Maryland Approval of employee stock purchase plan for The American Annuity Group, Inc.

Description

How to fill out Approval Of Employee Stock Purchase Plan For The American Annuity Group, Inc.?

Are you in the place in which you need paperwork for either business or specific functions almost every day time? There are a variety of legitimate papers themes accessible on the Internet, but finding ones you can depend on is not simple. US Legal Forms offers 1000s of type themes, much like the Maryland Approval of employee stock purchase plan for The American Annuity Group, Inc., which can be published in order to meet federal and state needs.

Should you be currently familiar with US Legal Forms website and have an account, basically log in. Following that, you may acquire the Maryland Approval of employee stock purchase plan for The American Annuity Group, Inc. design.

Unless you provide an profile and wish to start using US Legal Forms, adopt these measures:

- Get the type you want and ensure it is for your proper town/county.

- Take advantage of the Review key to check the shape.

- Browse the outline to actually have chosen the correct type.

- If the type is not what you are trying to find, make use of the Lookup industry to obtain the type that meets your requirements and needs.

- Whenever you get the proper type, just click Get now.

- Opt for the costs program you would like, submit the specified information and facts to create your account, and pay money for the transaction with your PayPal or bank card.

- Select a practical data file structure and acquire your version.

Locate all of the papers themes you have bought in the My Forms food selection. You can aquire a additional version of Maryland Approval of employee stock purchase plan for The American Annuity Group, Inc. any time, if possible. Just select the needed type to acquire or printing the papers design.

Use US Legal Forms, one of the most substantial variety of legitimate kinds, to conserve time and prevent mistakes. The support offers appropriately produced legitimate papers themes which can be used for a variety of functions. Create an account on US Legal Forms and start producing your life easier.

Form popularity

FAQ

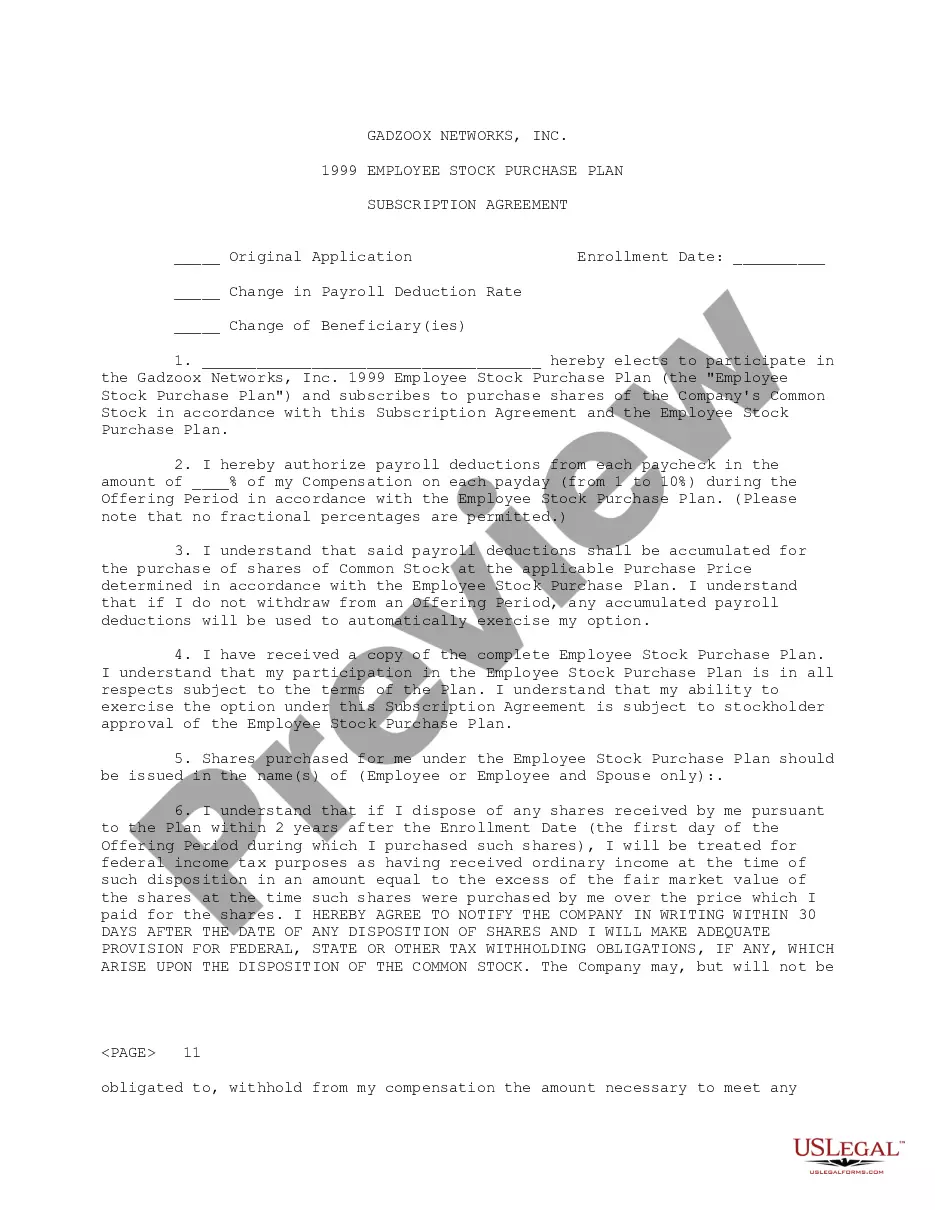

Employee Stock Purchase Plan: Qualified or Non-qualified Now, we can have a look at the key difference between the two types. An ESPP qualified plan is designed and operates ing to Internal Revenue Section (IRS) 423 regulations, whereas a non-qualified ESPP does not meet those criteria.

Employee Stock Purchase Plans (ESPPs) are widely regarded as one of the most simple and straightforward equity compensation strategies available to businesses today. There are two major types of ESPP: 1) Qualified ESPP offering tax advantages and 2) Non-qualified ESPP offering flexibility.

Section 423 of the Code permits a plan to exclude employees who have been employed for less than two years or who are employed for less than 20 hours per week or five months per year. Also, owners of 5% or more of the common stock of a company by statute are not permitted to participate.

Yes, you can sell stock purchased through your ESPP plan immediately if you want to guarantee that you profit from your discount. Otherwise, the value of the stock may go up, which increases your profit, or it may go down, causing you to lose money.

An ESPP must be approved by the stockholders of the sponsoring corporation within the period commencing 12 months before and ending 12 months after the ESPP is adopted by the sponsoring corporation's board of directors.

To be eligible for a Section 423 ESPP, you must be an employee from the start of the offering until at least three months before the purchase date (12 months for termination because of disability). However, most companies end participation when you terminate employment.

You may withdraw from the ESPP by notifying Fidelity and completing a withdrawal election. When you withdraw, all of the contributions accumulated in your account will be returned to you as soon as administratively possible and you will not be able to make any further contributions during that offering period.

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.