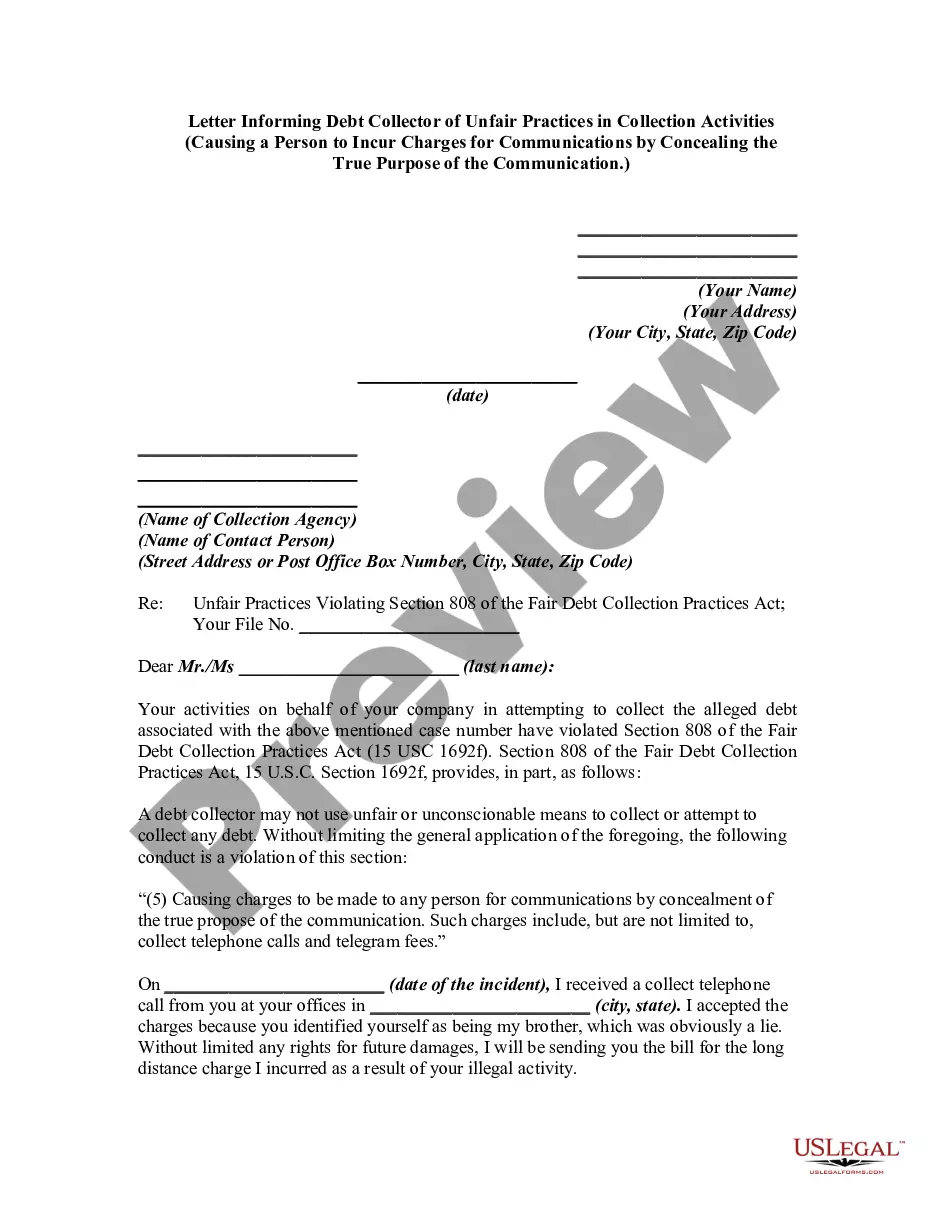

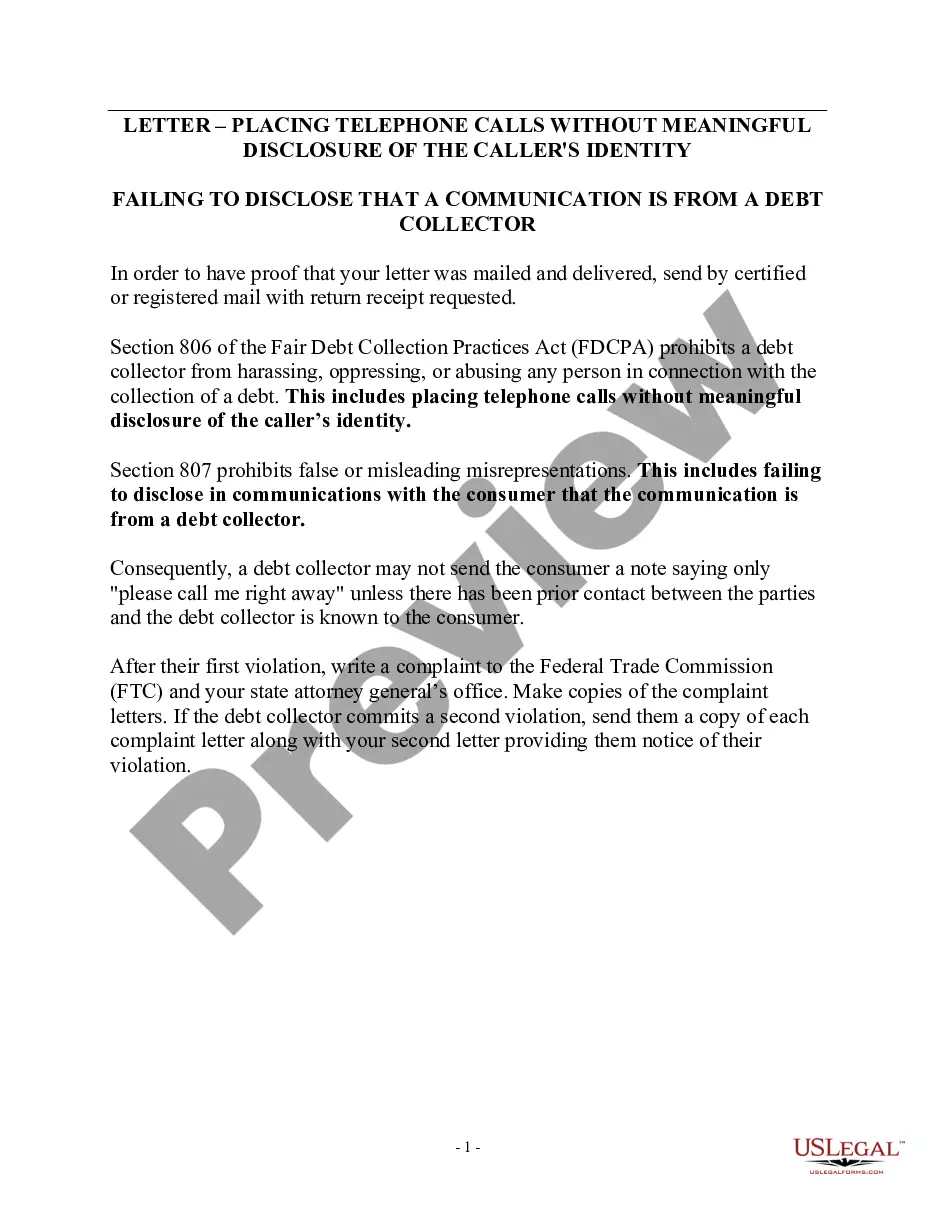

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

Idaho Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

Selecting the appropriate legal document template can be quite challenging. Clearly, there are numerous formats accessible online, but how will you find the legal form you require? Utilize the US Legal Forms website.

This service provides a vast array of templates, including the Idaho Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication, which you can utilize for both business and personal needs. All of the forms are reviewed by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and click the Download button to acquire the Idaho Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication. Use your account to browse the legal forms you have previously purchased. Go to the My documents section of your account to retrieve another copy of the document you need.

Complete, edit, print, and sign the acquired Idaho Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication. US Legal Forms is the largest collection of legal forms where you can view various document templates. Utilize the service to download professionally crafted paperwork that meets state requirements.

- If you are a new customer of US Legal Forms, here are basic instructions for you to follow.

- First, ensure you have chosen the correct form for your region/area. You can review the form using the Preview feature and examine the form description to confirm it is indeed the right one for you.

- If the form does not meet your expectations, utilize the Search field to find the suitable form.

- Once you are confident that the form is acceptable, click the Get now button to obtain the form.

