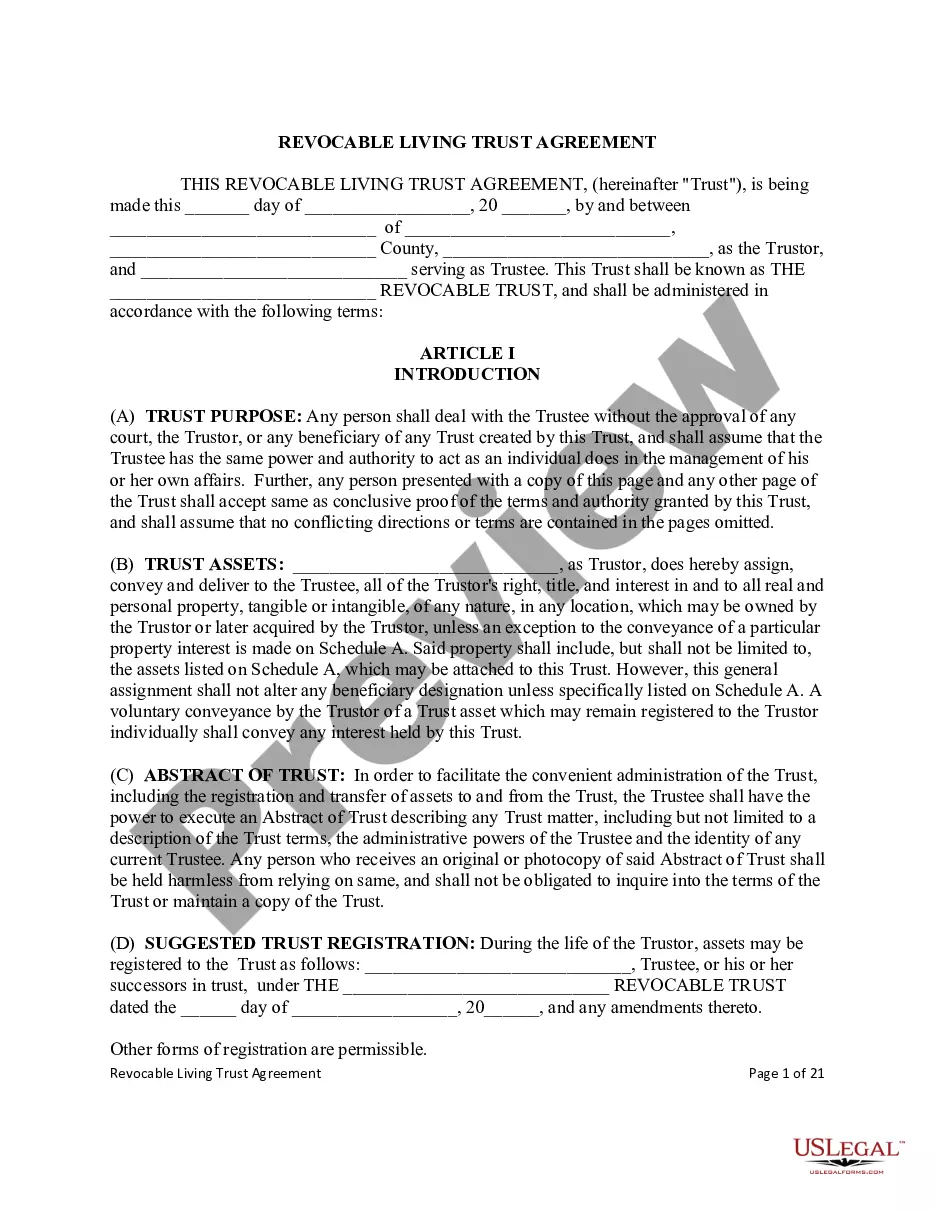

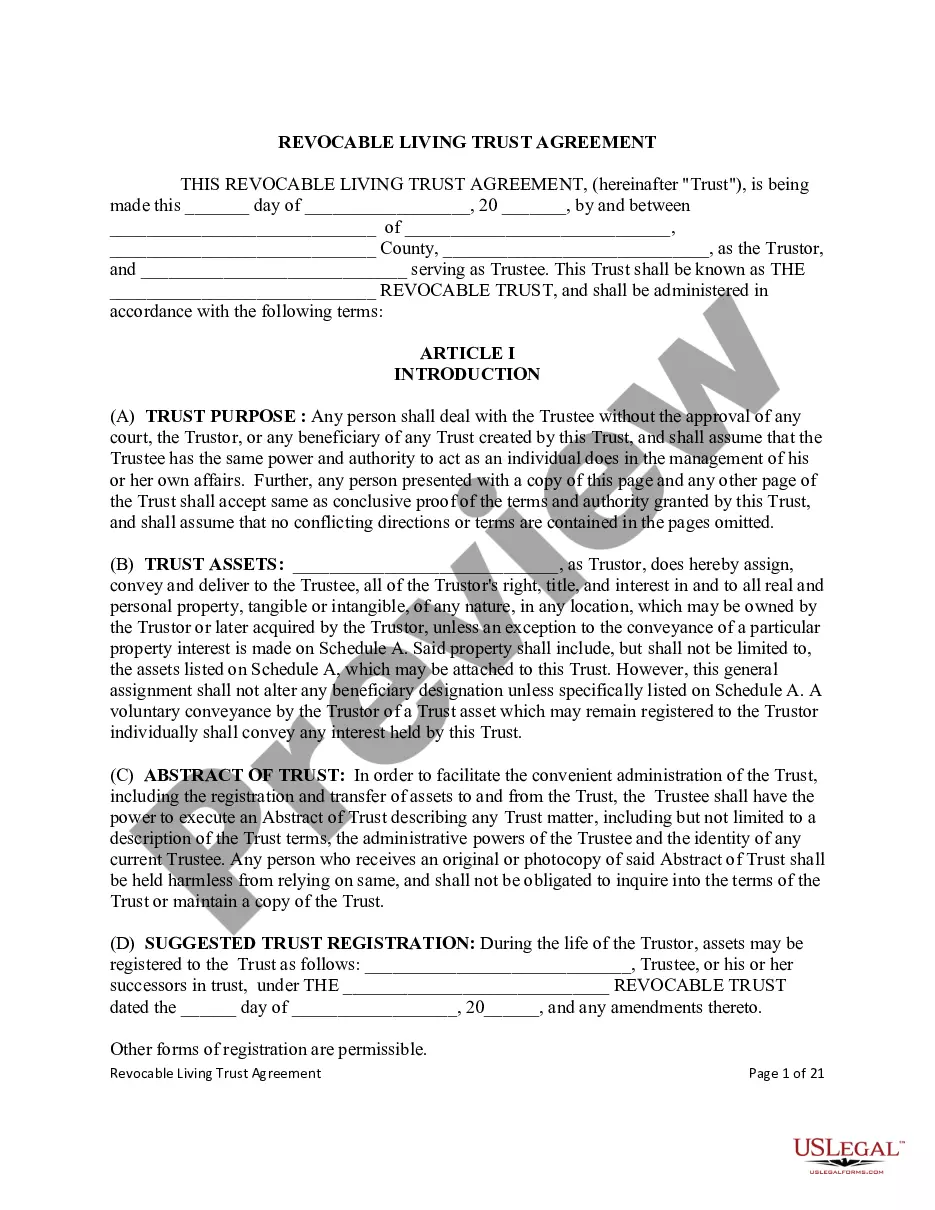

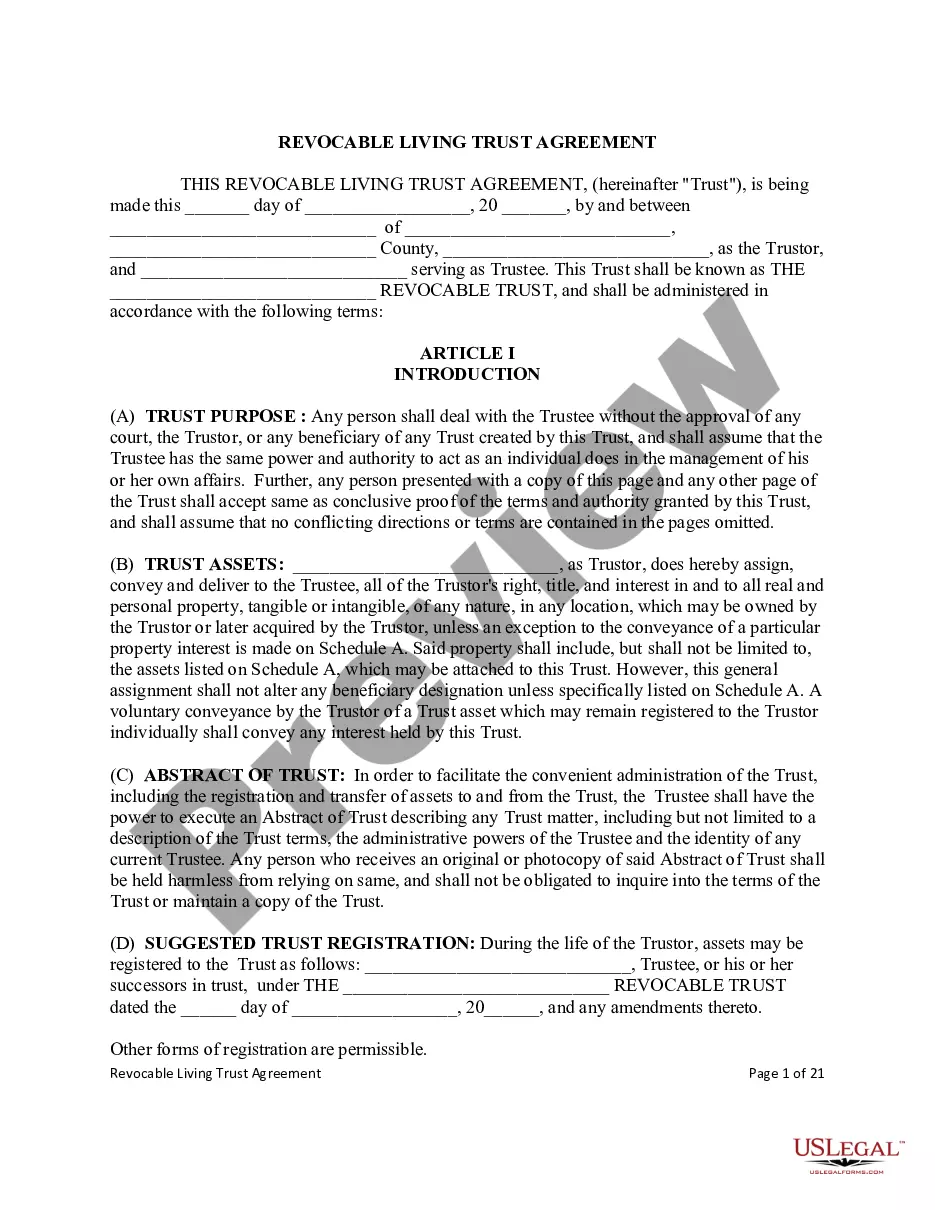

Connecticut Living Trust with Provisions for Disability

Description

How to fill out Living Trust With Provisions For Disability?

You can spend time online trying to locate the legal document template that meets the state and federal criteria you will require.

US Legal Forms offers a vast array of legal forms that have been reviewed by professionals.

You can conveniently download or print the Connecticut Living Trust with Provisions for Disability from my service.

If available, take advantage of the Preview button to review the document format as well.

- If you already possess a US Legal Forms account, you can Log In and click on the Acquire button.

- After that, you can complete, modify, print, or sign the Connecticut Living Trust with Provisions for Disability.

- Every legal document template you obtain is your own for an extended period.

- To obtain an additional copy of a purchased form, go to the My documents tab and click on the corresponding button.

- If you're using the US Legal Forms site for the first time, adhere to the simple instructions below.

- First, ensure you have selected the correct document format for your region/city of choice.

