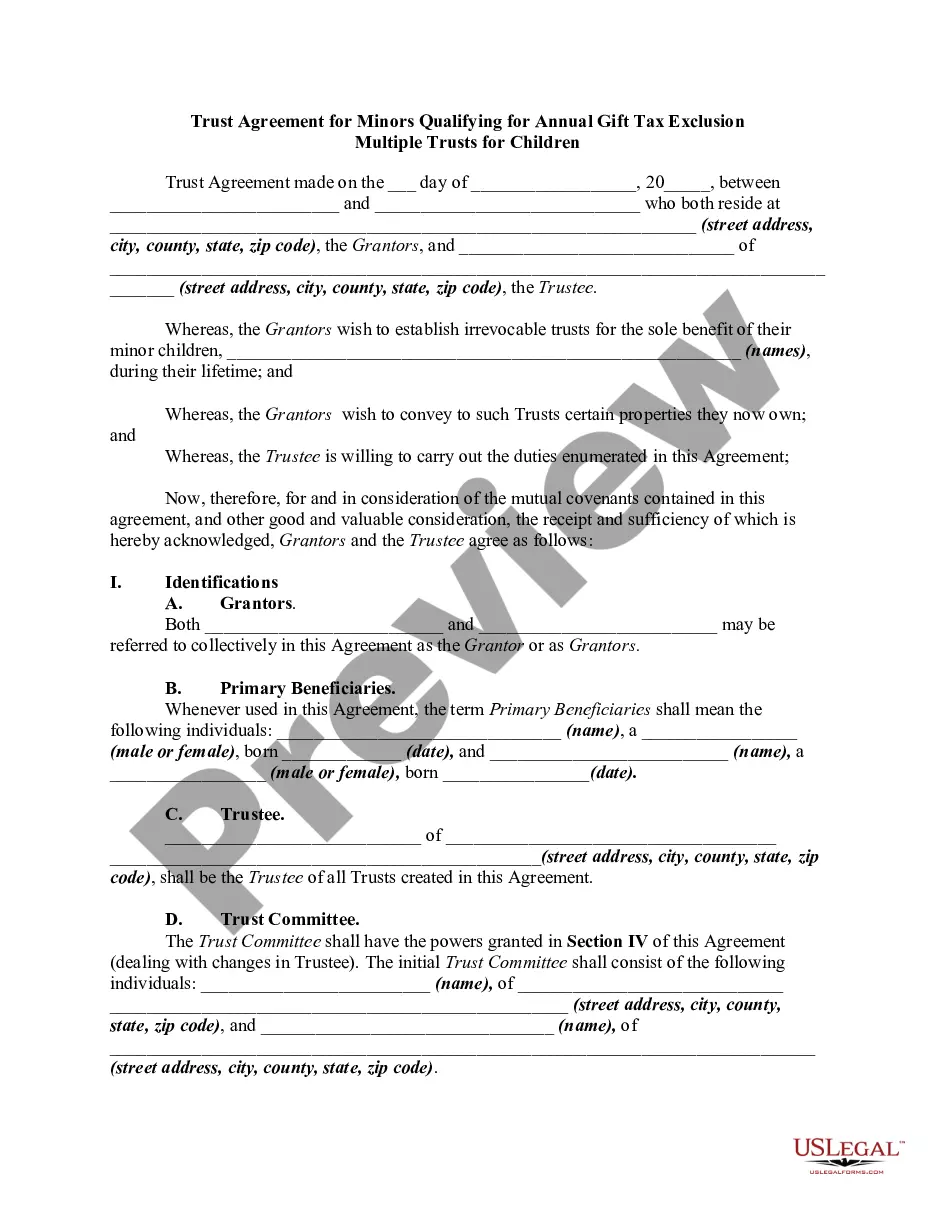

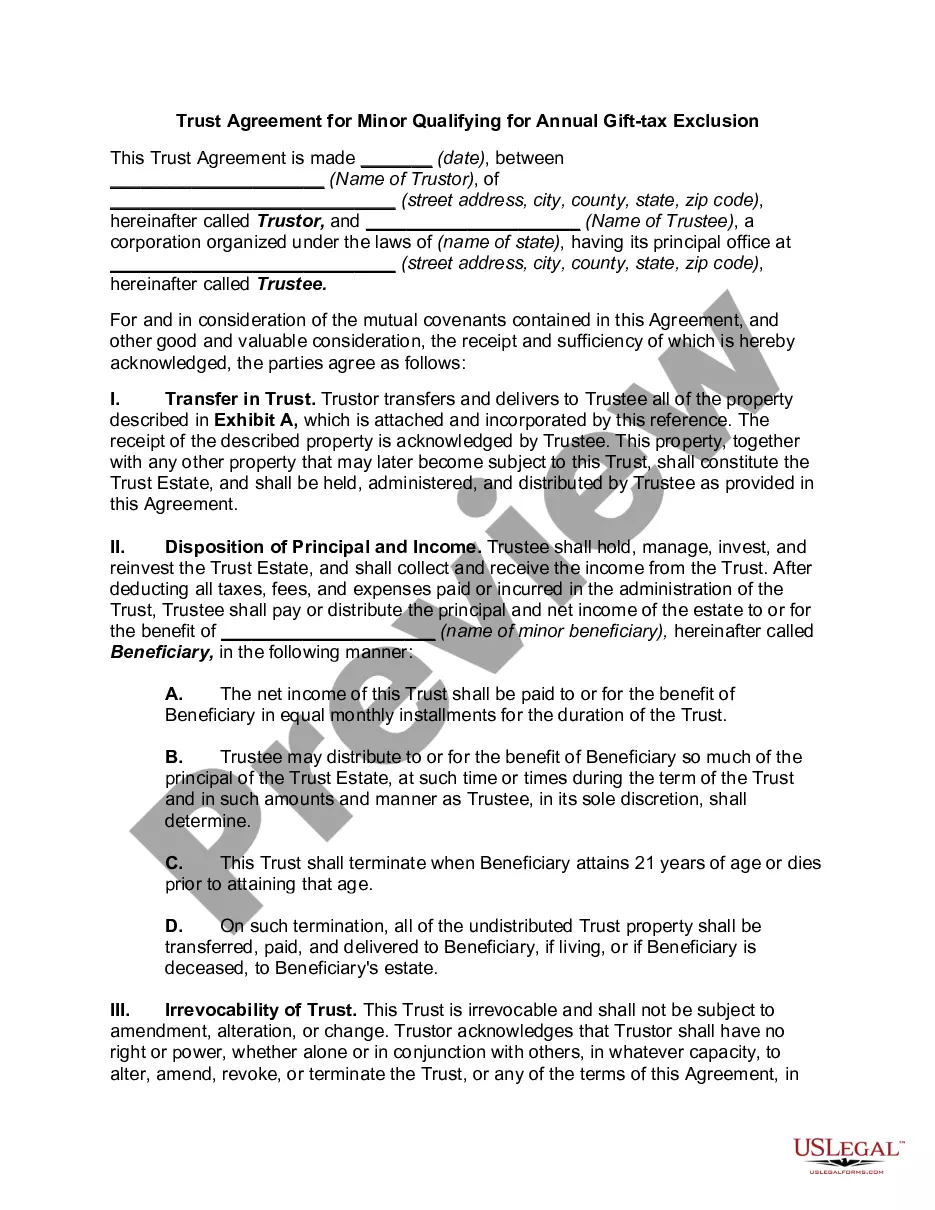

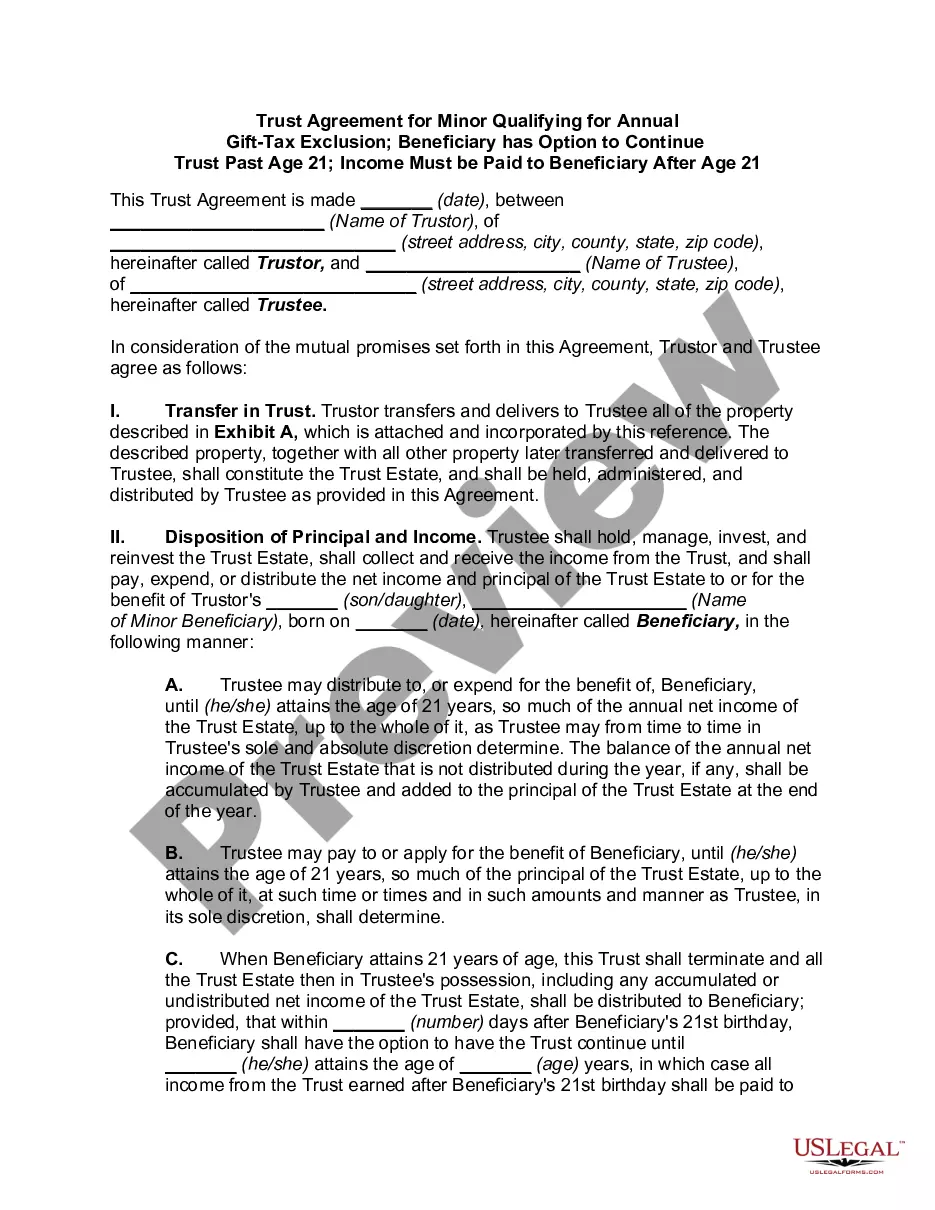

Colorado General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

You can spend hours online searching for the proper legal document template that complies with the federal and state requirements you need.

US Legal Forms provides thousands of legal documents that are assessed by experts.

It is easy to download or print the Colorado General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion from the platform.

First, make sure you have selected the correct document template for the county/city you wish. Review the form details to confirm you have chosen the right document. If available, use the Review button to examine the document template as well.

- If you possess a US Legal Forms account, you can sign in and then hit the Download button.

- After that, you can complete, edit, print, or sign the Colorado General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

- Every legal document template you obtain is yours indefinitely.

