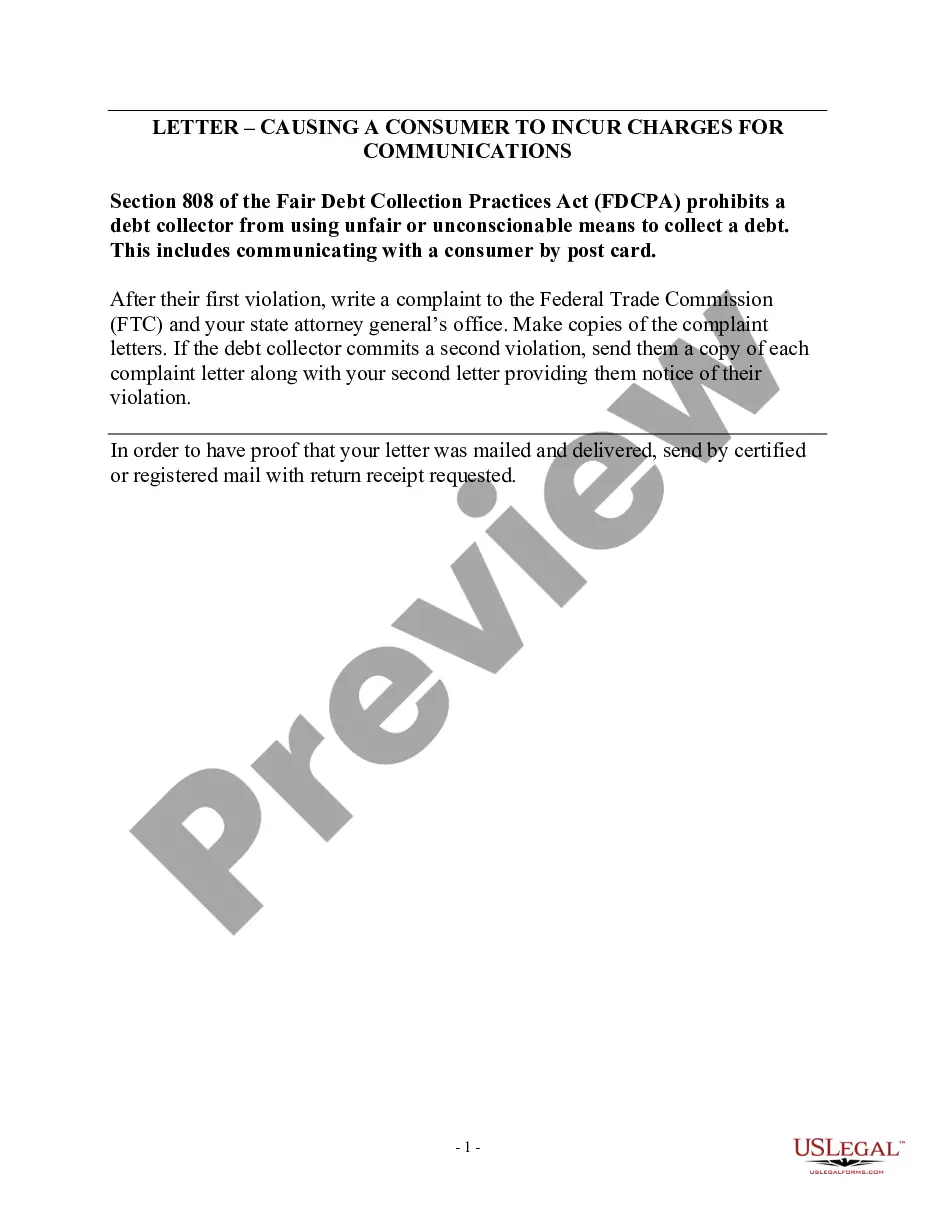

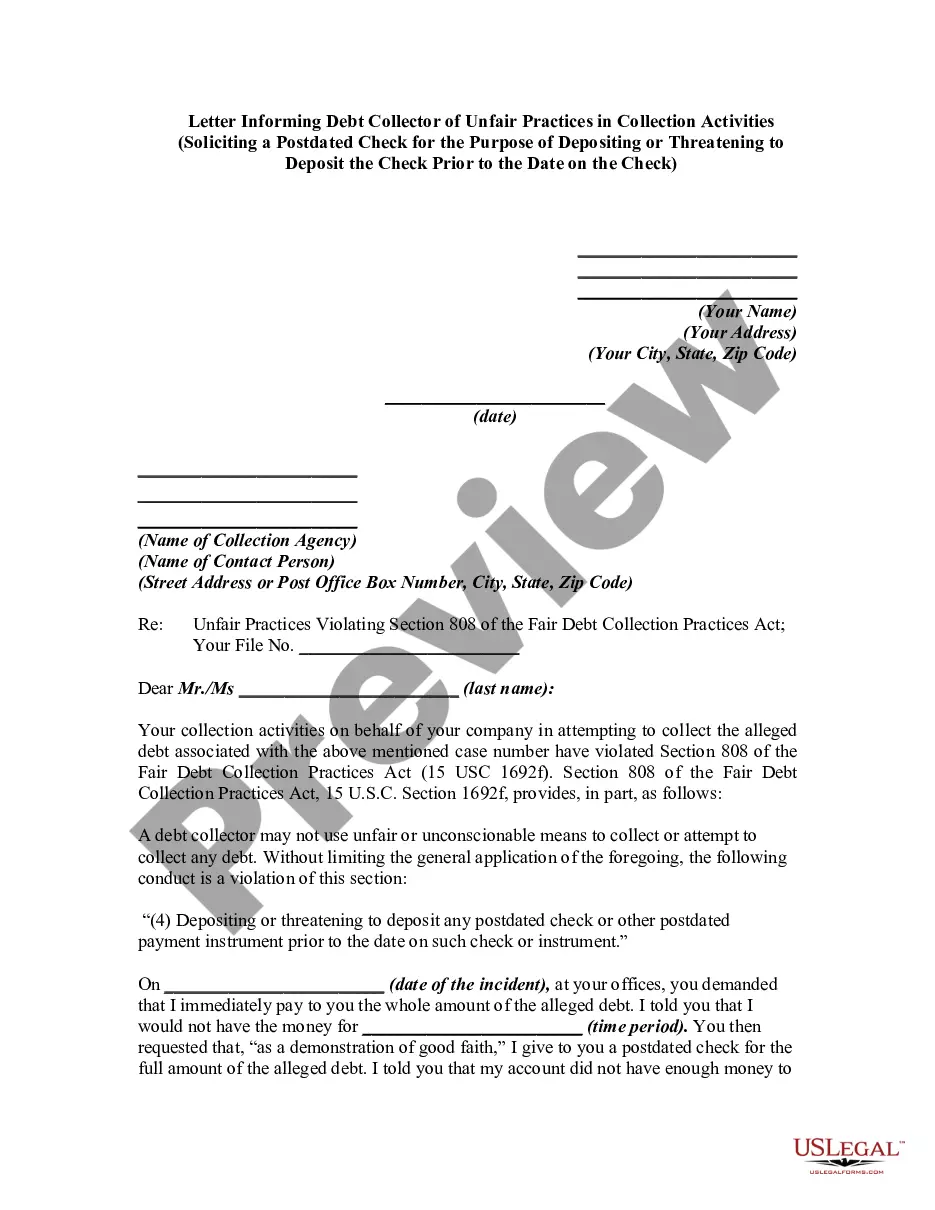

A debt collector may not use unfair or unconscionable means to collect a debt. This includes depositing a postdated check prior to the date on the check.

Delaware Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check

Category:

State:

Multi-State

Control #:

US-DCPA-43

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice To Debt Collector - Depositing A Postdated Check Prior To The Date On The Check?

Selecting the optimal official document format can be quite a challenge. It goes without saying that there are countless templates accessible online, but how do you acquire the official form you require? Utilize the US Legal Forms website.

The platform offers thousands of templates, such as the Delaware Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check, which you can apply for business and personal purposes. All forms are reviewed by experts and comply with federal and state regulations.

If you are already registered, Log In to your account and then click the Acquire button to obtain the Delaware Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check. Use your account to browse through the official forms you may have bought earlier. Go to the My documents section of your account and download another copy of the document you need.

US Legal Forms is the largest collection of official forms, where you can discover various document templates. Take advantage of this service to download professionally crafted documents that adhere to state requirements.

- First, ensure you have selected the appropriate form for your city/state. You can preview the form using the Preview button and review the form description to confirm it is suitable for your needs.

- If the form doesn’t meet your requirements, use the Search field to find the correct form.

