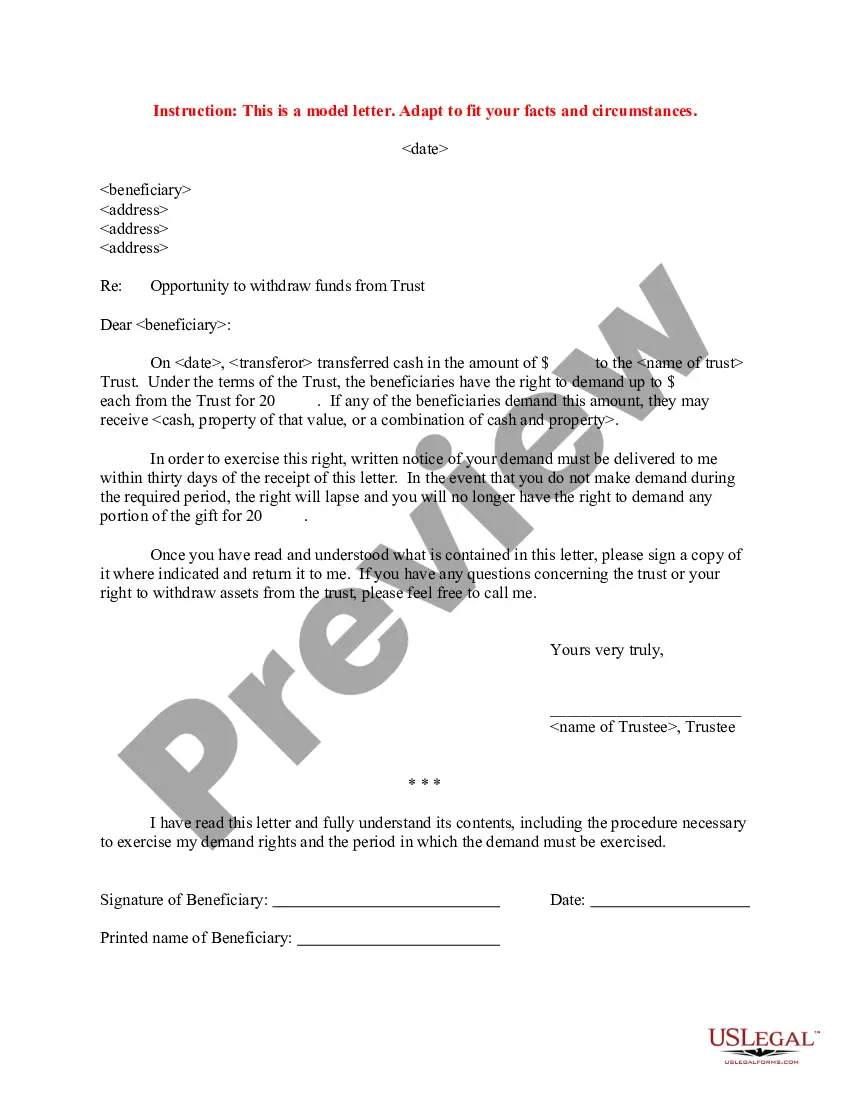

Trustee informs the trustor that he/she has the right to demand a certain amount of funds from the trust during the year. If the trustor demands a withdrawal for any of the beneficiaries, he/she may receive cash, property of that value, or a combination of cash and property.

Indiana Letter regarding trust money

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Letter Regarding Trust Money?

Are you in a scenario where you require documents for both corporate or personal tasks almost daily.

There are numerous legal document templates accessible online, but finding trustworthy versions isn't simple.

US Legal Forms provides thousands of template forms, such as the Indiana Letter regarding trust funds, designed to comply with federal and state regulations.

- If you are already familiar with the US Legal Forms site and possess an account, simply Log In.

- Then, you can download the Indiana Letter regarding trust funds template.

- If you don't have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it's for the right jurisdiction/state.

- Use the Preview button to review the document.

- Check the information to confirm that you've selected the correct form.

- If the form isn't what you're looking for, use the Search field to find the template that suits your needs and requirements.

- If you locate the correct document, click Purchase now.

- Choose the pricing plan you prefer, enter the necessary information to create your account, and pay for your order using PayPal or a credit card.

- Select a convenient file format and download your copy.

- Access all the document templates you've purchased in the My documents section. You can get an additional copy of the Indiana Letter regarding trust funds at any time. Just click on the desired form to download or print the document template.

- Utilize US Legal Forms, the most extensive collection of legal forms, to save time and avoid errors.

- The service provides professionally crafted legal document templates that can be utilized for a variety of purposes.

- Create an account on US Legal Forms and begin simplifying your life.

Form popularity

FAQ

Filing a trust in Indiana involves several key steps. First, you must draft a trust document outlining the terms and beneficiaries. Next, execute the document properly, and then consider funding the trust by transferring assets into it. For guidance, you can refer to resources available through uslegalforms to ensure compliance with Indiana laws.

How Can I Get My Money Out of a Trust?Create a Revocable Trust. There are revocable and irrevocable living trusts.List Your Rights. Spell out your right to withdraw money in the trust documents.Name Yourself a Trustee. Put the name of the trust, with yourself as trustee, on the ownership documents.Transfer Your Assets.

