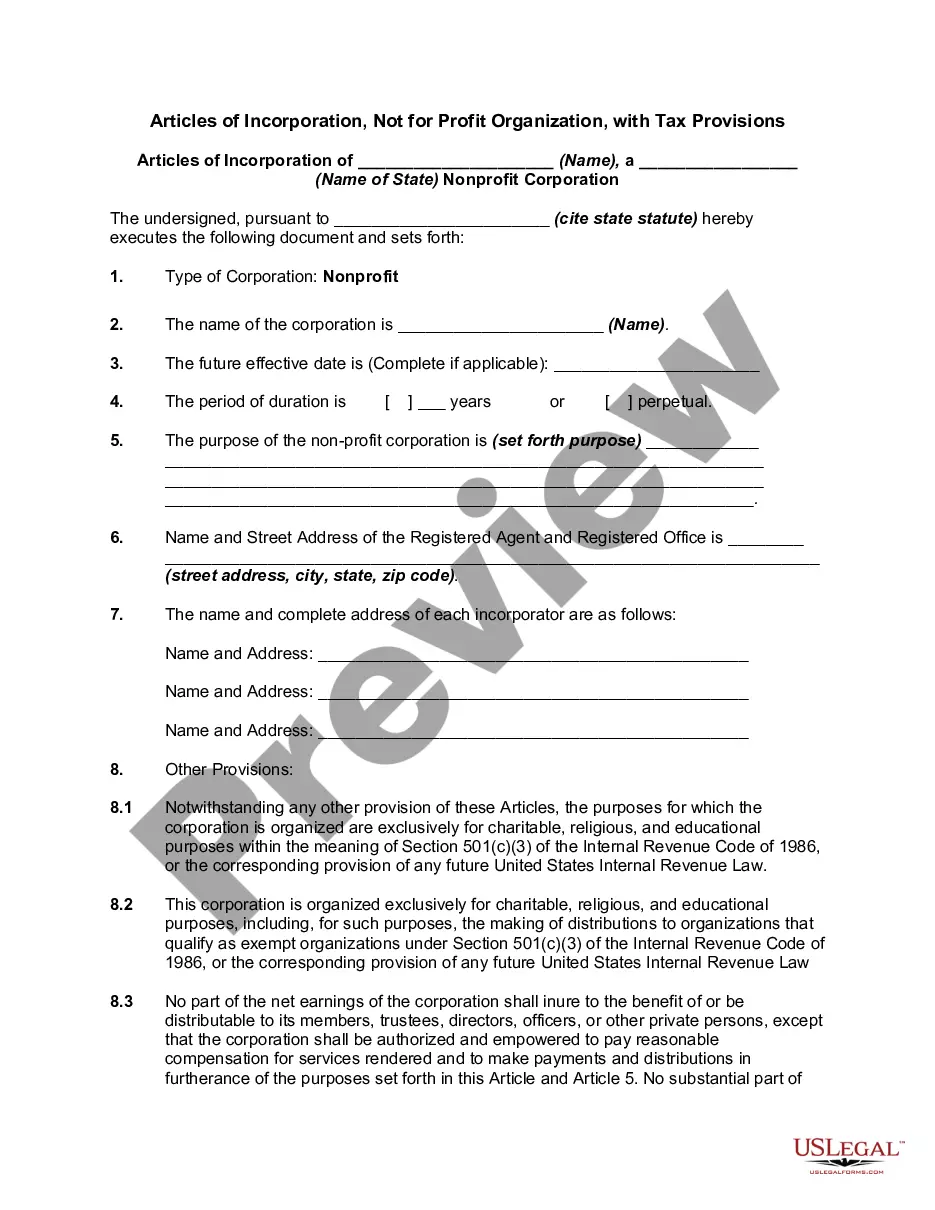

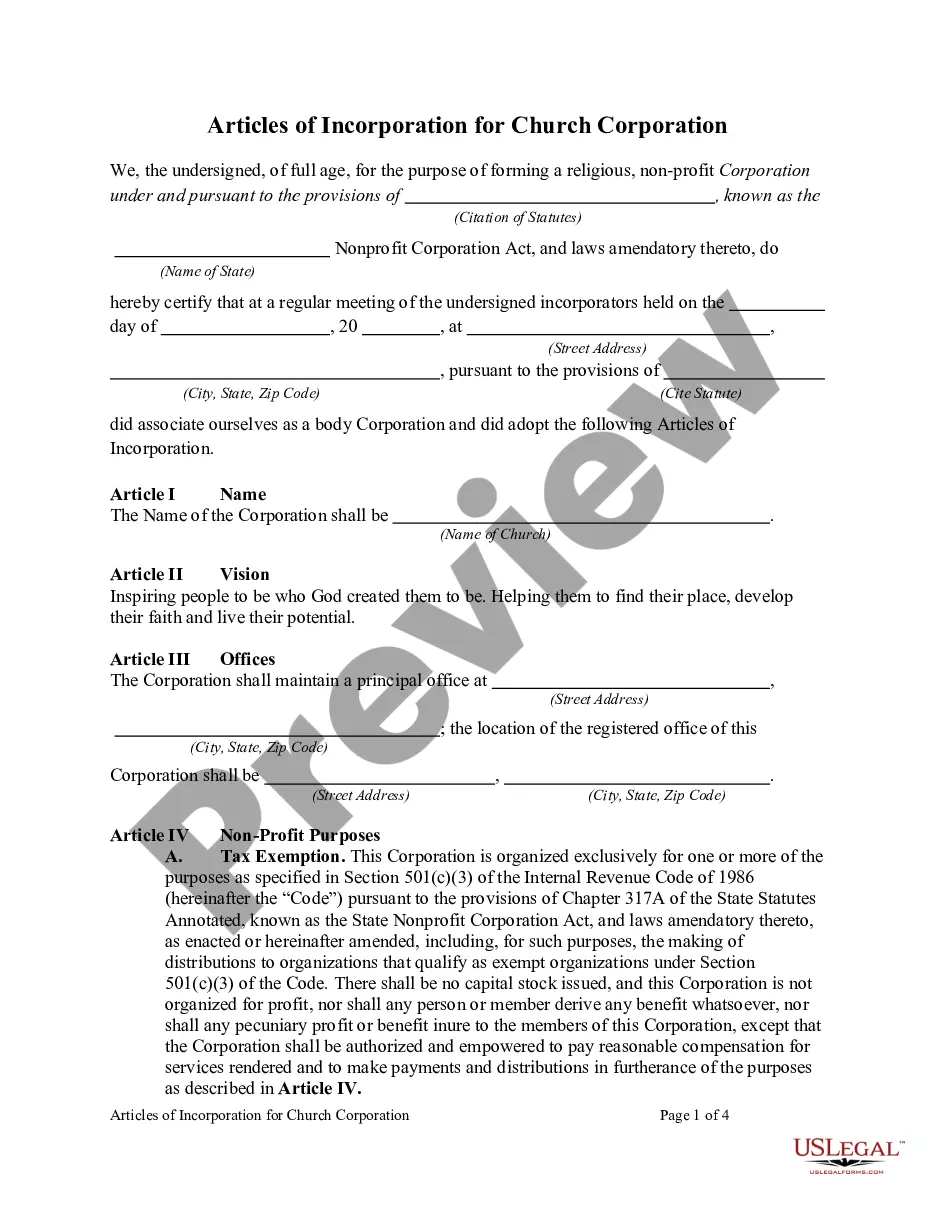

A nonprofit corporation is one that is organized for charitable or benevolent purposes. These corporations include certain hospitals, universities, churches, and other religious organizations. A nonprofit entity does not have to be a nonprofit corporation, however. Nonprofit corporations do not have shareholders, but have members or a perpetual board of directors or board of trustees.

Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions

Category:

State:

Multi-State

Control #:

US-04518BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Articles Of Incorporation For Non-Profit Organization, With Tax Provisions?

Have you ever been in a situation where you require documentation for both organizational and specific purposes almost daily.

There are numerous legal document templates available online, but finding ones you can trust is not simple.