- Once you are certain the form is suitable, click on the Get now button to obtain the form.

- Choose the pricing plan you desire and input the required information. Create your account and pay for your order using your PayPal account or credit card.

- Select the file format and download the official document format to your device.

- Complete, modify, print, and sign the received Delaware Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check.

Form popularity

FAQ

The primary rules for post-dated checks include not cashing or depositing them before their written date and clearly indicating this date on the check. Keep in mind that banks may process post-dated checks sooner than anticipated. If you're addressing a Delaware Notice to Debt Collector - Depositing a Postdated Check Prior to the Date on the Check, understanding the rules helps in meeting regulations. Always check your bank’s policies for specifics on handling these checks.

The Fair Debt Collection Practices Act (FDCPA) The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

Debts that may not be covered are those that are not incurred voluntarily, such as income taxes, parking and speeding tickets, and domestic support obligations like child support and alimony, or spousal support.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

The FDCPA broadly prohibits a debt collector from using 'any false, deceptive, or misleading representation or means in connection with the collection of any debt. ' 15 U.S.C. § 1692e. The statute enumerates several examples of such practices, 15 U.S.C.

Postdated checks can usually be cashed or deposited at any time unless the person who wrote the check specifically told their bank not to honor the check until a certain date. Rather than writing a postdated check, it may be better to use online payment services or coordinate with your biller to move back the due date.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.