Illinois Flood Zone Statement and Authorization

About this form

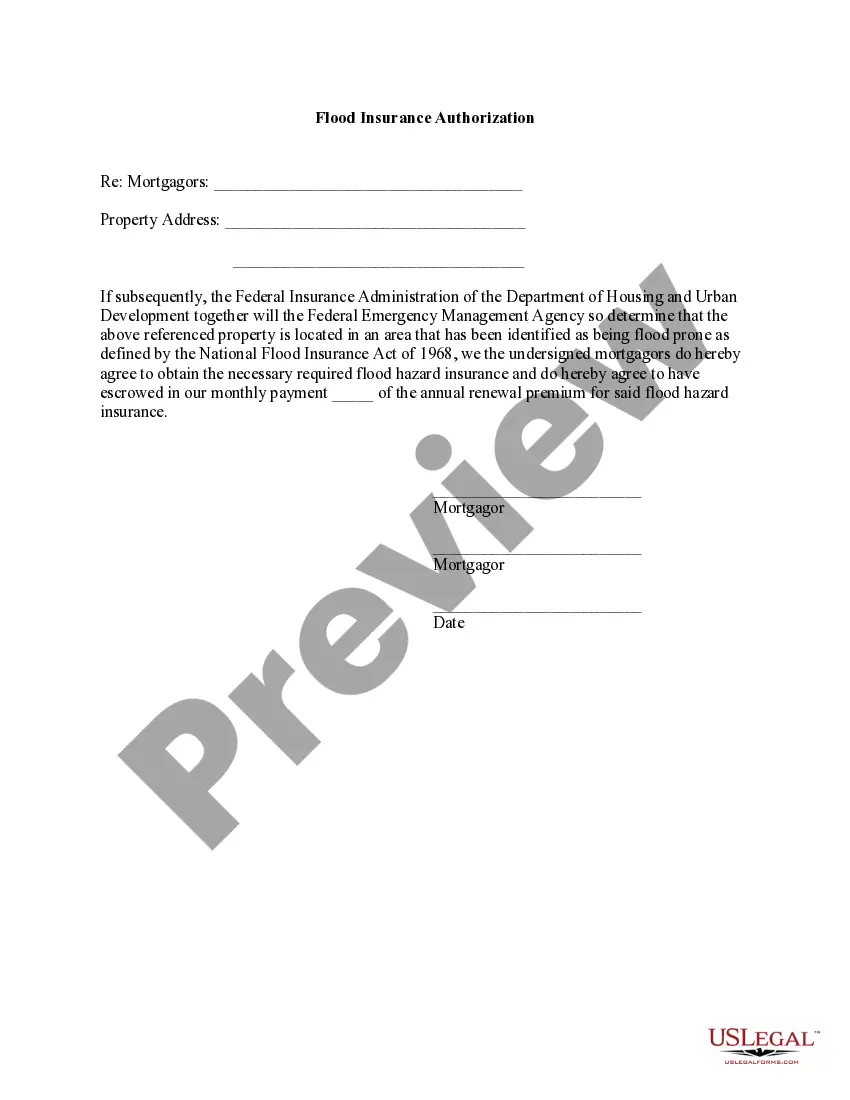

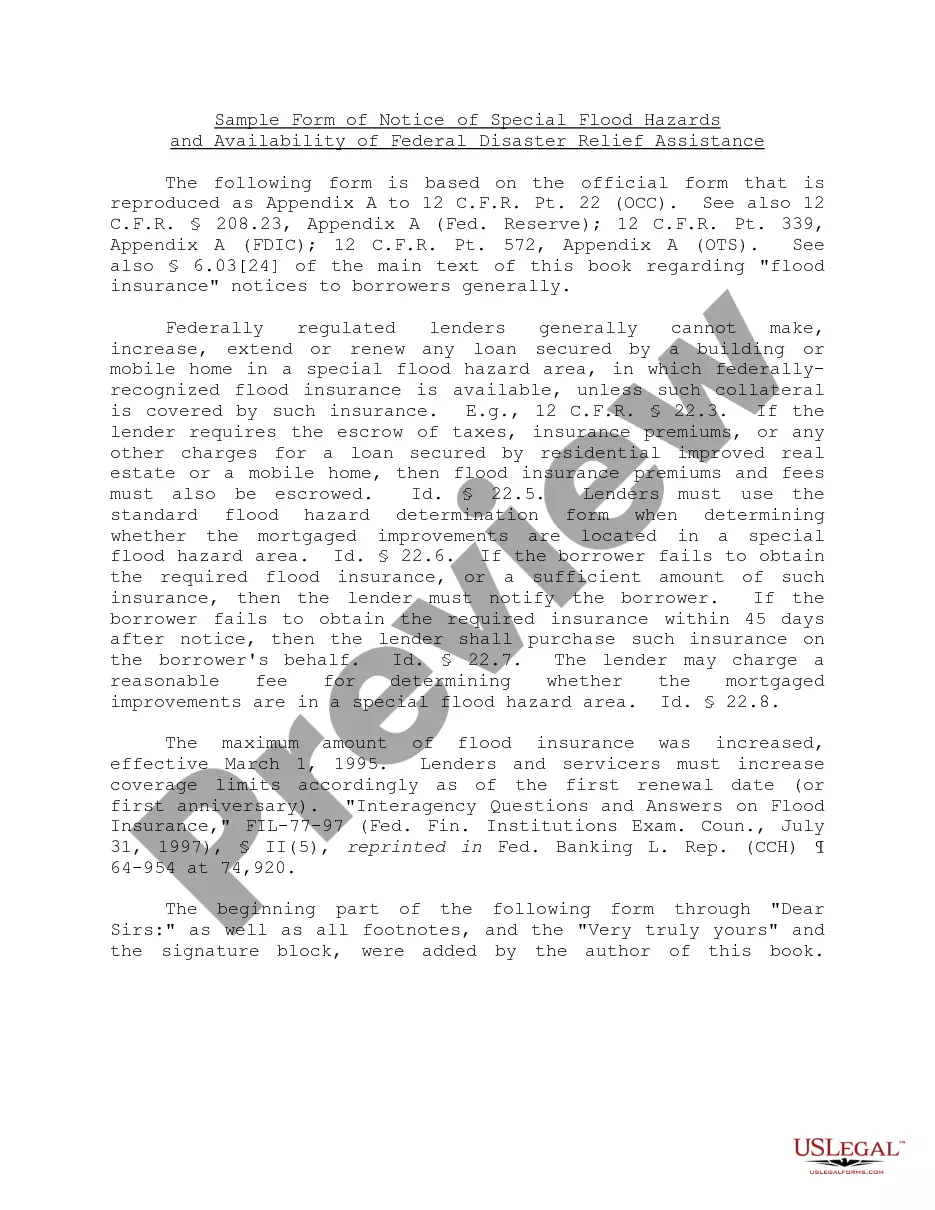

The Flood Zone Statement and Authorization is a legal document used in real estate transactions. It requires sellers to disclose the flood zone status of a property and requires buyers to acknowledge this status. This form plays a critical role in ensuring that all parties are aware of potential flood risks and insurance obligations. Unlike other property disclosure forms, it specifically addresses flood zones as defined by the National Flood Insurance Act of 1968.

Key components of this form

- Property address: Specify the location of the real estate being sold.

- Seller's statement: Sellers indicate whether the property is in a flood-prone area.

- Buyer's acknowledgment: Buyers confirm they are aware of the flood zone status and their insurance obligations.

- Insurance agreement: Buyers agree to secure flood hazard insurance if the property is determined to be flood-prone post-sale.

- Signatures: Required for both sellers and buyers to validate the document.