US Legal Forms offers thousands of template forms, such as the Massachusetts Articles of Incorporation for a Non-Profit Organization, with Tax Provisions, that are designed to meet state and federal requirements.

Once you find the appropriate form, click Purchase now.

Choose the pricing plan you need, complete the required information to create your account, and purchase an order using your PayPal or Visa or Mastercard. Select a convenient paper format and download your copy. Access all the document templates you have purchased in the My documents menu. You can obtain an additional copy of the Massachusetts Articles of Incorporation for a Non-Profit Organization, with Tax Provisions at any time if necessary. Simply click the desired form to download or print the template. Use US Legal Forms, the most extensive collection of legal forms, to save time and avoid mistakes. The service provides professionally created legal document templates that you can use for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and possess an account, just Log In.

- After that, you can download the Massachusetts Articles of Incorporation for a Non-Profit Organization, with Tax Provisions template.

- If you do not have an account and wish to begin using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is for the correct city/region.

- Utilize the Preview button to examine the form.

- Check the outline to confirm that you have selected the correct form.

- If the form does not meet your requirements, use the Lookup field to find the form that satisfies your needs and specifications.

Form popularity

FAQ

Creating articles of incorporation for a nonprofit involves several key steps. First, gather your organization’s name, purpose, and information about the initial directors. Next, use a reliable resource like US Legal Forms to access templates for the Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions. Completing this document accurately will help ensure your nonprofit is legally established and compliant with state laws.

To obtain the Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions, you can visit the Massachusetts Secretary of the Commonwealth's website or utilize legal document services like US Legal Forms. These platforms provide templates and guidance to help you accurately fill out the necessary information. After preparing your document, you will file it with the state for approval.

In Massachusetts, nonprofits must file the Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions. This document officially establishes your nonprofit and outlines its purpose, structure, and governance. It is essential to include the appropriate tax provisions to ensure compliance with state regulations. Completing this step correctly sets the foundation for your organization's legal recognition.

In Massachusetts, non-profits can apply for tax-exempt status under certain conditions, which is a significant benefit. Typically, organizations must qualify under IRS 501(c)(3) regulations to gain tax exemptions. This status enables non-profits to operate with financial advantages, enhancing their ability to fulfill their missions. For detailed guidance, uslegalforms provides valuable resources to help navigate tax provisions.

An article of incorporation typically includes the organization's name, its purpose, and the registered agent's information. For instance, a non-profit organization stating its mission and how it plans to operate can be regarded as a clear example of articles of incorporation. When preparing your documents, ensure they comply with requirements for Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions.

Writing articles of incorporation for a non-profit involves outlining the organization’s name, purpose, and structure. You should include provisions about the management and the distribution of assets upon dissolution. To ensure compliance with state laws, especially related to Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions, you may find it beneficial to refer to uslegalforms for precise templates and support.

Yes, you can write your own articles of incorporation, but it requires careful attention to state requirements. In Massachusetts, these documents must contain specific information, including the organization's purpose and structure. To ease the process, consider using services like uslegalforms, which provide templates and guidance for creating Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions.

The main difference lies in the structure and purpose. An LLC, or Limited Liability Company, is a legal structure for a business that provides personal liability protection to its owners. On the other hand, articles of organization specifically refer to the documents filed to create the LLC. When considering Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions, it's important to understand these concepts to ensure you select the right formation for your needs.

Creating articles of incorporation for a nonprofit involves several important steps. Start by drafting a document that includes your nonprofit's name, purpose, and structure. Ensure you comply with Massachusetts law by including tax provisions relevant to non profits. To simplify the process, consider using platforms like uslegalforms, which provide templates and guidance specifically for Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions.

Nonprofits can be tax-exempt in Massachusetts if they meet specific criteria. Generally, organizations that serve charitable or educational purposes may qualify for tax exemptions. To achieve this status, nonprofits should file the necessary documentation, including the Massachusetts Articles of Incorporation for Non-Profit Organization, with Tax Provisions. This step not only grants tax benefits but also enhances the organization’s credibility.