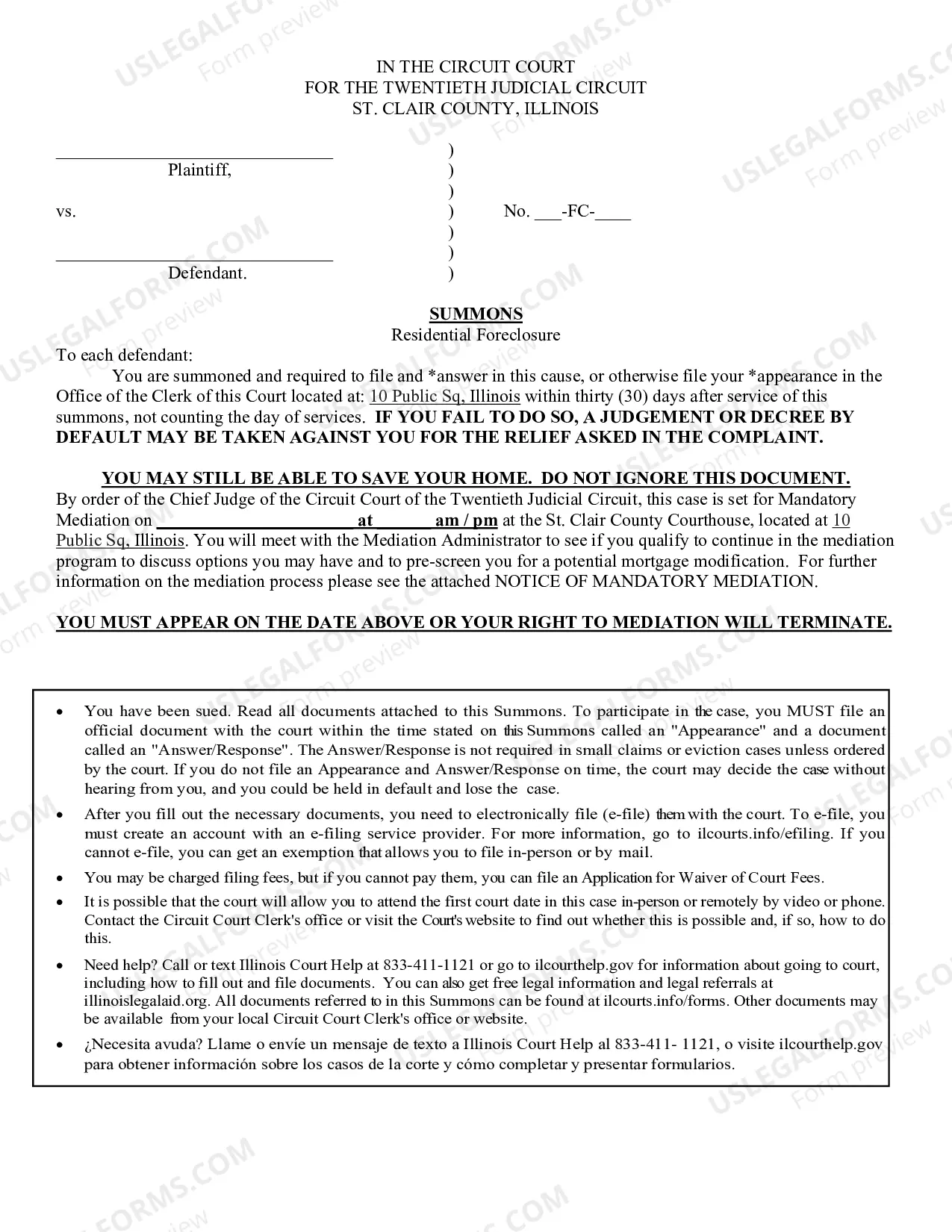

The Illinois Foreclosure Program Initial Questionnaire is a document used by the Illinois Department of Financial and Professional Regulation (ID FPR) to assess a homeowner’s eligibility for the Illinois Foreclosure Prevention Network (IFP). The questionnaire helps the ID FPR determine if the homeowner is a qualified participant in the program, which helps homeowners avoid foreclosure by providing counseling and other services. There are two types of Illinois Foreclosure Program Initial Questionnaire: one for homeowners who are facing foreclosure and another for homeowners who are already in foreclosure. The questionnaire for homeowners facing foreclosure includes questions about the homeowner's income, assets, debts, credit history, and other pertinent information. The questionnaire also requires the homeowner to provide proof of income, such as pay stubs or bank statements. The questionnaire for homeowners already in foreclosure requires the homeowner to provide information about the foreclosure process, including the date of the sale, the amount of the sale, and the current status of the foreclosure. The homeowner must also provide information about any attempts to stop the foreclosure, such as a loan modification or payment plan. The information collected through the Illinois Foreclosure Program Initial Questionnaire is used to determine if a homeowner is eligible for the IFP program and the services it provides.

Illinois Foreclsoure Program Initial Questionnaire

Description

How to fill out Illinois Foreclsoure Program Initial Questionnaire?

Filling out official documents can be quite a hassle if you lack pre-prepared fillable templates. With the US Legal Forms online repository of formal documents, you can trust the forms you receive, as they all align with federal and state laws and have been reviewed by our specialists.

So if you need to complete the Illinois Foreclosure Program Initial Questionnaire, our service is the ideal destination to access it.

Here’s a quick guide for you: Document compliance verification. You should thoroughly review the content of the form you wish to use and determine if it meets your requirements and complies with your state's regulations. Previewing your document and examining its overall description will assist you in doing just that.

- Retrieving your Illinois Foreclosure Program Initial Questionnaire from our collection is as straightforward as 1-2-3.

- Previously registered users with an active subscription simply need to Log In and click the Download button when they find the appropriate template.

- If necessary, users can also select the same form from the My documents section of their account.

- However, if you are a new user, signing up for an active subscription will only take a few minutes.

Form popularity

FAQ

How Can I Stop Foreclosure in Illinois? Your First Move: Find the Right Foreclosure Attorney. Negotiate with the Lender to Resume Payments. Request a Loan Modification. Seek Special Relief: CARES Act And COVID-19. Address Payments Missed By Mistake. Take the Case to Chicago Courts. Turn the House over to the Lender.

Subject to a few limited exceptions, you have 7 months from the date you are served to pay off your loan in full, either by refinancing the loan or by selling the house or by other means. This is called your right to redeem, and the 7-month period is called the redemption period. Sometimes you can have longer.

In Illinois, there is a redemption period during which you have the legal right to pay off the total debt plus certain costs and interest and reclaim your property, even after a judgment of foreclosure. The property cannot be sold during the redemption period.

In Illinois, it can take approximately 12-15 months for a foreclosure to be completed. Call your lender or a HUD-certified counseling agency as soon as you can.

In general, a lender won't begin foreclosure until you've missed four consecutive mortgage payments. Timing can vary from lender to lender as well as on the state of the housing market at the time. Lenders generally prefer to avoid foreclosure because it is costly and time-consuming.

In Illinois, your mortgage loan will automatically default after 90 days without payment. At this point, your lender will send a Notice of Default (NOD), which serves the purpose of informing you of their intent to foreclose on your property due to lack of payment.

How Long Do You Have to Move Out After Foreclosure in Illinois? You (the foreclosed homeowner) can stay in the home for 30 days after the court confirms the sale. (735 Ill. Comp.

Subject to a few limited exceptions, you have 7 months from the date you are served to pay off your loan in full, either by refinancing the loan or by selling the house or by other means. This is called your right to redeem, and the 7-month period is called the redemption period.