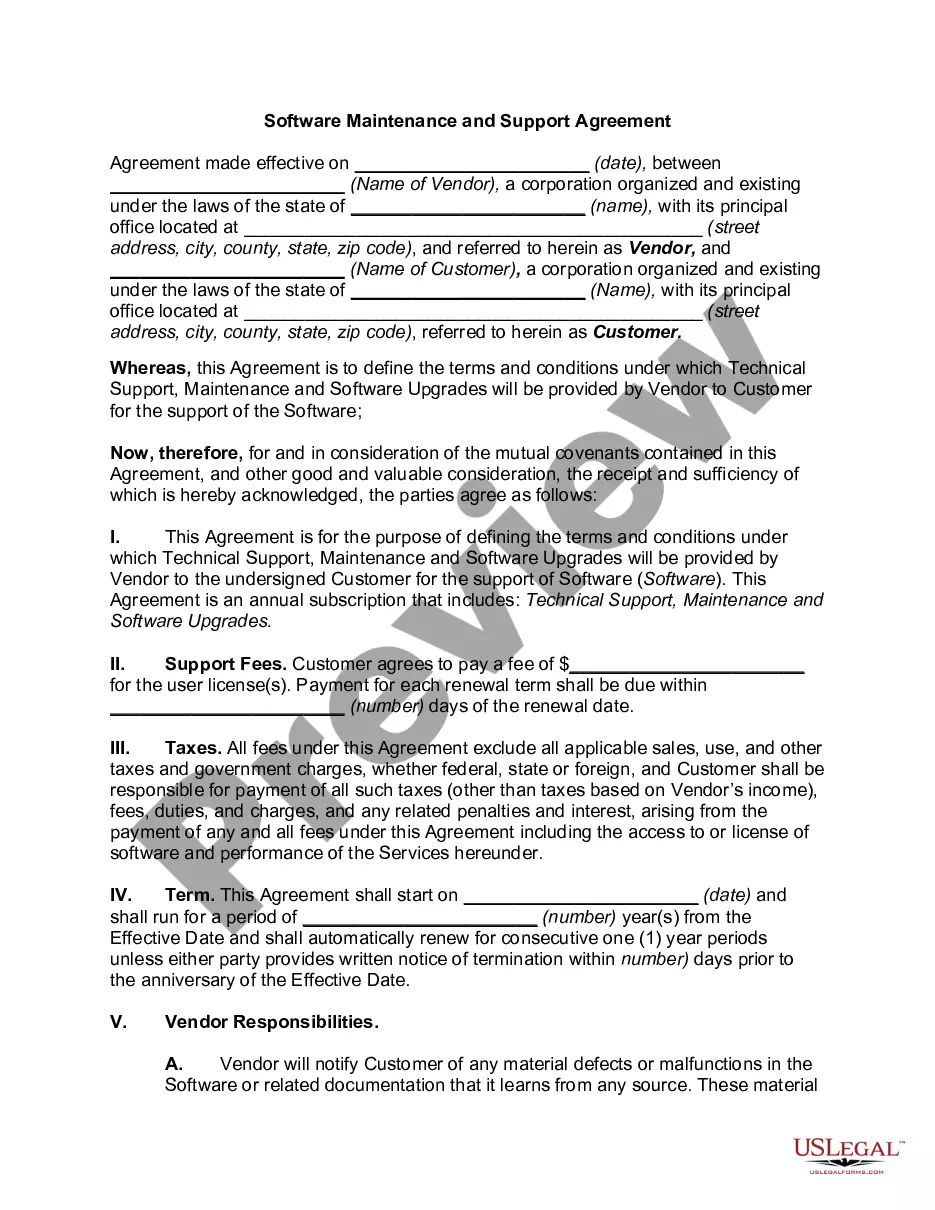

Connecticut Software Maintenance Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

