Kansas Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

US Legal Forms - among the most significant libraries of legitimate varieties in America - offers a wide array of legitimate document layouts you may obtain or print. Using the internet site, you may get a huge number of varieties for organization and person functions, categorized by categories, states, or key phrases.You will discover the most recent variations of varieties much like the Kansas Construction Loan Financing Term Sheet in seconds.

If you already possess a subscription, log in and obtain Kansas Construction Loan Financing Term Sheet in the US Legal Forms catalogue. The Download key can look on every single form you view. You gain access to all in the past delivered electronically varieties within the My Forms tab of the account.

In order to use US Legal Forms initially, listed here are basic instructions to get you started off:

- Make sure you have picked out the correct form for the metropolis/area. Click on the Preview key to check the form`s information. Read the form information to ensure that you have chosen the appropriate form.

- In case the form doesn`t suit your specifications, utilize the Look for discipline near the top of the display screen to get the the one that does.

- In case you are satisfied with the shape, validate your option by clicking the Purchase now key. Then, pick the pricing plan you prefer and supply your credentials to sign up for the account.

- Process the deal. Make use of bank card or PayPal account to perform the deal.

- Choose the formatting and obtain the shape in your gadget.

- Make adjustments. Load, edit and print and indication the delivered electronically Kansas Construction Loan Financing Term Sheet.

Every design you included in your account does not have an expiration particular date which is the one you have for a long time. So, if you would like obtain or print one more duplicate, just check out the My Forms area and then click in the form you require.

Gain access to the Kansas Construction Loan Financing Term Sheet with US Legal Forms, probably the most comprehensive catalogue of legitimate document layouts. Use a huge number of skilled and state-particular layouts that satisfy your small business or person requirements and specifications.

Form popularity

FAQ

- Lender typically issues final payment jointly to borrower and the builder, so that check cannot be cashed until all parties have endorsed it and have had the opportunity to resolve any problems that may have arisen.

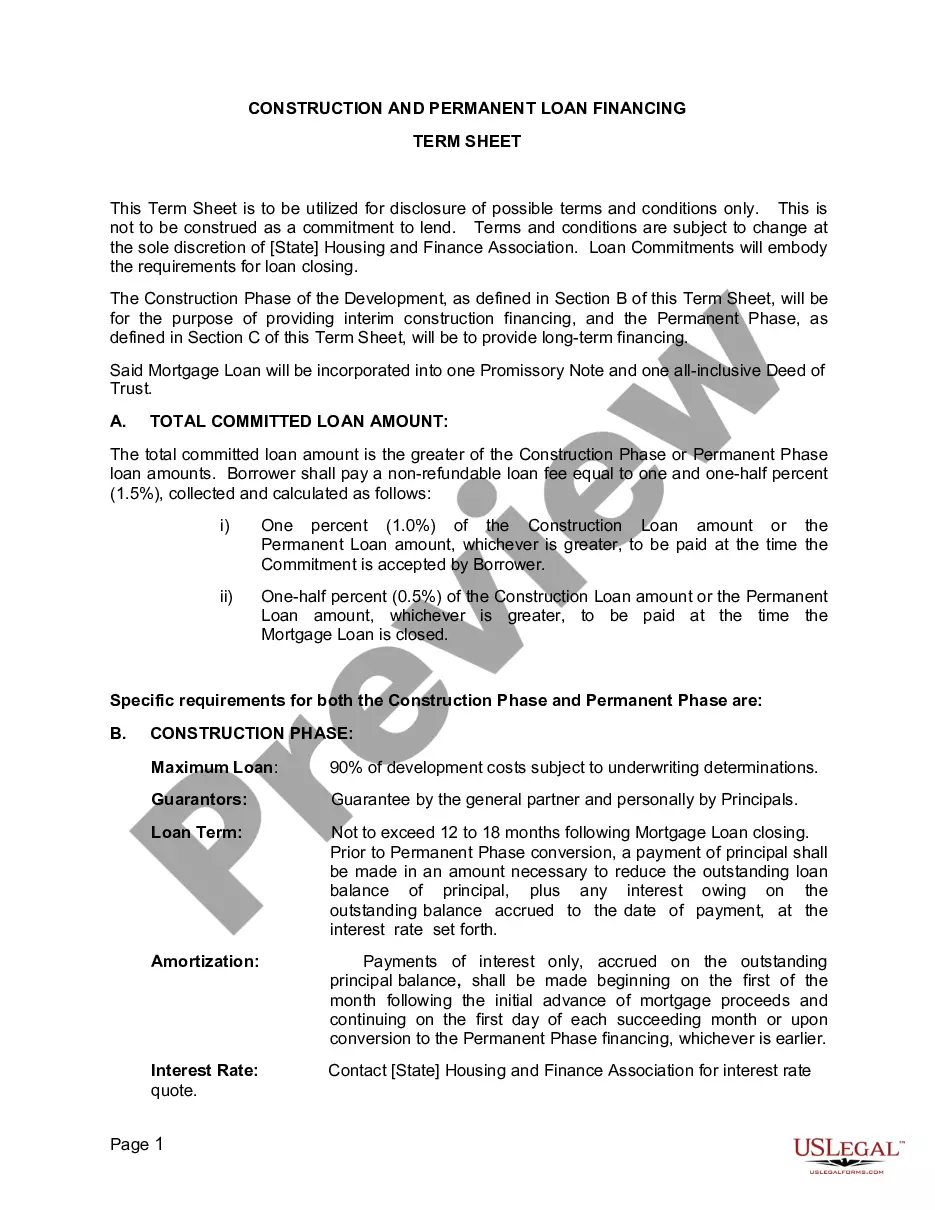

In general, construction loans have higher interest rates than longer-term mortgage loans used to purchase homes. The money borrowed through a construction loan is typically provided in a series of advances as the construction progresses.

Construction loans are usually taken out by builders or a homebuyer custom-building their own home. They are short-term loans, usually for a period of only one year.

Construction Loan Requirements Credit score: Most lenders will require you to have a minimum credit score of 620 or higher in order to qualify for a construction loan. Debt-to-income (DTI) ratio: Your lender will also look at your DTI ratio, which compares your recurring monthly debts to your gross monthly income.

TERM LENGTH Construction loans have much shorter terms than conventional mortgages. A 30-year loan may be the most common, but homebuyers have the option of selecting shorter terms depending on their bank, such as 20 or 15 years. A construction loan has a term of one year or less. The rates tend to be much higher, too.

Cons to doing a construction loan would be that payments on the construction loan begin once funds start being disbursed to the builder. With a traditional mortgage, payments don't begin until settlement. Another con is that the interest rates on construction loans are typically higher than on traditional mortgages.

Unlike traditional mortgages, which carry fixed rates, construction loans usually have variable rates that fluctuate with the prime rate. That means your monthly payment can also change, moving upward or downward based on rate changes. Construction loan rates are also typically higher than traditional mortgage rates.

Construction factoring is an increasingly popular financing option among subcontractors. It improves cash flow and provides a financial platform that can be used to grow the business. Most factoring companies finance your invoices by purchasing them rather than offering a loan.