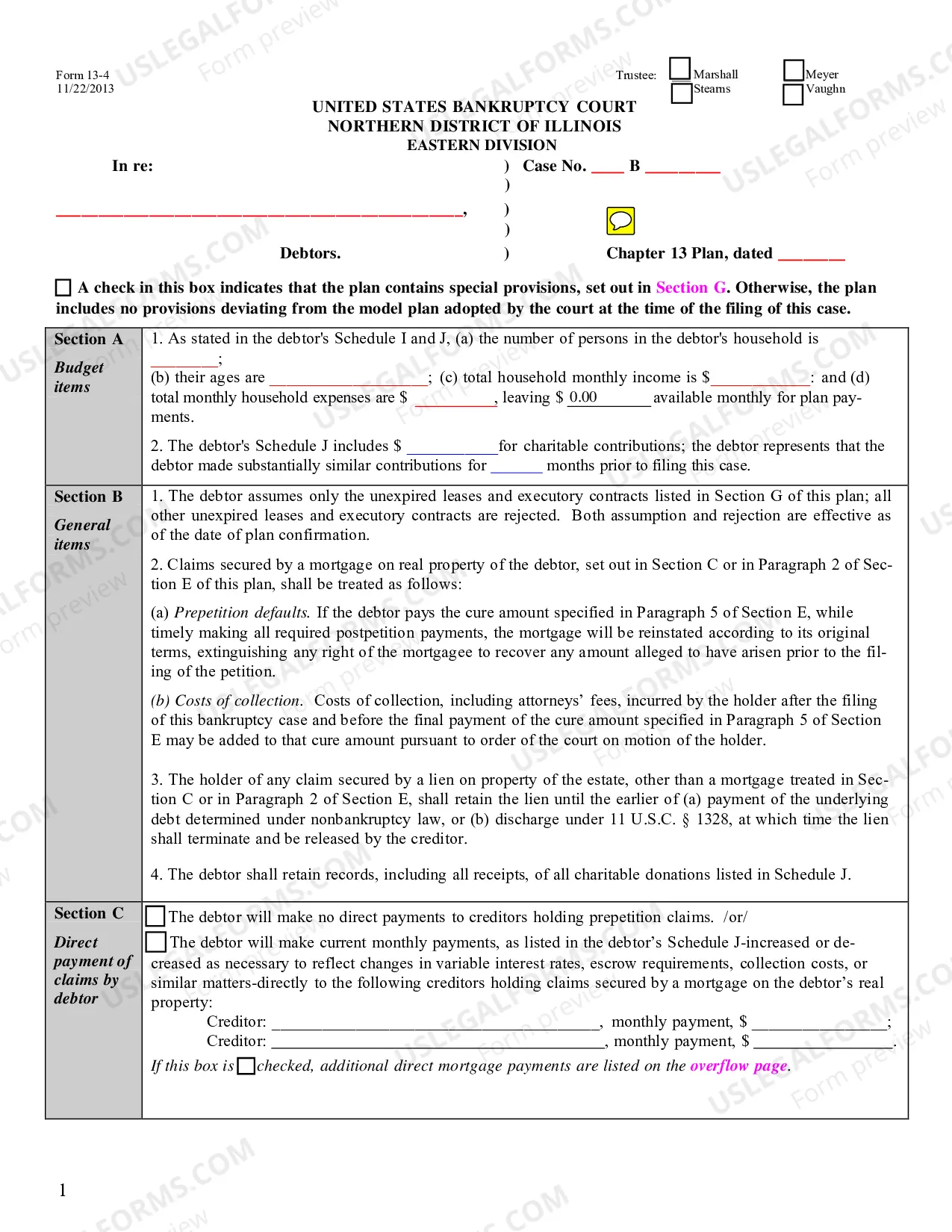

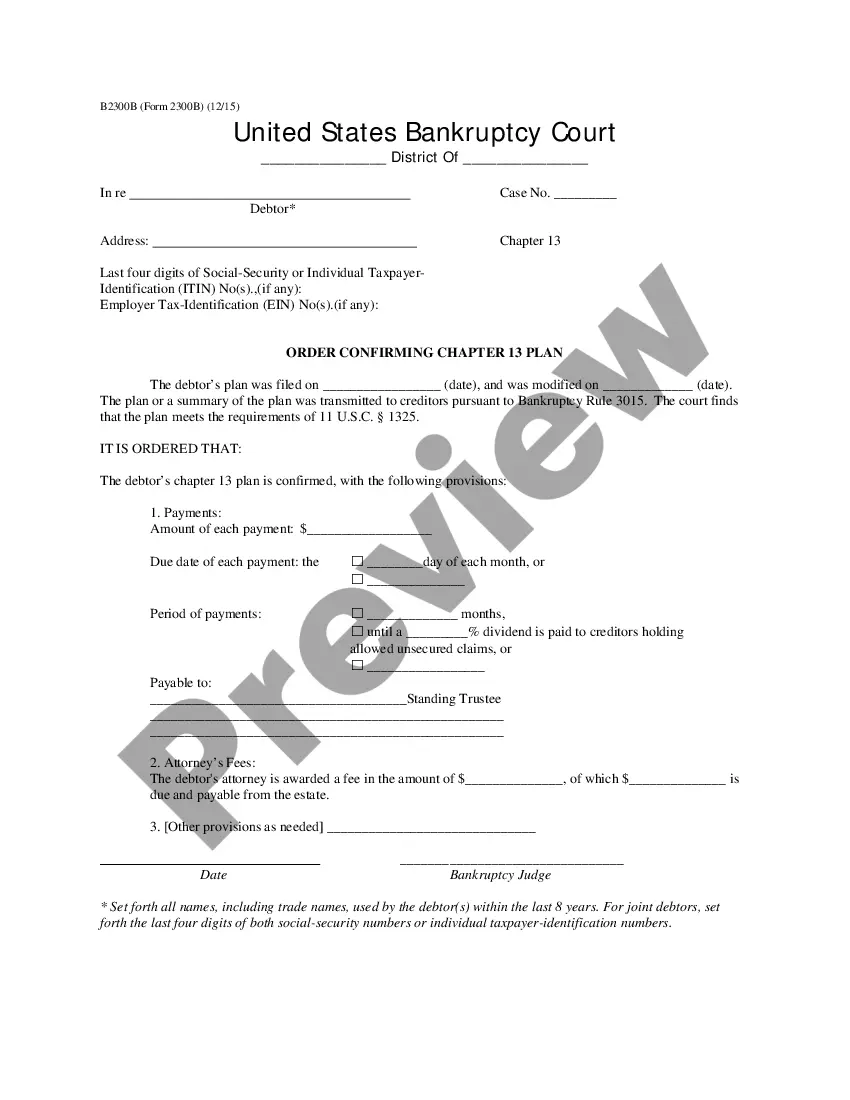

The Illinois Chapter 13 Model Plan (non-calculating) is a type of bankruptcy filing available for individuals in Illinois. It allows for debtors to pay their creditors through a court-approved repayment plan. The repayment plan is based on the debtor’s income, expenses, and other factors. The plan is typically over a 3-5 year period. Under the Illinois Chapter 13 Model Plan (non-calculating), debtors must make regular payments to a court-appointed trustee, who then distributes the money to creditors according to the approved repayment plan. The payments are typically made on a biweekly or monthly basis. The Illinois Chapter 13 Model Plan (non-calculating) also allows for debtors to discharge certain types of debt. This includes credit card debt, medical bills, personal loans, and other unsecured debt. It also allows for debtors to keep certain assets, such as a home or vehicle, that would otherwise be liquidated in a Chapter 7 bankruptcy. There are two types of Illinois Chapter 13 Model Plan (non-calculating): the Standard Plan and the Modified Plan. The Standard Plan is the more common of the two, and it requires debtors to pay a percentage of their unsecured debt. The Modified Plan is better suited for debtors with more challenging financial circumstances, and it requires debtors to pay all of their unsecured debt.

Illinois Chapter 13 Model Plan (non-calculating)

Description

")

")

")

")

")

")

How to fill out Illinois Chapter 13 Model Plan (non-calculating)?

Managing legal documentation necessitates focus, accuracy, and utilizing well-prepared templates.

US Legal Forms has been assisting individuals across the country with this for 25 years, so when you select your Illinois Chapter 13 Model Plan (non-calculating) template from our platform, you can be assured it adheres to federal and state regulations.

All documents are crafted for multiple uses, similar to the Illinois Chapter 13 Model Plan (non-calculating) displayed here. If you require them again in the future, you can complete them without any additional payment - simply access the My documents tab in your profile and finalize your document whenever necessary. Experience US Legal Forms and efficiently prepare your business and personal documentation in full legal compliance!