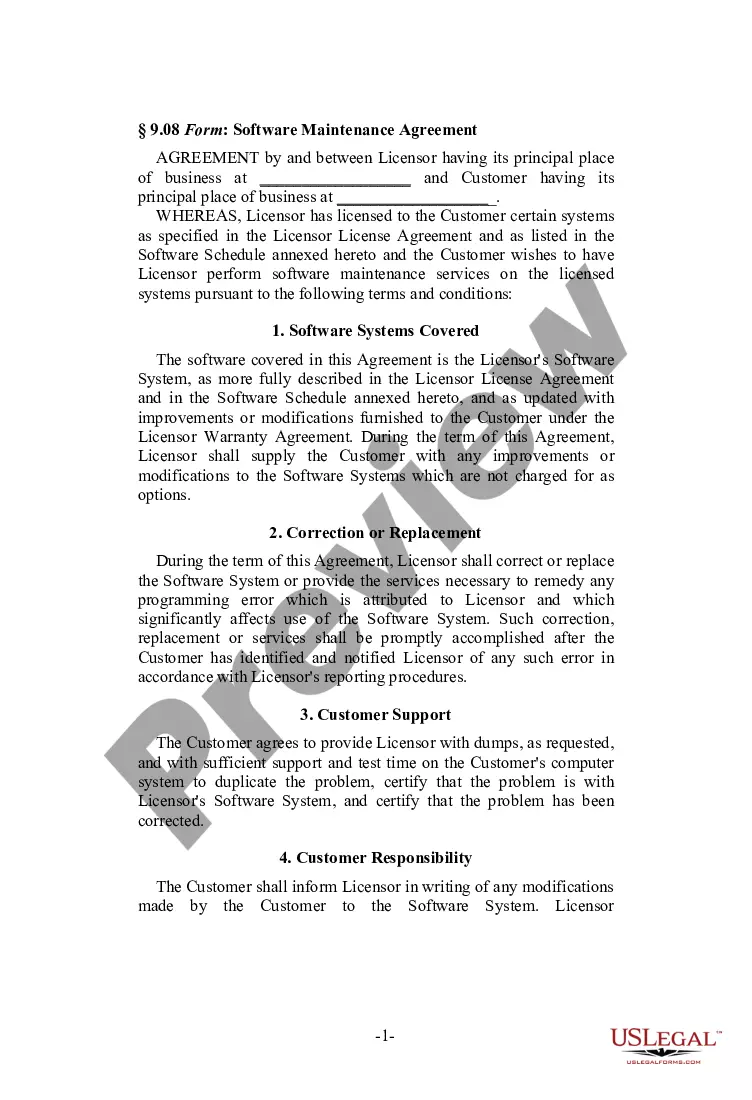

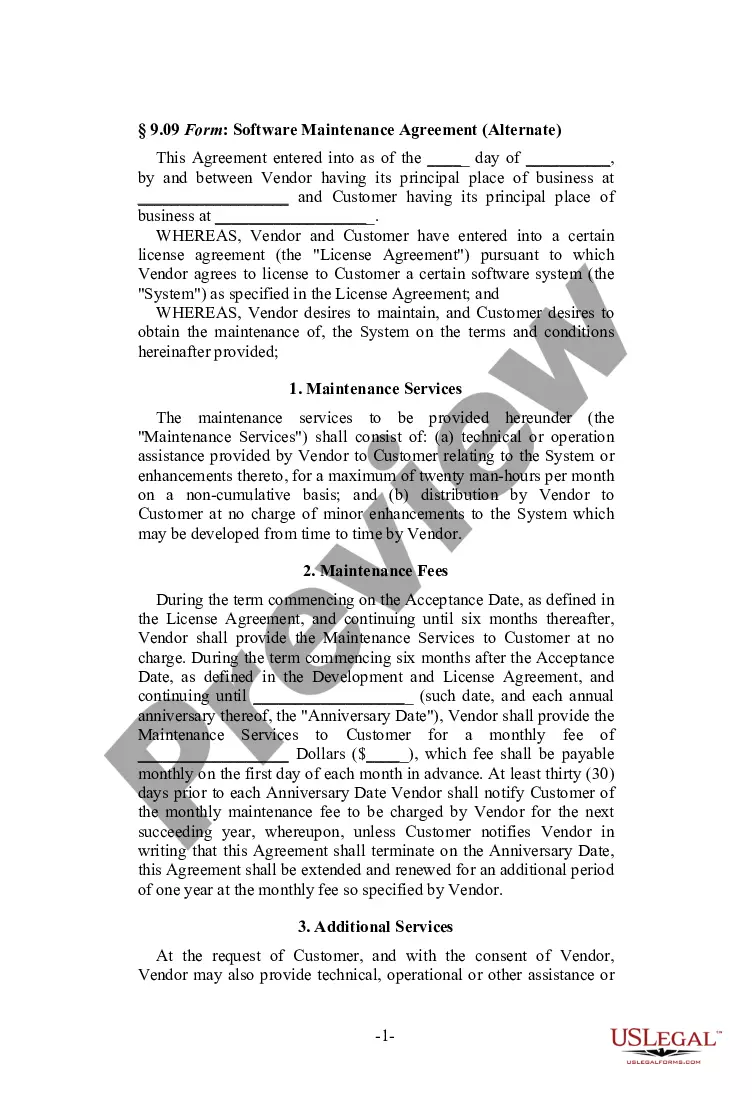

How to fill out Software Maintenance Agreement?

Selecting the top authentic document template might pose challenges. Clearly, there are numerous designs accessible online, but how can you find the valid form you need? Utilize the US Legal Forms website.

The service offers a vast array of templates, including the Connecticut Software Maintenance Agreement, that can be utilized for business and personal purposes. All of the forms are verified by experts and comply with state and federal regulations.

If you are already registered, sign in to your account and hit the Download button to obtain the Connecticut Software Maintenance Agreement. Use your account to browse through the legal forms you may have purchased previously. Check the My documents tab of your account for another copy of the document you need.

Complete, edit, print, and sign the obtained Connecticut Software Maintenance Agreement. US Legal Forms is the largest collection of legal forms where you can find numerous document templates. Utilize the service to download well-crafted documents that adhere to state requirements.

- If you are a new user of US Legal Forms, here are simple steps to follow.

- First, ensure you have selected the correct form for your city/state. You can explore the form using the Review button and examine the form outline to confirm it is the right one for you.

- If the form does not meet your requirements, utilize the Search field to find the appropriate form.

- Once you are confident that the form is suitable, click the Get now button to acquire the form.

- Choose the payment plan you wish and enter the necessary information. Create your account and purchase an order using your PayPal account or credit card.

- Select the document format and download the legal document template to your device.

Form popularity

FAQ

The use tax rate for taxable goods and services is 6%. However, the tax on computer and data processing services is 1%. Examples of taxable tangible personal property include equipment, machines, furniture, appliances, computers, computer software, office supplies, and books.

