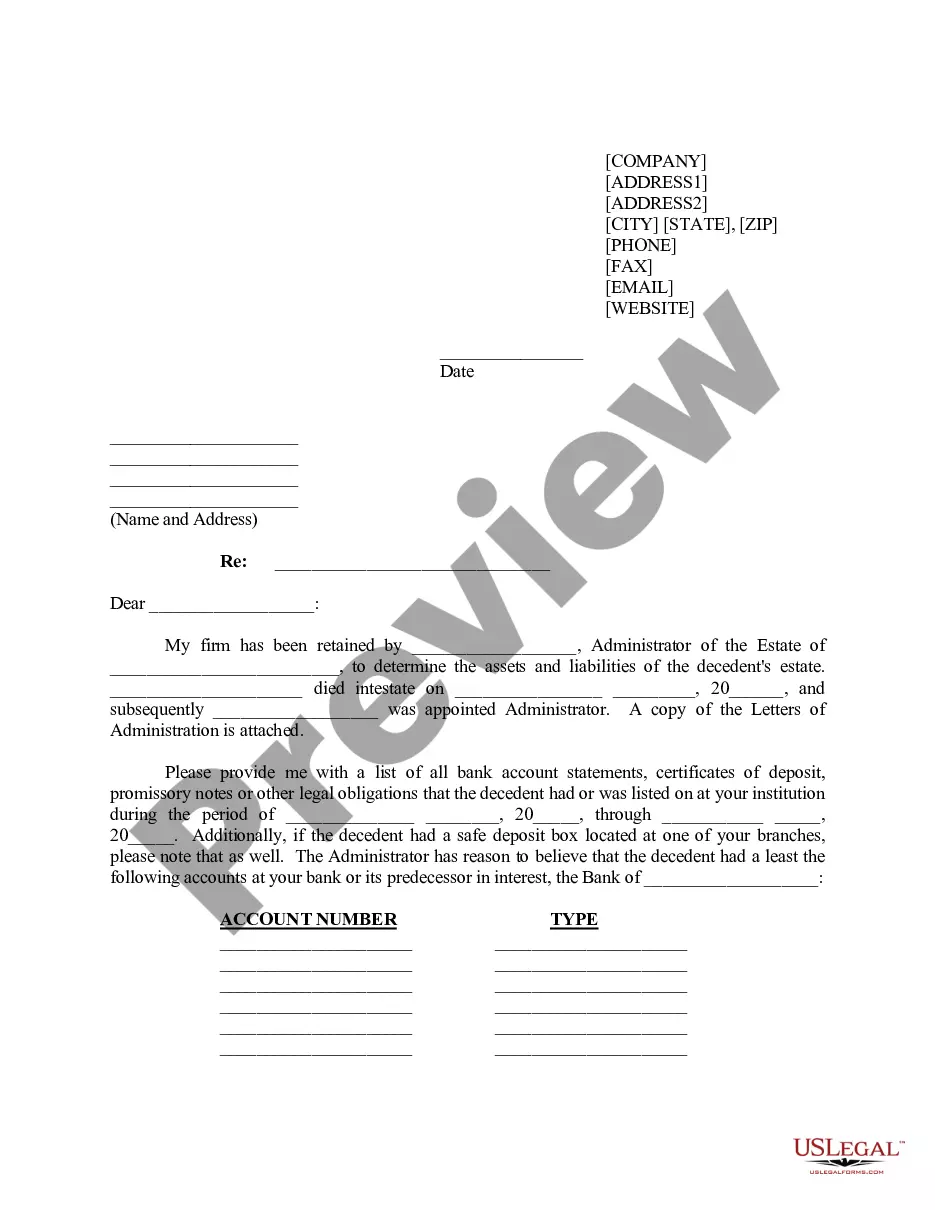

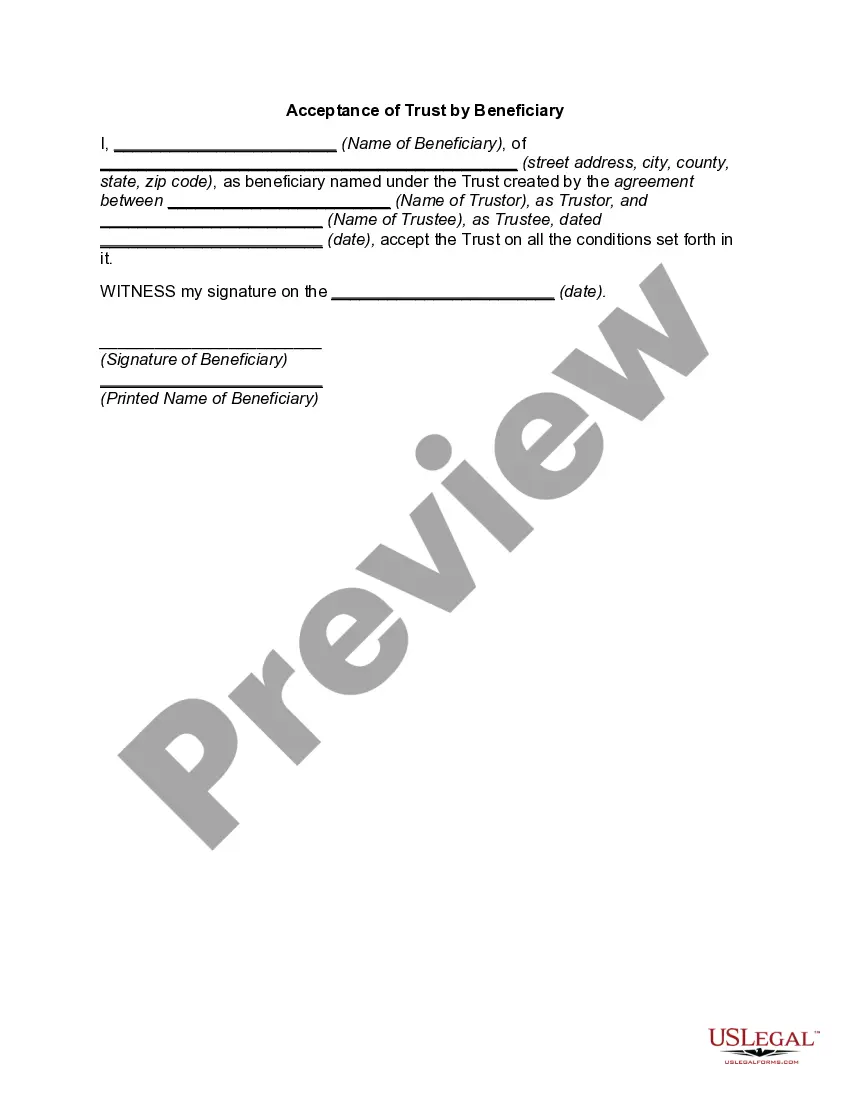

This form anticipates that a decedent left a will directing that all assets in a certain investment account be transferred to a trust. This form is a sample request to the investment firm from the trustee/executor for the assets.

District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent

Instant download

Description

How to fill out Letter Of Instruction To Investment Firm Regarding Account Of Decedent From Executor / Trustee For Transfer Of Assets In Account To Trustee Of Trust For The Benefit Of Decedent?

You can spend numerous hours online searching for the legal document format that meets the state and federal criteria you need.

US Legal Forms offers a vast array of legal documents that have been reviewed by experts.

It is easy to download or print the District of Columbia Letter of Instruction to Investment Firm Concerning Account of Decedent from Executor / Trustee for Asset Transfer in Account to Trustee of Trust for the Benefit of Decedent from my assistance.

If available, utilize the Review button to examine the document format as well.

- If you already possess a US Legal Forms account, you can Log In and then click the Obtain button.

- After that, you can fill out, amend, print, or sign the District of Columbia Letter of Instruction to Investment Firm Concerning Account of Decedent from Executor / Trustee for Asset Transfer in Account to Trustee of Trust for the Benefit of Decedent.

- Every legal document format you purchase is yours permanently.

- To obtain another copy of any purchased form, go to the My documents tab and click the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, make sure to select the correct document format for the area/city of your choice.

- Check the form description to confirm you have selected the appropriate form.

Form popularity

FAQ

Being a grantor means you are the individual who creates a trust and establishes its terms, which dictate how the assets will be managed and distributed. As the grantor, you have the authority and responsibility to define the structure and purpose of the trust. In the context of the District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, your role as a grantor is foundational to the trust's operation.

Yes, a trust can transfer assets to another trust under certain conditions. This could be beneficial for reorganizing or reclassifying assets based on changing needs or circumstances. When addressing this in a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, proper documentation and adherence to legal standards are necessary.

A trustee has several important obligations towards a beneficiary, including managing the trust assets prudently and acting in the beneficiary's best interests. They must communicate effectively about the trust's status and ensure timely distributions as specified in the trust document. When using a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, it's essential for trustees to fulfill these responsibilities.

