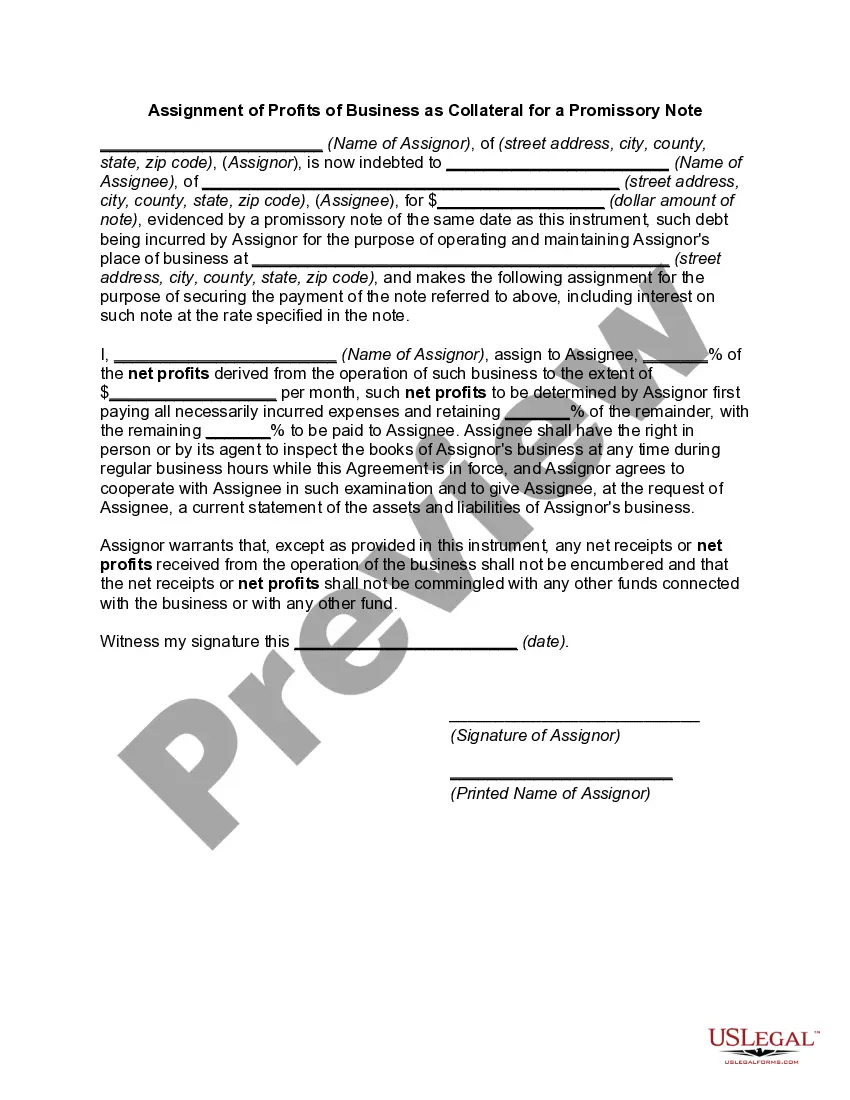

Massachusetts Assignment of Profits of Business

Description

How to fill out Assignment Of Profits Of Business?

US Legal Forms - one of the largest repositories of legal documents in the United States - offers a diverse selection of legal document formats that you can download or print.

By using the website, you can access thousands of documents for business and personal use, organized by categories, states, or keywords. You can find the latest versions of documents like the Massachusetts Assignment of Profits of Business in no time.

If you already have a monthly subscription, Log In to download the Massachusetts Assignment of Profits of Business from your US Legal Forms library. The Download button will be visible on every document you view. You have access to all previously obtained documents in the My documents section of your account.

Complete the transaction. Use your Visa, Mastercard, or PayPal account to finalize the purchase.

Select the format and download the document to your device. Edit. Complete, modify, print, and sign the downloaded Massachusetts Assignment of Profits of Business.

Every template added to your account does not expire and is yours permanently. So, if you need to download or print another copy, simply go to the My documents section and click on the document you need.

Access the Massachusetts Assignment of Profits of Business with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal requirements.

- If you are using US Legal Forms for the first time, follow these simple steps to get started.

- Ensure you have chosen the correct document for the city/region. Click the Preview button to review the document's content.

- Check the document details to confirm that you have selected the right one.

- If the document does not meet your needs, use the Search box at the top of the screen to find the one that does.

- If you are satisfied with the document, confirm your selection by clicking on the Purchase now button.

- Then, select the pricing plan you prefer and provide your information to register for an account.

Form popularity

FAQ

The Massachusetts Department of Revenue (DOR) oversees tax collection and enforcement in the state. The DOR administers various tax laws, including income and sales tax, and provides guidance on compliance. Understanding its role is vital for business owners, especially when managing the Massachusetts Assignment of Profits of Business.

Apportionment is the determination of the percentage of a business' profits subject to a given jurisdiction's corporate income or other business taxes. U.S. states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders.

A corporation that is so engaged in manufacturing and whose manufacturing activities are substantial is a section 38 manufacturer for the taxable year regardless of whether, or to what extent, it conducts its manufacturing activities in Massachusetts.

But effective this year Massachusetts has adopted market-based sourcing which regards as Massachusetts sales: Sales of services to the extent delivered to a location in Massachusetts; and. Receipts from intangible property to the extent used in Massachusetts.

1. For Massachusetts tax purposes, a taxpayer's income subject to apportionment is its entire income derived from its related business activities within and outside of Massachusetts not including any allocable items of income that either are or are not subject to the tax jurisdiction of Massachusetts.

Rather than seeking to assign all sales to the states in which the company operates, the throwout rule simply excludes from overall sales any sales that are not assigned to any state.

There are three states that have a throwout rule:Louisiana.Maine.West Virginia.29-Oct-2019

Massachusetts source income includes items of gross income derived from or effectively connected with any trade or business, including any employment, carried on by the taxpayer in Massachusetts, whether or not the non-resident is actively engaged in a trade or business or employment in Massachusetts in the year in

Under the secondary (throwback) rule, a sale is in Massachusetts if the seller is not taxable in the state where the property sold is delivered to the purchaser, and the property is not sold by an agent of the seller who is chiefly situated at, connected with, or sent out from the Seller's owned or rented business

While the Legislature included a throwout rule for sales sourced to a state where the taxpayer is not subject to taxation, Massachusetts has defined subject to taxation very broadly, and few, if any, taxpayers should end up throwing out receipts from sales of services or intangibles on the basis that the receipts