- Choose the pricing plan you prefer and input the necessary information. Create your account and process the payment using your PayPal account or Visa or Mastercard.

- Select the file format and download the legal document template to your device.

Form popularity

FAQ

Yes. The federal Fair Debt Collection Practices Act specifically gives you the right to sue a debt collector for harassment. If a debt collector is found to have engaged in harassing behavior, you are entitled to up to $1,000 in damages, along with court costs and attorney fees.

The Fair Credit Reporting Act is a federal law that regulates the collection and reporting of credit information from consumers. The law governs how a consumer's credit information is collected and shared with others.

The Debt Collectors Act specifically provides that a debt collector MAY NEVER charge more than 10% plus Vat of the amount received from the debtor as a collection commission (the Act refers to a receipt fee).

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

The Fair Debt Collection Practices Act makes it illegal for debt collectors to harass or threaten you when trying to collect on a debt. In addition, on November 30, 2021, the CFPB's new Debt Collection Rule became effective.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

The Fair Debt Collection Practices Act (FDCPA) is the main federal law that governs debt collection practices. The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

The creditor pays the collector a percentage, typically between 25% to 50% of the amount collected. Debt collection agencies collect various delinquent debtscredit cards, medical, automobile loans, personal loans, business, student loans, and even unpaid utility and cell phone bills.