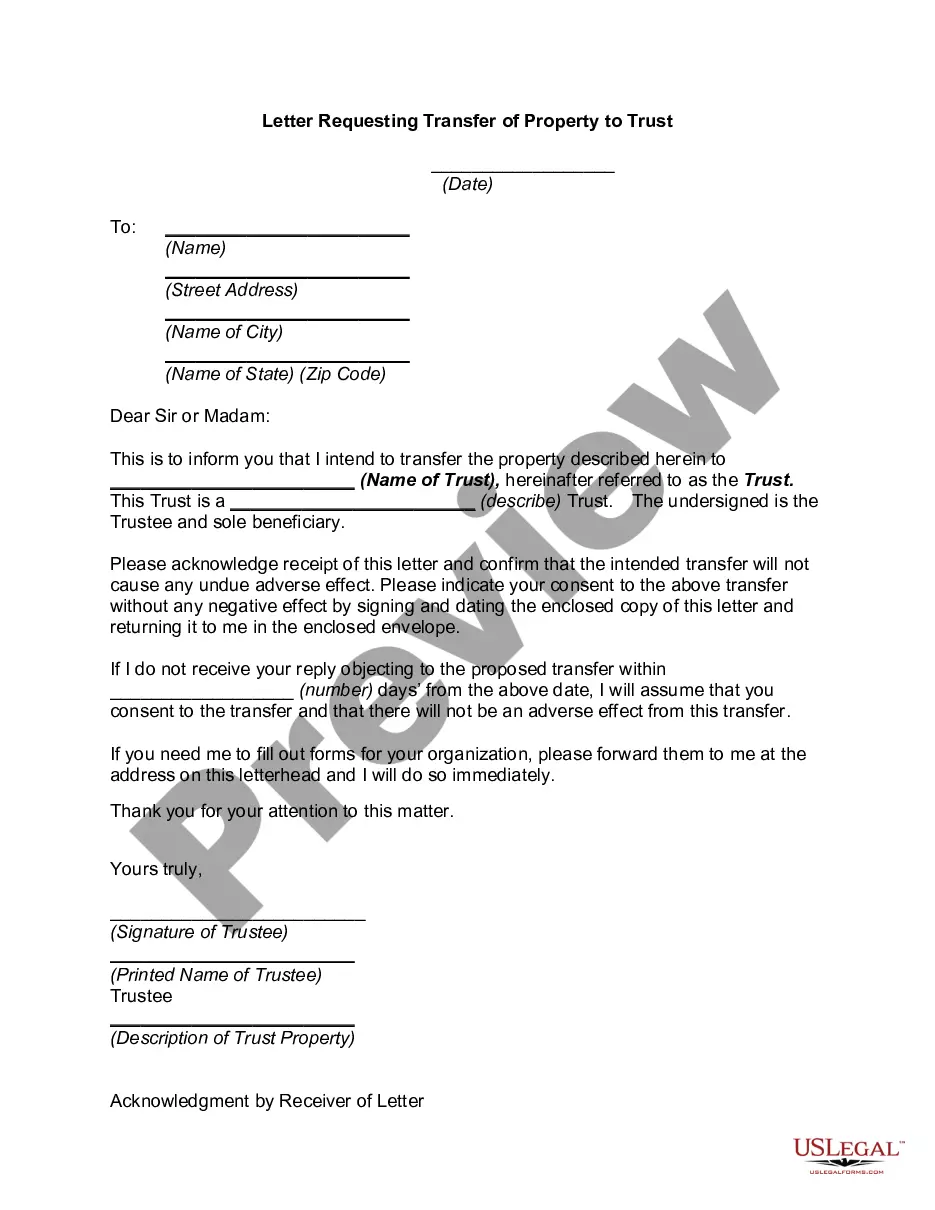

Reference the name of the irrevocable trust, and the trust account number if applicable. Write a salutation followed by a colon. Identify yourself as a beneficiary of the irrevocable trust in the body of the letter. State that you are requesting money from the trust, and the reason for the request.

The trust allows the trustee to gift from the trust to the current beneficiary's issue up to the annual gift exclusion (currently $15K).

The federal gift tax law provides that every person can give a present interest gift of up to $14,000 each year to any individual they want. This means that each parent can each give each of their children and grandchildren $14,000 (two parents permits a total gift per recipient of $28,000).

If you have created a revocable trust and have appointed someone else as trustee, you will have to request the cash withdrawal from the person you appointed as the trustee. However, the trustee has a fiduciary duty to administer the trust for your benefit while you are alive.

In Indiana, the statute of limitations to file a will contest is 90 days after the admission of a will to probate.

In the case of a good Trustee, the Trust should be fully distributed within twelve to eighteen months after the Trust administration begins. But that presumes there are no problems, such as a lawsuit or inheritance fights.

The grantor can set up the trust, so the money distributes directly to the beneficiaries free and clear of limitations. The trustee can transfer real estate to the beneficiary by having a new deed written up or selling the property and giving them the money, writing them a check or giving them cash.

When executing their trust, settlors generally name themselves as the sole trustee and beneficiary while they are living; this allows them to exercise full control over the trust and its assets during their lifetime, as well as to withdraw trust funds as they see fit.