The grantor creates the trust and specifies its terms, while the trustee is tasked with overseeing and managing the trust. The grantor usually has a vision for the trust, directing how assets should be utilized or distributed. Understanding this distinction is vital, especially when handling a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent.

A trustee manages trust assets, while a guarantor provides assurance to a lender that the borrower will fulfill their obligations. Their roles differ significantly; the trustee has fiduciary responsibilities towards beneficiaries, whereas a guarantor's role is often limited to guaranteeing payment. If you're dealing with a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, knowing your roles can help clarify legal responsibilities.

No, the grantor and trustee are not the same person. The grantor creates the trust and determines its terms, while the trustee administers the trust per those terms. In the context of a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, these roles play distinct but interconnected parts.

No, a trustee is not the same as an owner. The trustee manages the assets in accordance with the trust's terms, while the actual ownership of those assets remains with the beneficiaries. When dealing with a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, it's crucial to understand these roles clearly.

Choosing the right executor is crucial for effective estate management. Ideally, you should select someone who is trustworthy, organized, and knowledgeable about financial matters. Consider a candidate who is familiar with the use of a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent, as this will help ensure that all assets are handled efficiently.

Starting your role as an executor involves several key steps that begin with probate court procedures. You will need to file the decedent's will and related documents, which can vary based on the estate plan. Additionally, having a comprehensive District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent can streamline asset transfer, ensuring as smooth a transition as possible.

To become an executor of an estate in the District of Columbia, you must first be appointed by the probate court. This typically involves filing a petition and providing the court with necessary documents, such as the will and proof of your identity. This legal process may require the use of a District of Columbia Letter of Instruction to Investment Firm Regarding Account of Decedent from Executor / Trustee for Transfer of Assets in Account to Trustee of Trust for the Benefit of Decedent to manage assets effectively.