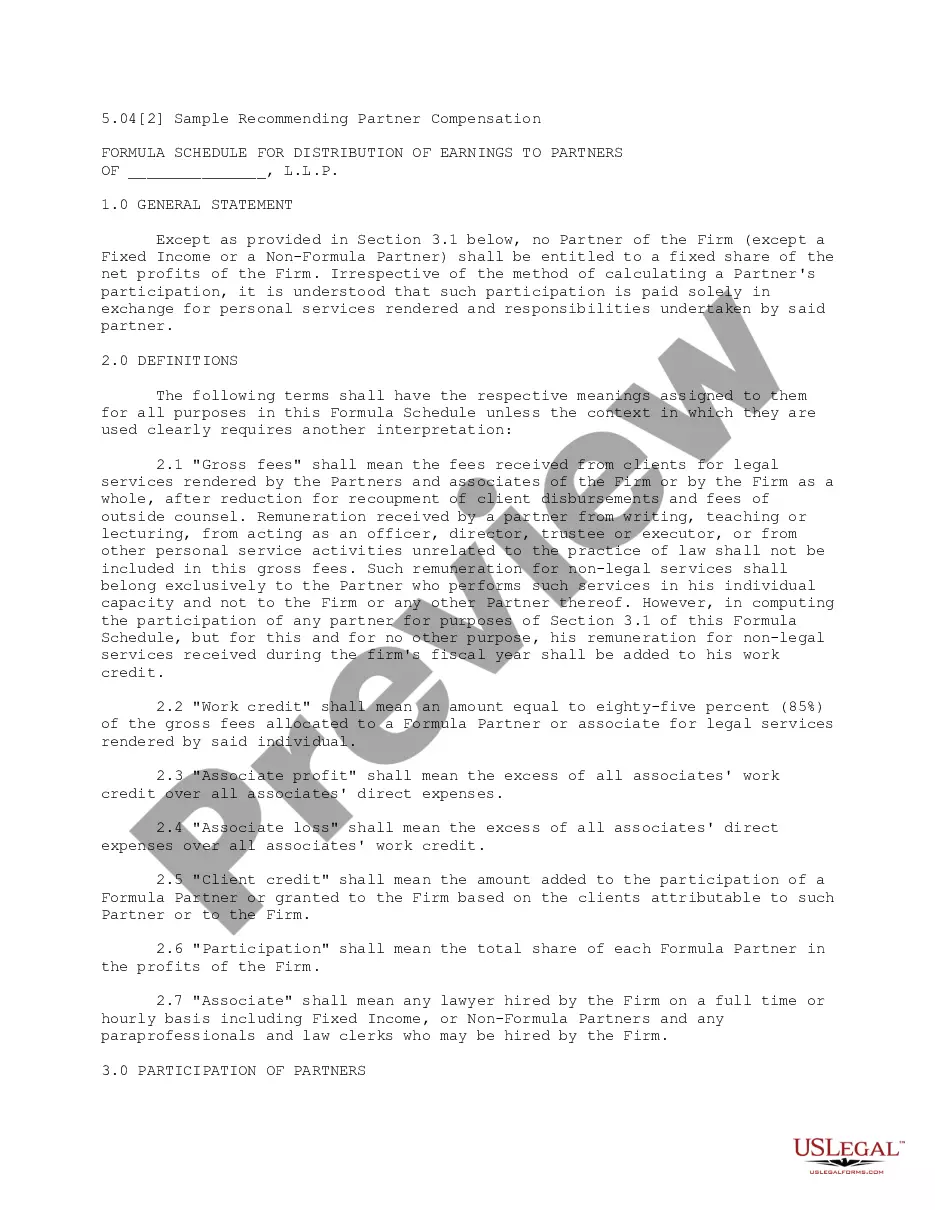

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

Connecticut Formula System for Distribution of Earnings to Partners

Category:

State:

Multi-State

Control #:

US-L05041A

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out Formula System For Distribution Of Earnings To Partners?

You may invest hrs on-line searching for the legal file design that suits the state and federal requirements you will need. US Legal Forms gives thousands of legal varieties that are analyzed by professionals. You can easily download or print the Connecticut Formula System for Distribution of Earnings to Partners from your service.

If you currently have a US Legal Forms accounts, you are able to log in and click the Acquire switch. After that, you are able to comprehensive, change, print, or indicator the Connecticut Formula System for Distribution of Earnings to Partners. Every single legal file design you buy is the one you have permanently. To obtain another duplicate of any acquired kind, proceed to the My Forms tab and click the corresponding switch.

If you use the US Legal Forms site for the first time, keep to the easy recommendations beneath:

- Initially, be sure that you have selected the right file design to the county/town that you pick. See the kind explanation to ensure you have picked the correct kind. If offered, use the Preview switch to appear with the file design also.

- If you wish to discover another edition of the kind, use the Research field to discover the design that meets your requirements and requirements.

- Upon having found the design you need, simply click Acquire now to continue.

- Select the prices prepare you need, enter your qualifications, and register for your account on US Legal Forms.

- Comprehensive the deal. You should use your bank card or PayPal accounts to cover the legal kind.

- Select the format of the file and download it in your product.

- Make modifications in your file if necessary. You may comprehensive, change and indicator and print Connecticut Formula System for Distribution of Earnings to Partners.

Acquire and print thousands of file web templates using the US Legal Forms site, that provides the biggest collection of legal varieties. Use expert and state-certain web templates to deal with your organization or personal requires.

Form popularity

FAQ

Connecticut?sourced income of a part?year resident is the sum of: Connecticut adjusted gross income for the part of the year you were a resident; Income derived from or connected with Connecticut sources for the part of the year you were a nonresident; and. Special accruals.

The law imposes a 6.99 percent tax on partnerships, LLCs, and S corporations. The tax is imposed on either the entity's entire Connecticut-sourced taxable income or an alternative tax base, which reduces taxable income by the percentage of nonresident ownership.

A partnership generally is not a taxable entity. The income, gains, losses, deductions, and credits of a partnership are passed through to the partners based on each partner's distributive share of these items.

If the partnership had income, debit the income section for its balance and credit each partner's capital account based on his or her share of the income. If the partnership realized a loss, credit the income section and debit each partner's capital account based on his or her share of the loss.

"Your spouse will pay income tax on the income that they earn, and you will separately pay income tax on the income that you earn." Translation: don't stress if your partner earns more than you. You're not going to be responsible for footing their bill.

This means that the partnership itself is not subject to tax: any profits are instead taxable on the partners. Generally, for tax purposes each partner is treated as receiving their share of the income and expenses of the partnership as they arise.

Each partner reports their share of the partnership's income or loss on their personal tax return. Partners are not employees and shouldn't be issued a Form W-2. The partnership must furnish copies of Schedule K-1 (Form 1065) to the partner. For deadlines, see About Form 1065, U.S. Return of Partnership Income.

Partnerships Investments by each partner are credited to the partners' capital accounts. Withdrawals from the partnership by a partner are debited to the respective drawing account. The net income for a partnership is divided between the partners as called for in the partnership agreement.