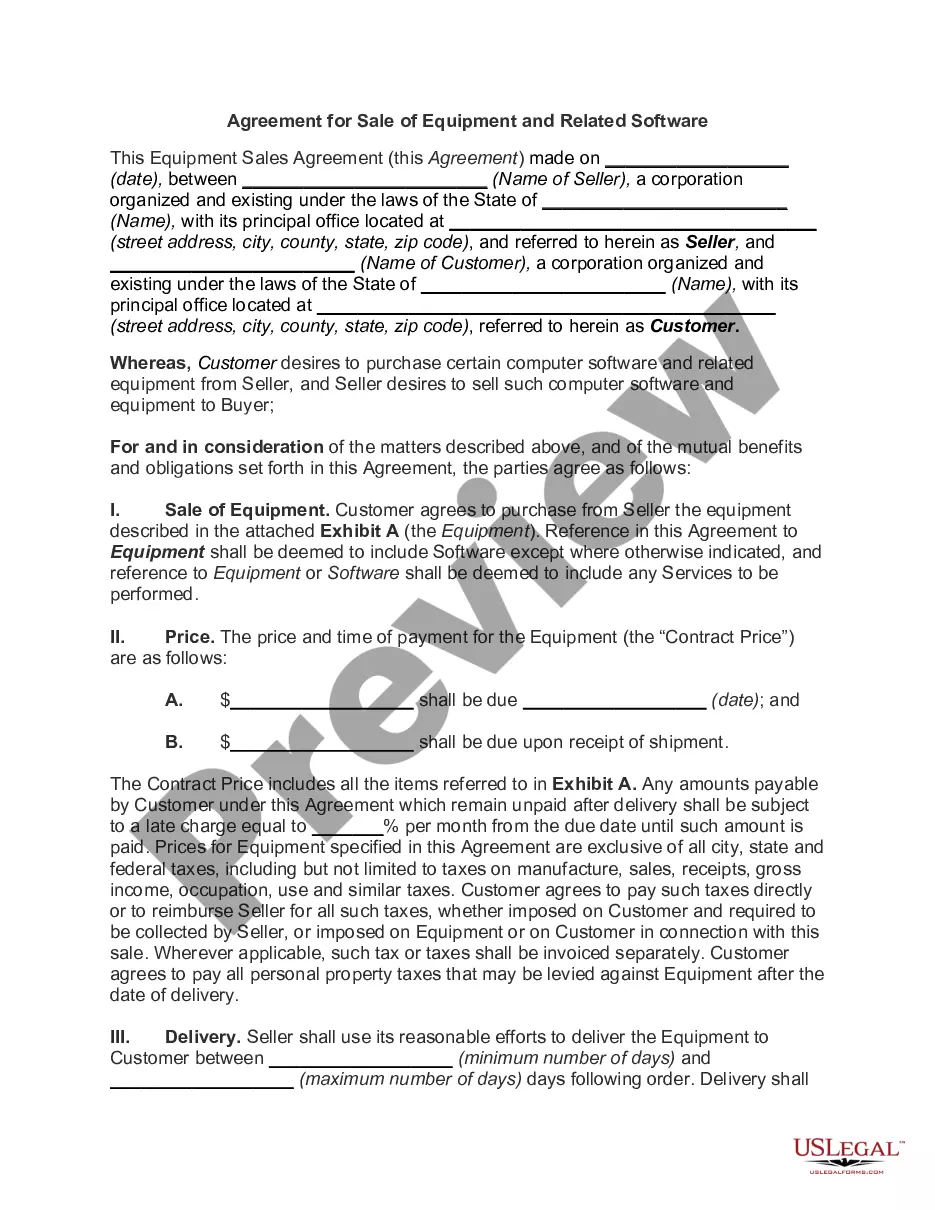

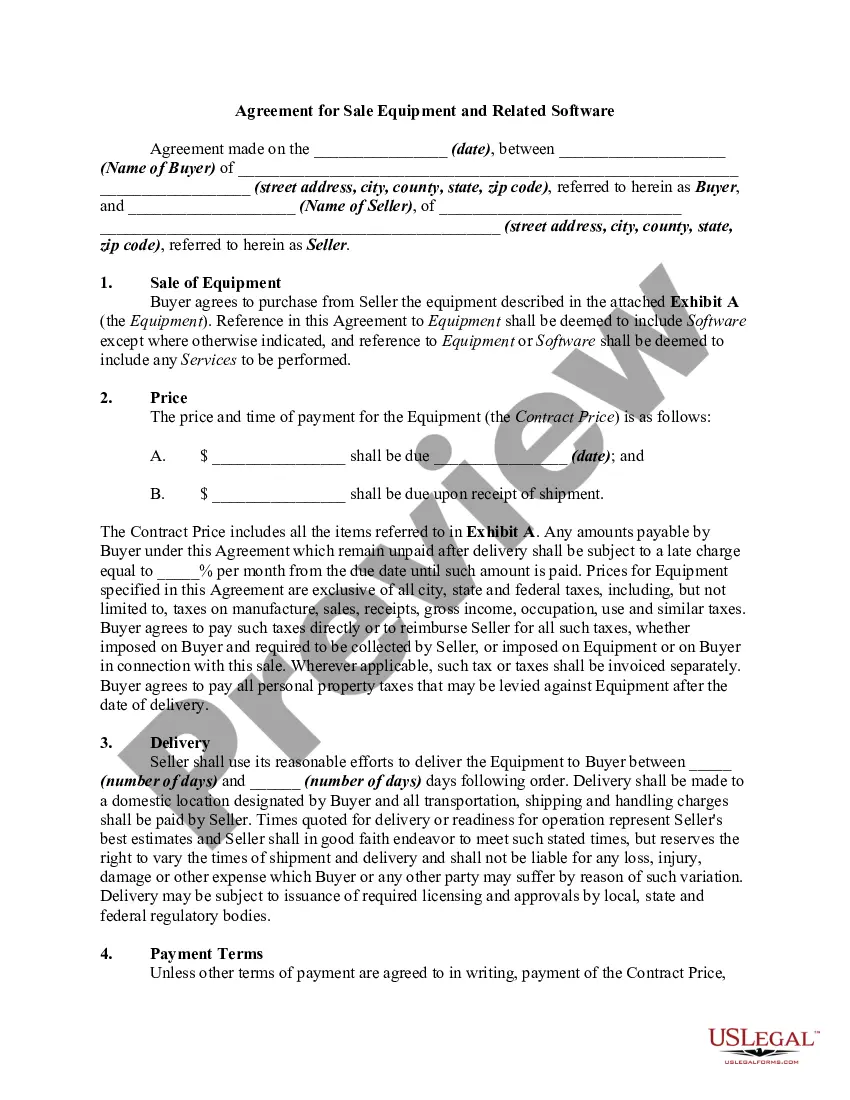

Colorado Agreement for Sales of Data Processing Equipment

Description

How to fill out Agreement For Sales Of Data Processing Equipment?

You might spend numerous hours online looking for the legal document template that fulfills the federal and state requirements you need.

US Legal Forms offers thousands of legal documents that are evaluated by professionals.

It is easy to obtain or print the Colorado Agreement for Sales of Data Processing Equipment from the service.

Review the form description to ensure you have chosen the correct form. If available, use the Preview button to look through the document template as well. If you wish to find another version of your form, use the Search field to discover the template that suits your needs and requirements. Once you have found the template you want, click on Acquire now to proceed. Select the pricing plan you desire, enter your credentials, and register for a free account on US Legal Forms. Complete the transaction. You can use your Visa or Mastercard or PayPal account to pay for the legal form. Choose the format of your document and download it to your device. Make adjustments to your document if necessary. You can complete, modify, sign, and print the Colorado Agreement for Sales of Data Processing Equipment. Access and print thousands of document templates using the US Legal Forms site, which provides the largest selection of legal forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you already have a US Legal Forms account, you can Log In and click on the Obtain button.

- Afterward, you can complete, modify, print, or sign the Colorado Agreement for Sales of Data Processing Equipment.

- Every legal document template you purchase is yours permanently.

- To get another copy of a purchased form, visit the My documents tab and click on the corresponding button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure you have selected the correct document template for your county/city of preference.

Form popularity

FAQ

To obtain a sales tax exemption certificate in Colorado, you need to complete the Colorado Sales Tax Exemption Certificate, Form DR 0592. This certificate is essential for businesses that qualify for exemptions, such as those involving the Colorado Agreement for Sales of Data Processing Equipment. You can easily access the necessary forms and guidance through the US Legal Forms platform, streamlining the process for you.

Yes, in Colorado, the sale of software can be subject to sales tax, especially if it is delivered in tangible form or as part of a service. However, the Colorado Agreement for Sales of Data Processing Equipment may provide specific conditions under which software sales may be exempt. To navigate these regulations effectively, consider consulting the US Legal Forms platform for comprehensive resources.

