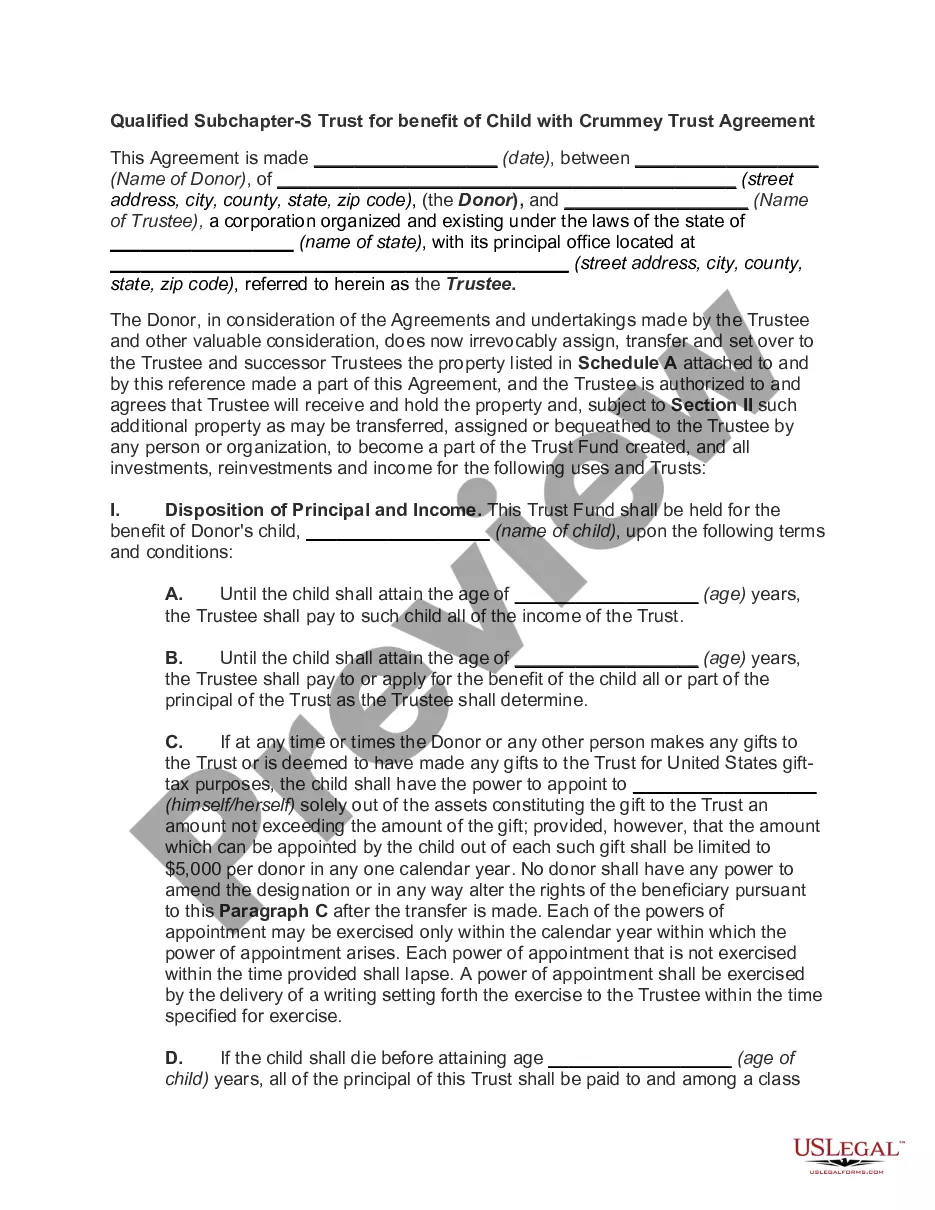

Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors

Description

How to fill out Crummey Trust Agreement For Benefit Of Child With Parents As Trustors?

US Legal Forms - one of the most prominent repositories of legal documents in the United States - provides a range of legal document templates that you can download or print.

While using the website, you can discover thousands of forms for business and personal purposes, categorized by types, states, or keywords. You can find the latest editions of forms such as the Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors in minutes.

If you have an account, Log In and download the Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors from the US Legal Forms collection. The Download button will appear on every form you view. You can access all previously downloaded forms from the My documents tab in your account.

Edit. Complete, modify and print and sign the downloaded Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors.

Every template you added to your account does not have an expiration date and belongs to you indefinitely. So, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Gain access to the Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs and requirements.

- If you are using US Legal Forms for the first time, here are some simple steps to get you started.

- Ensure you have selected the correct form for your city/state. Click the Review button to look over the form’s content. Check the form summary to confirm that you have selected the appropriate document.

- If the form doesn’t meet your requirements, use the Search field at the top of the screen to find one that does.

- When you are content with the form, confirm your choice by clicking on the Get now button. Then, choose your payment plan and provide your details to register for an account.

- Complete the transaction. Use your credit or debit card or PayPal account to finalize the payment.

- Select the format and download the form to your device.

Form popularity

FAQ

A potential disadvantage of an Iowa Crummey Trust Agreement for Benefit of Child with Parents as Trustors is the need for annual notifications. Parents must inform the child of their withdrawal rights each year, which can create an administrative burden. Additionally, if beneficiaries are unaware of their rights, they may miss the opportunity to withdraw funds during critical times. This lapse in understanding can lead to frustration for both parents and children.

Key TakeawaysTrust beneficiaries must pay taxes on income and other distributions that they receive from the trust. Trust beneficiaries don't have to pay taxes on returned principal from the trust's assets. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

Crummey Trust, Definition This type of trust is typically used by parents who want to make financial gifts to minor or adult children, though anyone can establish one on behalf of a beneficiary.

Crummey powers give the beneficiary a limited time (often 30, 45 or 60 days) to withdraw contributions to a trust at will, converting the future interest gift to a present interest gift. This withdrawal right is generally limited to an amount equal to the current annual gift tax exclusion.

Crummey powers give the beneficiary a limited time (often 30, 45 or 60 days) to withdraw contributions to a trust at will, converting the future interest gift to a present interest gift. This withdrawal right is generally limited to an amount equal to the current annual gift tax exclusion.

A Crummey Trust allows you to take advantage of the gift tax exclusions and simultaneously minimize your estate taxes. You do not have to provide an opportunity for the beneficiary to withdraw the entire balance of the trust until a certain age. A Crummey trust can have multiple beneficiaries.

Key Takeaways. Crummey power allows a person to receive a gift that is not eligible for a gift-tax exclusion and then effectively transform the status of that gift into one that is eligible for a gift-tax exclusion.

Crummey power is a technique that enables a person to receive a gift that is not eligible for a gift-tax exclusion and change it into a gift that is, in fact, eligible. Individuals often apply Crummey power to contributions in an irrevocable trust.

A Crummey trust is part of an estate planning technique that can be employed to take advantage of the gift tax exclusion when transferring money or assets to another person while retaining the option to place limitations on when the recipient can access the money.

Crummey trusts are typically used by parents to provide their children with lifetime gifts while sheltering their money from gift taxes as long as the gift's value is equal to or less than the permitted annual exclusion amount.