms account, you may Log In and select the Acquire button.

- After that, you can fill out, modify, print, or sign the Maryland Second Notice to Debt Collector of Harassment or Abuse in Collection Activities Involving Threats to Use Violence or other Criminal Means to Harm the Physical Person, Reputation, and/or Property of the Debtor.

- Each legal document format you obtain is yours indefinitely.

- To obtain another version of any purchased template, navigate to the My documents tab and click the appropriate button.

- If you are visiting the US Legal Forms website for the first time, follow the simple instructions provided below.

- First, make sure you have selected the correct document format for the region/area of your choice.

- Check the template description to confirm you have chosen the right one.

- If available, utilize the Review button to examine the document format accordingly.

- Should you wish to find another edition of the template, use the Lookup field to find the format that suits you and your requirements.

Form popularity

FAQ

Debt Collectors Can't Call You Repeatedly to Harass You This means that while the FDCPA doesn't place a specific limit on the number of calls debt collectors can make, it prohibits them from calling you multiple times just to harass you. (15 U.S. Code §? 1692d).

Also, debt collectors can't call you numerous times a day. Doing so is considered a form of harassment by the Federal Trade Commission (FTC) and is explicitly not allowed.

It is Legal for a Debt Collector to Contact Your Family Typically, debt collectors are allowed to contact each family member, but only once. The only case where they may do so again is if they believe the information given to them was false.

Federal law doesn't give a specific limit on the number of calls a debt collector can place to you. A debt collector may not call you repeatedly or continuously intending to annoy, abuse, or harass you or others who share the number.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

No harassment The Fair Debt Collection Practices Act (FDCPA) says debt collectors can't harass, oppress, or abuse you or anyone else they contact. Some examples of harassment are: Repetitious phone calls that are intended to annoy, abuse, or harass you or any person answering the phone. Obscene or profane language.

A debt collector can't harass you Now, for a few rules that apply to any debt collector, including collection agents. First, they can't communicate with you in a way that amounts to harassment. Harassment can include: using threatening, intimidating, or profane language.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

The definition of debt collection harassment is to intimidate, abuse, coerce, bully or browbeat consumers into paying off debt. This happens most often over the phone, but harassment could come in the form of emails, texts, direct mail or talking to friends or neighbors about your debt.