- Ensure to carefully review the form's content and its alignment with general and legal criteria by previewing it or examining its description.

- Look for an alternative official template if the first one does not fit your situation or state laws (the option for this is located on the top page corner).

- Log in to your account and save the Illinois Chapter 13 Model Plan (non-calculating) in your desired format. If it’s your initial experience with our site, click Buy now to proceed.

- Create an account, select your subscription plan, and make your payment using your credit card or PayPal.

- Choose the format you wish to save your document in and click Download. Print the blank form or add it to a professional PDF editor for a paperless preparation.

Form popularity

FAQ

The Chapter 13 Hardship Discharge After confirmation of a plan, circumstances may arise that prevent the debtor from completing the plan. In such situations, the debtor may ask the court to grant a "hardship discharge." 11 U.S.C. § 1328(b).

If your Chapter 13 plan payment is too high, you can sometimes get it lowered if you encounter a reduction in household income. If your income reduces, you are many times also allowed to reduce your plan payment. This is accomplished usually by filing a Motion to Modify your Chapter 13 plan.

Many low-income filers have little or no nonexempt property, and no disposable income left after paying their bills and expenses. If you are in this situation, your plan can propose to pay off only your required debts, making no payments on your unsecured debt.

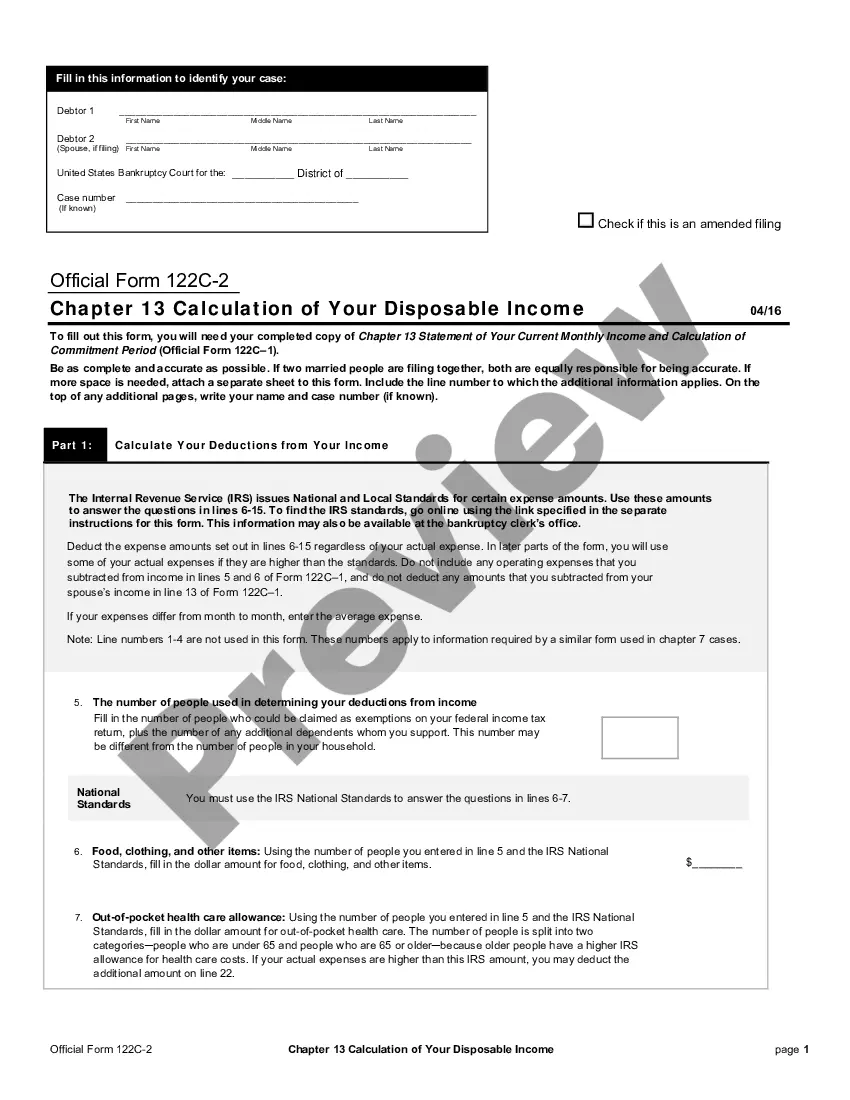

The disposable income calculation starts with your gross income. You must also be a wage earner in order to file a Chapter 13. Then, certain expenses are deducted based on an IRS deduction. The deduction is based upon a national average, taking into consideration the metropolitan area you live.

