Connecticut Chapter 13 Plan

Understanding this form

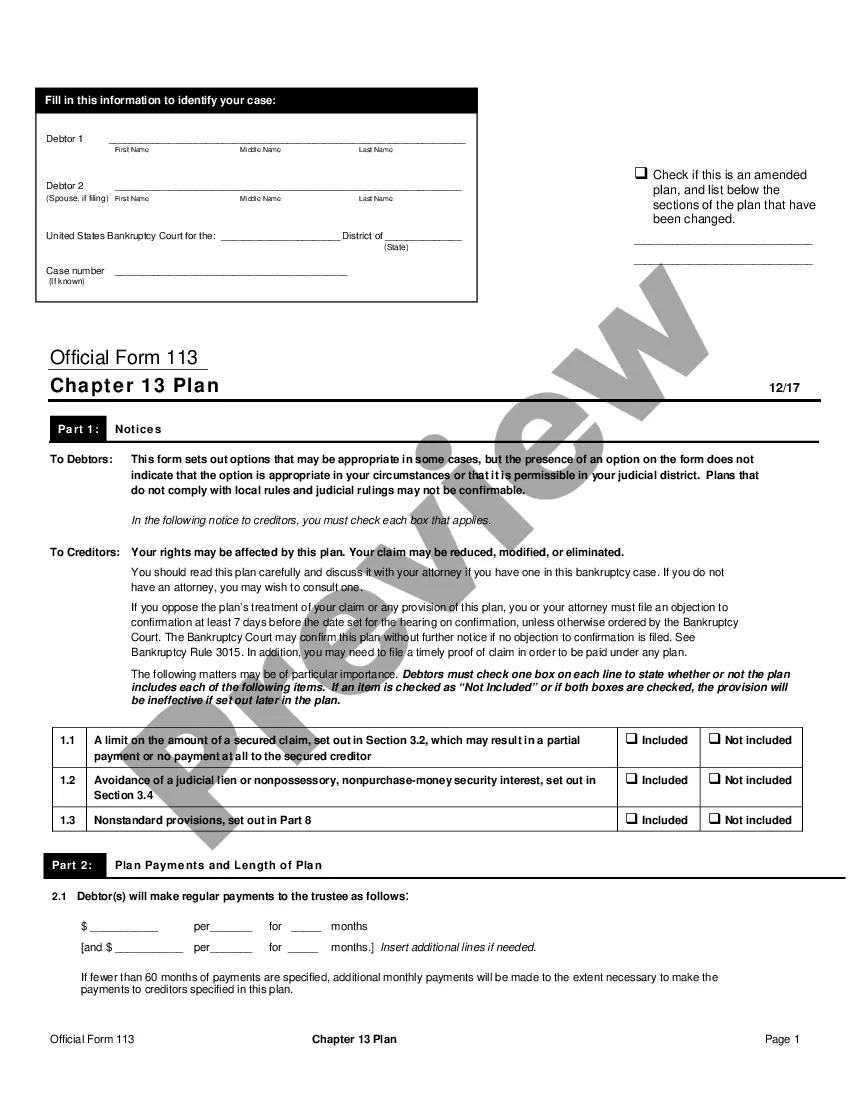

The Chapter 13 Plan is a legal document that outlines how a debtor proposes to repay creditors over a specified period, typically three to five years. It is specifically designed for individuals who want to reorganize their debts while keeping their property, distinguishing it from Chapter 7 bankruptcy, which liquidates assets. This form includes details about priority claims, secured claims, general unsecured claims, and the fees for the debtor's attorney, establishing a clear framework for managing financial obligations during bankruptcy proceedings.

Key components of this form

- Details of priority claims that must be paid in full.

- Information regarding secured claims recognized under the plan.

- Outline of general unsecured claims and their treatment.

- Specification of the debtor's attorney's fees and payment schedule.

When to use this document

This form should be used when an individual needs to propose a repayment plan as part of a Chapter 13 bankruptcy filing. It is suitable for those who have a regular income and wish to keep their property while repaying debts over time. Common scenarios include preventing foreclosure, stopping wage garnishment, or addressing significant medical expenses.