- Review the form description to make certain you have chosen the correct template.

Form popularity

FAQ

A Trust that does not require distribution of all its income by the terms of the trust agreement is called a Complex Trust, and is allowed an exemption of $100. A Qualified Disability Trust or QDT is allowed the same exemption as an individual under IRS Code §642(b)(2)(C).

Using a Special Needs Trust Fortunately, there is a simple way to accept an inheritance without risking loss of SSI benefits. By setting up a special needs trust and depositing the inheritance into it, the beneficiary can continue to receive SSI while also getting the benefit of the inheritance.

In 2003, Congress added a section to the Internal Revenue Code allowing disability trusts to qualify for a special personal exemption. Trusts that meet the requirements of this law are called qualified disability trusts.

In cases of spendthrift or other concerns, an accumulation trust provides the greatest option. Perhaps the greatest advantage of an accumulation trust is you can have the best of both worlds, that is if you choose to distribute all RMD out in the year received to have it operate like a conduit trust.

Most special needs trusts are subject to accumulation trusts rules because they are typically, and often must be, discretionary trusts where the trustee has the choice either to pay or to withhold income and/or principal.

If you use your assets to establish a trust on or after January 1, 2000, generally, the trust will count as your resource for SSI. In the case of a revocable trust, the whole trust is your resource.

As far as assets are concerned, to be eligible for SSI, an applicant can have no more than $2,000 in assets ($3,000 for a couple), a figure that has not changed since 1989. If the applicant can use or liquidate an asset to pay for food or shelter, the asset will probably count as a "resource" against this limit.

A Special Disability Trust (SDT) is a special type of trust that allows parents and immediate family members to plan for current and future needs of a person with severe disability. The trust can pay for reasonable care, accommodation and other discretionary needs of the beneficiary during their lifetime.

A special needs trust is a trust tailored to a person with special needs that is designed to manage assets for that person's benefit while not compromising access to important government benefits.

The short answer is that there's no difference. Here's the long answer: When the field of special needs planning began more than two decades ago, trusts created for people with disabilities were generally called supplemental needs trusts.