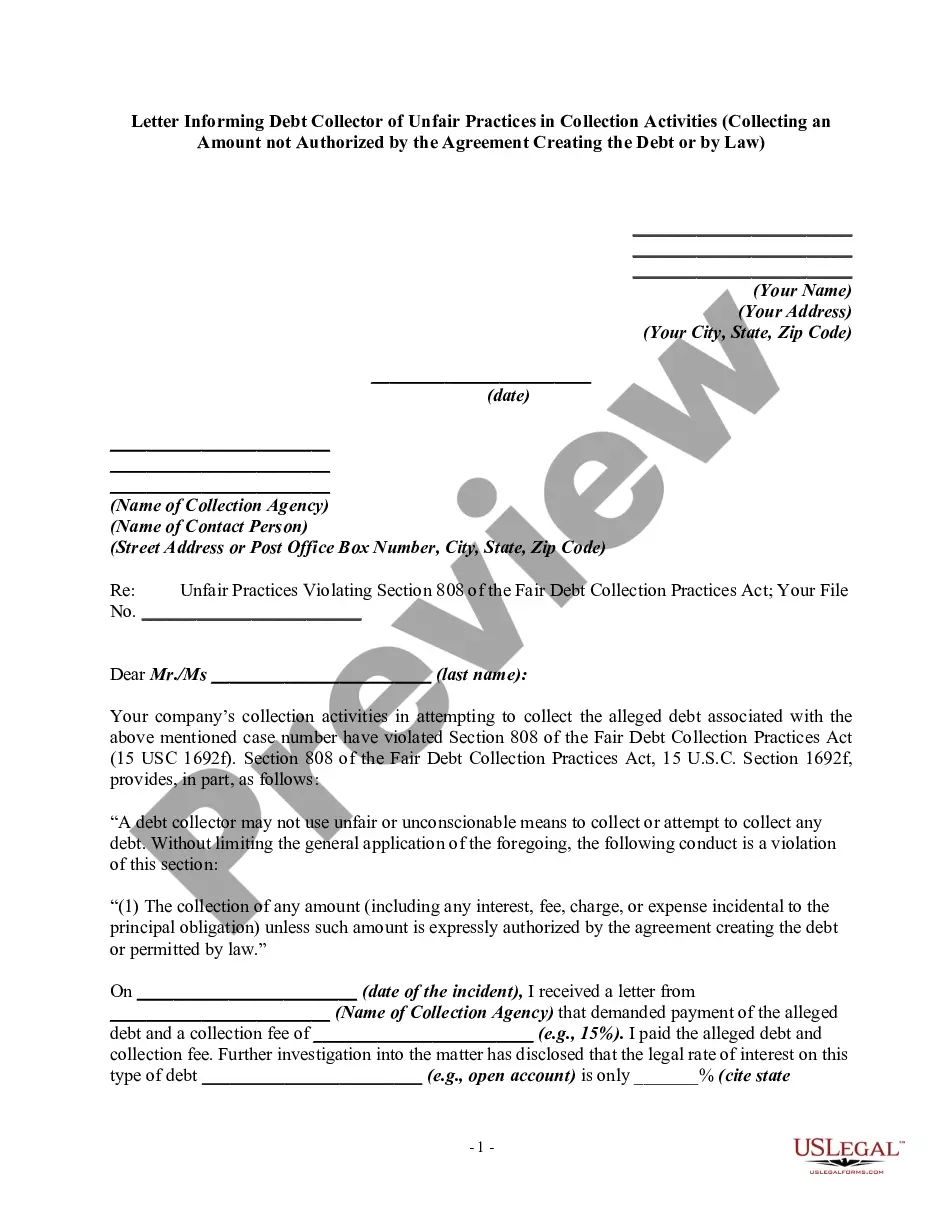

A debt collector may not use unfair or unconscionable means to collect a debt. This includes collecting an amount not authorized by the agreement creating the debt or by law.

Idaho Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law

Category:

State:

Multi-State

Control #:

US-DCPA-42

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Collecting An Amount Not Authorized By Agreement Or By Law?

Locating the appropriate legal document format can be challenging. Indeed, there are countless online templates accessible across the web, but how can you find the specific legal type you require? Utilize the US Legal Forms website.

The platform offers thousands of templates, including the Idaho Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law, which you can utilize for business and personal purposes. All documents are verified by professionals and comply with federal and state regulations.

If you are already registered, Log In to your account and then click the Download button to receive the Idaho Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law. Use your account to review the legal documents you have previously purchased. Navigate to the My documents tab of your account and obtain another copy of the document you require.

US Legal Forms is the premier repository of legal documents where you can find numerous file templates. Utilize the service to download professionally crafted documents that adhere to state requirements.

- First, ensure you have selected the correct form for your city/region. You can browse the form using the Preview button and review the form description to confirm it is suitable for you.

- If the form does not meet your requirements, employ the Search field to locate the appropriate form.

- When you are confident that the form is correct, click the Purchase now button to obtain the form.

- Choose the pricing plan you desire and enter the necessary information. Create your account and complete the transaction using your PayPal account or credit card.

- Select the document format and download the legal document to your device.

- Fill out, edit, print, and sign the acquired Idaho Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law.

Form popularity

FAQ

The 7-7 rule in collections refers to the communication limit debt collectors must follow. Specifically, they cannot contact you more than seven times in a seven-day period regarding the same debt. Understanding the Idaho Notice to Debt Collector - Collecting an Amount Not Authorized by Agreement or by Law can help you recognize when collectors have crossed these boundaries. Compliance with this rule is essential for protecting your rights.

If a debt collector fails to verify the debt but continues to go after you for payment, you have the right to sue that debt collector in federal or state court. You might be able to get $1,000 per lawsuit, plus actual damages, attorneys' fees, and court costs.

Plan and modify arrangements with them and the creditor. Organise a settlement offer with you that may make it easier to pay off the debt. Sell your debt to another company who will have the same arrangements and powers as the original creditor. Obtain an order from a court to repossess some of your property.

South Africa has different laws which specify prescription periods, for example, the Prescription Act says that contractual and delictual debts extinguish after three years from the date when it became payable (due).

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Debt collectors are legally required to send one within five days of first contact. You have within 30 days from receiving a debt validation letter to send a debt verification letter. Here's the important part: You have just 30 days to respond to a debt validation letter with your debt verification letter.

Debt collectors have no special legal powers. You may feel under pressure to pay more than you can afford, but don't feel threatened. Find out more about the difference between debt collectors and bailiffs. Debt collectors may work for your creditor, or they may work for a separate debt collection agency.

If a creditor takes too long to take action to recover a debt it becomes 'statute barred', meaning it can no longer be recovered through court action. In practical terms, this effectively means the debt is written off, even though technically it still exists.

If a debt collector fails to validate the debt in question and continues trying to collect, you have a right under the FDCPA to countersue for up to $1,000 for each violation, plus attorney fees and court costs, as mentioned previously.

Review the debt validation letter The debt validation letter includes: The amount owed. The name of the creditor seeking payment. A statement that the debt is assumed valid by the collector unless you dispute it within 30 days of the first contact.