Who this form is for

This form is intended for:

- Individuals filing for Chapter 13 bankruptcy.

- Debtors who wish to propose a repayment plan to manage their debts.

- People looking to protect their assets from liquidation.

How to prepare this document

To complete the Chapter 13 Plan, follow these steps:

- Identify the debtor's details, including name and address.

- List and categorize all claims, specifying priority and secured claims.

- Detail the proposed repayment schedule and amounts for each claim.

- Include attorney fees and clarify payment arrangements.

- Sign and date the form to validate the proposal.

Does this form need to be notarized?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to categorize claims correctly, which can affect repayment priorities.

- Omitting important details about income or expenses, leading to inaccuracies.

- Not signing or dating the form, which can invalidate the submission.

Benefits of completing this form online

- Convenient access to legal documents without needing to visit a lawyer.

- Editable templates allow for customization to fit individual circumstances.

- Reliable resources drafted by licensed attorneys ensure legal compliance.

Legal use & context

- The Chapter 13 Plan serves as a binding agreement approved by the bankruptcy court.

- Failure to adhere to the established plan can result in dismissal of the bankruptcy case.

- Plans must comply with relevant federal laws, including fair treatment of all creditors.

Main things to remember

- The Chapter 13 Plan allows individuals to repay debts while keeping their assets.

- It is crucial to accurately categorize claims to uphold legal standards.

- Using this form online provides convenience and access to expert-drafted content.

Looking for another form?

Form popularity

FAQ

To start filing for a Connecticut Chapter 13 Plan, first gather your financial documents, including income statements and an inventory of your debts. Next, consider consulting with a bankruptcy attorney or using platforms like uslegalforms to help guide you through the filing process. Completing the necessary paperwork accurately is essential to ensure your case proceeds smoothly.

Yes, it is possible to be denied a Connecticut Chapter 13 Plan. Reasons for denial often include failing to meet eligibility requirements or providing incomplete or inaccurate information. To increase your chances of approval, ensure your application is thorough and accurate, and consider using uslegalforms for assistance in preparing your documents.

Under current guidelines for a Connecticut Chapter 13 Plan, your unsecured debt must be less than $394,725. Additionally, your secured debts should be under $1,184,200. Keeping these limits in mind as you evaluate your financial status can help you effectively plan your next steps toward filing.

To file for a Connecticut Chapter 13 Plan, you must have a regular income and unsecured debts under $394,725, and secured debts under $1,184,200. These limits can change, so it's wise to check for the latest figures to ensure you qualify. Understanding your total debt helps you make informed decisions about your financial future.

While it is possible to file for a Connecticut Chapter 13 Plan without an attorney, it's generally not recommended. The process can be complex, and errors in paperwork could lead to your case being dismissed. By using services like uslegalforms, you can navigate the process more smoothly and ensure all necessary documents are completed correctly.

The average monthly payment for a Connecticut Chapter 13 Plan varies based on individual circumstances, including income, expenses, and the amount of debt. Generally, it can range between $200 to $1,500, depending on your financial situation. A qualified attorney can help you determine a realistic payment plan that meets your needs and adheres to the requirements of the court.

You may become ineligible for a Connecticut Chapter 13 Plan for various reasons. If your secured and unsecured debts exceed the federal limits, or if you fail to make required payments in a previous bankruptcy case, you won't qualify. Furthermore, having a recent bankruptcy discharge can also impact your eligibility.

To file a Connecticut Chapter 13 Plan, you first need to complete a credit counseling course. After that, you gather your financial documents and file a petition with the bankruptcy court. It's advisable to consult legal resources or platforms like uslegalforms to ensure you follow the correct procedures and maximize the benefits of your plan.

Several factors can disqualify you from filing a Connecticut Chapter 13 Plan. If you have previously filed for Chapter 13 and failed to complete the plan, or have received a discharge under this chapter within the last two years, you may be ineligible. Additionally, failing to meet income or debt limits can also disqualify you.

Yes, a Connecticut Chapter 13 Plan can be denied under specific circumstances. If the plan does not meet legal requirements or if you fail to propose a feasible repayment plan, the court may reject it. It's crucial to ensure your plan is well-structured and in compliance to improve your chances of approval.