Idaho Summary of Rights and Obligations under COBRA

Description

How to fill out Summary Of Rights And Obligations Under COBRA?

Are you currently in a situation where you require documents for either business or personal purposes almost every day.

There are numerous legitimate document templates accessible online, but locating ones you can rely on is not straightforward.

US Legal Forms provides a vast array of form templates, including the Idaho Summary of Rights and Responsibilities under COBRA, designed to meet state and federal requirements.

If you find the correct form, click on Buy now.

Choose the payment plan you prefer, fill out the required information to create your account, and complete your order using your PayPal or credit card.

- If you are already familiar with the US Legal Forms site and possess an account, simply Log In.

- After that, you can download the Idaho Summary of Rights and Responsibilities under COBRA template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is suited to the correct area/county.

- Use the Review button to examine the form.

- Check the details to confirm you have selected the right form.

- If the form is not what you are looking for, utilize the Search field to discover the form that meets your needs.

Form popularity

FAQ

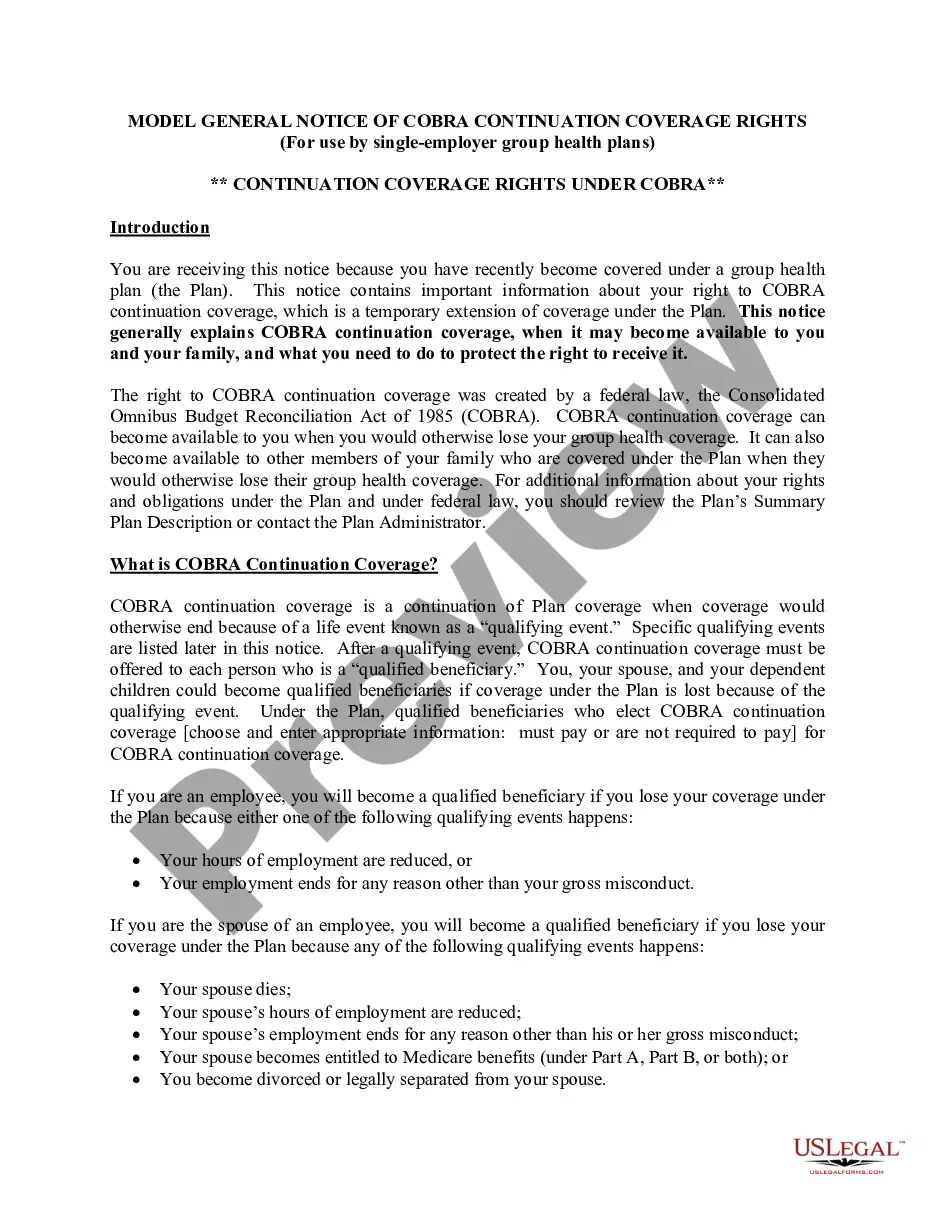

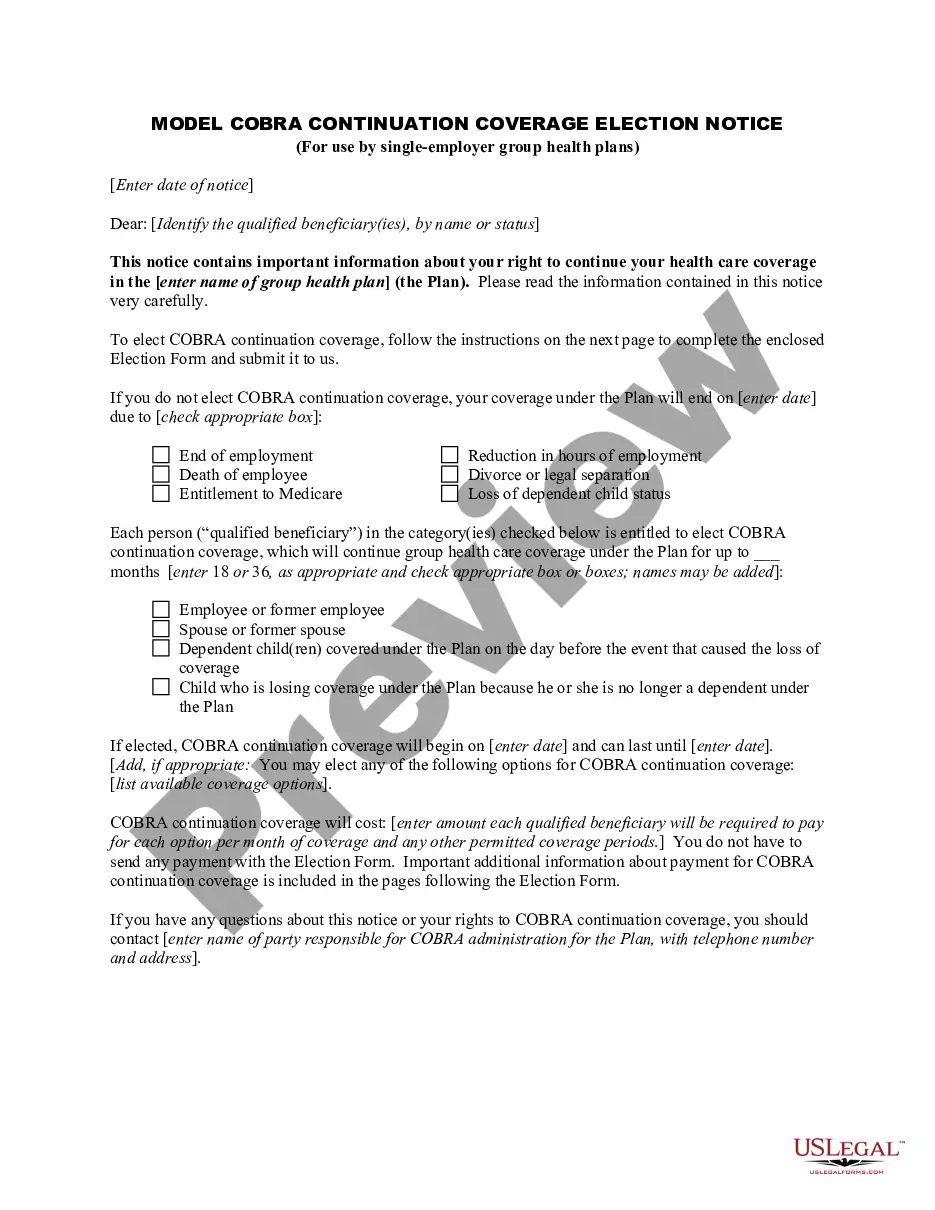

The following are qualifying events: the death of the covered employee; a covered employee's termination of employment or reduction of the hours of employment; the covered employee becoming entitled to Medicare; divorce or legal separation from the covered employee; or a dependent child ceasing to be a dependent under

The Consolidated Omnibus Budget Reconciliation Act (COBRA) Passed in 1985, COBRA is a federal law that allows employees of certain companies to continue their health insurance with the same benefits even after they stop working for their employer.