- To receive another copy of any purchased form, navigate to the My documents section and click the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the simple instructions provided below.

Form popularity

FAQ

Yes, the gift associated with creating a Grantor Retained Annuity Trust (GRAT) might qualify for the annual gift tax exclusion under certain circumstances. When you use the Colorado General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, it is essential to structure the trust appropriately to ensure that the gifts made meet the criteria for exclusion. Understanding this can significantly benefit your estate planning and tax strategies.

Gifts to Beneficiary You control the amount and timing of these gifts through the terms of the trust. The trust can limit annual gifts to a younger beneficiary, for example, or to a beneficiary who may be careless with money.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

Qualifying gifts to an irrevocable trust for the annual gift tax exclusion will involve giving the beneficiary either the right, for a limited time, to withdraw assets given to the trust (a "Crummey withdrawal right") or the use of a trust that lasts only until the beneficiary reaches age 21.

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.

The key difference between a 2503(c) trust and a 2503(b) trust is the distribution requirement. Parents who are concerned about providing a child or other beneficiary with access to trust funds at age 21 might be better off with a 2503(b), since there is no requirement for access at age 21.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

A gift in trust is a special legal and fiduciary arrangement that allows for an indirect bequest of assets to a beneficiary. The purpose of a gift in trust is to avoid the tax on gifts that exceed the annual gift tax exclusion limit. This type of trust is commonly used to transfer wealth to the next generation.

The trust allows the trustee to gift from the trust to the current beneficiary's issue up to the annual gift exclusion (currently $15K).

The IRS does not levy gift taxes on trusts, nor does it consider payments from the trust to a beneficiary as a gift (it may be taxable income to the beneficiary, however).