When this form is needed

This form should be used during the sale of residential or commercial properties, particularly in areas known for flooding. It's necessary when a seller must clarify flood zone risks and a buyer needs to understand their insurance obligations. It is crucial in safeguarding both parties by transparently communicating property risks.

Who should use this form

- Property Sellers: Individuals or entities selling real estate in flood-prone regions.

- Property Buyers: Individuals or entities purchasing real estate who need to confirm flood status.

- Real Estate Agents: Professionals facilitating property transactions to ensure compliance and protection for clients.

Completing this form step by step

- Identify the property: Fill in the complete property address in the designated space.

- Sellers' disclosure: Check the appropriate box to declare the flood zone status.

- Attach documentation: Include any relevant surveys or certifications regarding flood status.

- Buyers' acknowledgment: Confirm awareness of flood risks and agree to insurance terms.

- Sign and date: Ensure both sellers and buyers sign and date the form for validation.

Notarization requirements for this form

This form does not typically require notarization unless specified by local law. Always check your jurisdictionâs regulations to confirm if additional notarization is necessary.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to check the correct flood zone status box.

- Not providing or attaching necessary flood certifications.

- Omitting signatures or dates, leaving the form invalid.

- Using outdated information regarding the flood status of the property.

- Not understanding local laws that may affect the use of this form.

Benefits of completing this form online

- Convenience: Easily download, complete, and store the form electronically.

- Editability: Edit fields as needed before finalizing and printing.

- Reliability: Access professionally drafted templates that adhere to legal standards.

Legal use & context

- The form mitigates risk by ensuring clear communication regarding flood zone status.

- It provides legal protection for sellers against future claims of non-disclosure.

- Buyers are legally bound to obtain flood insurance if the property is later identified as being in a flood zone.

Quick recap

- The Flood Zone Statement and Authorization is essential for property transactions involving potential flood risk.

- Both sellers and buyers have defined responsibilities regarding flood zone disclosure and insurance.

- Completing this form helps ensure compliance with legal requirements, protecting both parties in a transaction.

Glossary of terms

- Flood zone: An area identified by the federal government as being at risk for flooding.

- Flood insurance: Insurance coverage that protects property owners from losses due to flooding.

- National Flood Insurance Act of 1968: A federal law that established a program for flood insurance and floodplain management.

Looking for another form?

Form popularity

FAQ

Summary: Proximity to a flood zone lowers property values. By law, a property is considered in a flood zone if any part of the structure falls within a floodplain, an area that is adjacent to a stream or river that experiences periodic flooding.

Evidence of flood insurance Completed and executed NFIP Flood Insurance Application PLUS a copy of the Borrower's premium check or agent's paid receipt.

Areas in flood zone A have a 1 percent chance of flooding per year and a 25 percent chance of flooding at least once during a 30-year mortgage. Since there haven't been detailed hydraulic analysis in these areas, the base flood elevation and depths have not been determined.

Use the Comments area of Section D, on the back of the certificate, to provide datum, elevation, or other relevant information not specified on the front. Complete Section E if the building is located in Zone AO or Zone A (without BFE). Otherwise, complete Section C instead.

If you live in a high-risk area for flooding and are purchasing flood insurance through the National Flood Insurance Program (NFIP), you will almost certainly be required to provide an elevation certificate to complete your purchase.

Zone A. Zone A is the flood insurance rate zone that corresponds to the I-percent annual chance floodplains that are determined in the Flood Insurance Study by approximate methods of analysis.

The BFE is the elevation that floodwaters are estimated to have a 1% chance of reaching or exceeding in any given year. The higher your lowest floor is above the BFE, the lower the risk of flooding. Lower risk typically means lower flood insurance premiums.

If you live in a high-risk area for flooding and are purchasing flood insurance through the National Flood Insurance Program (NFIP), you will almost certainly be required to provide an elevation certificate to complete your purchase.

The best way to find flood insurance without a Flood Elevation Certificate is to consult a licensed flood insurance agent to see if they work with any companies that don't rely on a certificate to price out flood risk.