It is important to note that the federal COBRA law only applies to employers with 20 or more employees, and, while some states offer mini-COBRA continuation programs that apply to employers with fewer than 20 employees, Idaho currently does not offer any additional COBRA insurance benefits outside of those provided

The Consolidated Omnibus Budget Reconciliation Act (COBRA) gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances such as voluntary or involuntary job loss,

The Consolidated Omnibus Budget Reconciliation Act (COBRA) gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances such as voluntary or involuntary job loss,

COBRA is a federal law about health insurance. If you lose or leave your job, COBRA lets you keep your existing employer-based coverage for at least the next 18 months. Your existing healthcare plan will now cost you more. Under COBRA, you pay the whole premium including the share your former employer used to pay.

For disabled QBs who receive an 11-month COBRA extension (29 months in total), you can charge up to 150% of the group rate. Many states have regulations that are similar to federal COBRA. These state regulations are known as mini-COBRA.

The Consolidated Omnibus Budget Reconciliation Act (COBRA) is a federal law passed in 1986 that lets certain employees, their spouses, and their dependents keep group health plan (GHP) coverage for 18 to 36 months after they leave their job or lose coverage for certain other reasons, as long as they pay the full cost

Q3: Which employers are required to offer COBRA coverage? COBRA generally applies to all private-sector group health plans maintained by employers that had at least 20 employees on more than 50 percent of its typical business days in the previous calendar year.

Even if you enroll in COBRA on the last day that you are eligible, your coverage is retroactive to the date you lost your employer-sponsored health plan.