Maintenance of computer software is a computer and data processing service taxable at the 1% rate, whether the software is prewritten or custom.

California: SaaS is not a taxable service. However, software or information that is delivered electronically is exempt. The ability to access software from a remote network or location is exempt. Under California sales and use tax law, there must be a transfer of TPP, in order to have a taxable event.

Several exemptions are certain types of safety gear, some types of groceries, certain types of clothing, children's car seats, children's bicycle helmets, college textbooks, compact fluorescent light bulbs, most types of medical equipment, and certain motor vehicles.

Generally speaking, access to informational databases are non-taxable in most states either because they are not included in the definition of tangible personal property, or they are not specially identified as taxable services in presumably non-taxable service states, or in a few cases they are specially made exempt

Section 12-407(2)(i)(F) of the Connecticut General Statutes imposes the sales and use tax on "architectural, building engineering and design services" without regard to the type of building which is designed.

Are services subject to sales tax in Connecticut? "Goods" refers to the sale of tangible personal property, which are generally taxable. "Services" refers to the sale of labor or a non-tangible benefit. In Connecticut, specified services are taxable.

Business Use: Electronically accessed or transferred canned or prewritten software, and any additional content related to such software, that is sold to a business for use by the business remains taxable at the 1% rate as computer and data processing services.

The majority of states which have addressed the issue and have concluded that software (at least unbundled software) is not tangible personal property for ad valorem tax purposes and therefore is generally not taxable.

Unless contracts or other documents specifically state otherwise, digital goods will be presumed to be electronically delivered or transferred into Connecticut, and subject to Connecticut sales and use tax, if the billing address of the consumer or subscriber is in Connecticut.