To report taxable sales in Colorado, businesses must file the Colorado Sales Tax Return, specifically Form DR 0100. This form helps you detail your sales, including those related to the Colorado Agreement for Sales of Data Processing Equipment, ensuring compliance with state tax laws. It’s crucial to file this return accurately and on time to avoid penalties.

In Colorado, certain items are exempt from sales tax, including food for home consumption, prescription medications, and some agricultural products. Additionally, the Colorado Agreement for Sales of Data Processing Equipment may provide specific exemptions related to technology and equipment sales. It is essential to consult the latest state regulations or a tax professional to understand fully which items qualify for exemption.

Yes, computer software is taxable in Colorado unless it qualifies for specific exemptions. This includes any software utilized in connection with data processing equipment as described in the Colorado Agreement for Sales of Data Processing Equipment. If you have questions about your specific situation, consulting a tax expert or referring to resources like USLegalForms can provide clarity.

In Colorado, certain services are subject to sales tax, including some data processing services and repair services for tangible goods. It's essential to distinguish between taxable and non-taxable services to avoid surprises. When dealing with agreements such as the Colorado Agreement for Sales of Data Processing Equipment, you may find relevant details about which services apply.

In Colorado, the sales tax on electronics can vary depending on the jurisdiction, but at the state level, the base sales tax rate is 2.9%. Additionally, local taxes may apply, so it's important to check local rates when considering purchases, such as those outlined in the Colorado Agreement for Sales of Data Processing Equipment. Staying informed helps you budget effectively for any electronics acquisition.

The bulk sales law in Colorado governs the sale of a substantial part of a business's inventory and assets. This law aims to protect creditors by requiring sellers to notify them before executing a bulk sale. If you are entering an agreement related to a sale of data processing equipment, such as under the Colorado Agreement for Sales of Data Processing Equipment, understanding these regulations is crucial.

Yes, software is typically subject to sales tax in Colorado. Under the regulations, tangible personal property includes software, making it taxable unless it complies with specific exemptions. When acquiring software for data processing equipment, it's vital to refer to the Colorado Agreement for Sales of Data Processing Equipment to understand your tax obligations fully.

In general, computer software that is considered a business expense may be tax deductible. This could potentially include software used for the management of data processing equipment as outlined in the Colorado Agreement for Sales of Data Processing Equipment. It's essential to keep detailed records of your software purchases and consult a tax professional to ensure full compliance with tax regulations.