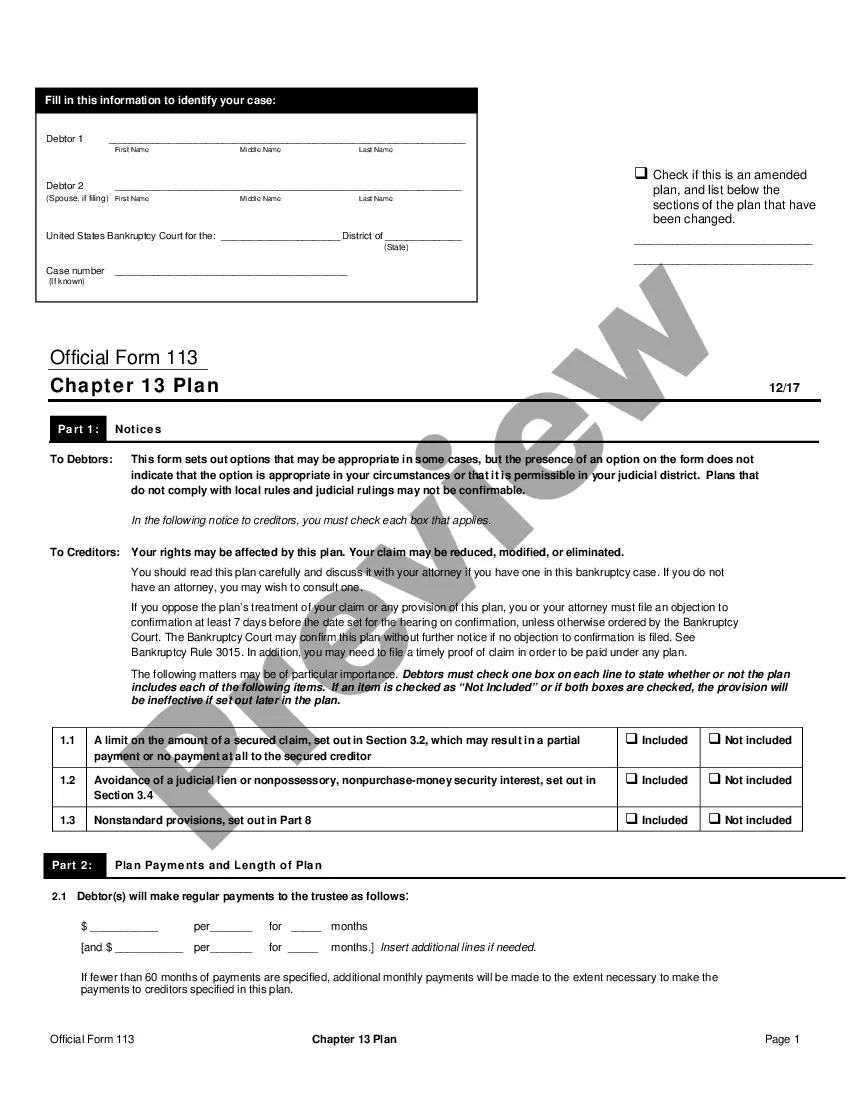

In Chapter 13 bankruptcy, you must devote all of your disposable income to your Chapter 13 repayment plan. Through the plan, which lasts either three or five years, you pay 100% of certain debts and a portion of other types of debts.

You Have Too Much Debt. You must have no more than $419,275 of unsecured debt or $1,257,850 of secured debt to be eligible for a Chapter 13 bankruptcy. Secured debts refer to debts based on collateral, in which the creditor has the right to take property back if you do not make payments.

The chapter 13 disposable income test is the court's way of ensuring that all your disposable income is going towards repaying your debts during your repayment period. Prior to approving any chapter 13 repayment plan, you must show that what you are paying is your best effort.

To calculate the total average monthly payment, add all amounts that are contractually due to each secured creditor in the 60 months after you file for bankruptcy. Then divide by 60.