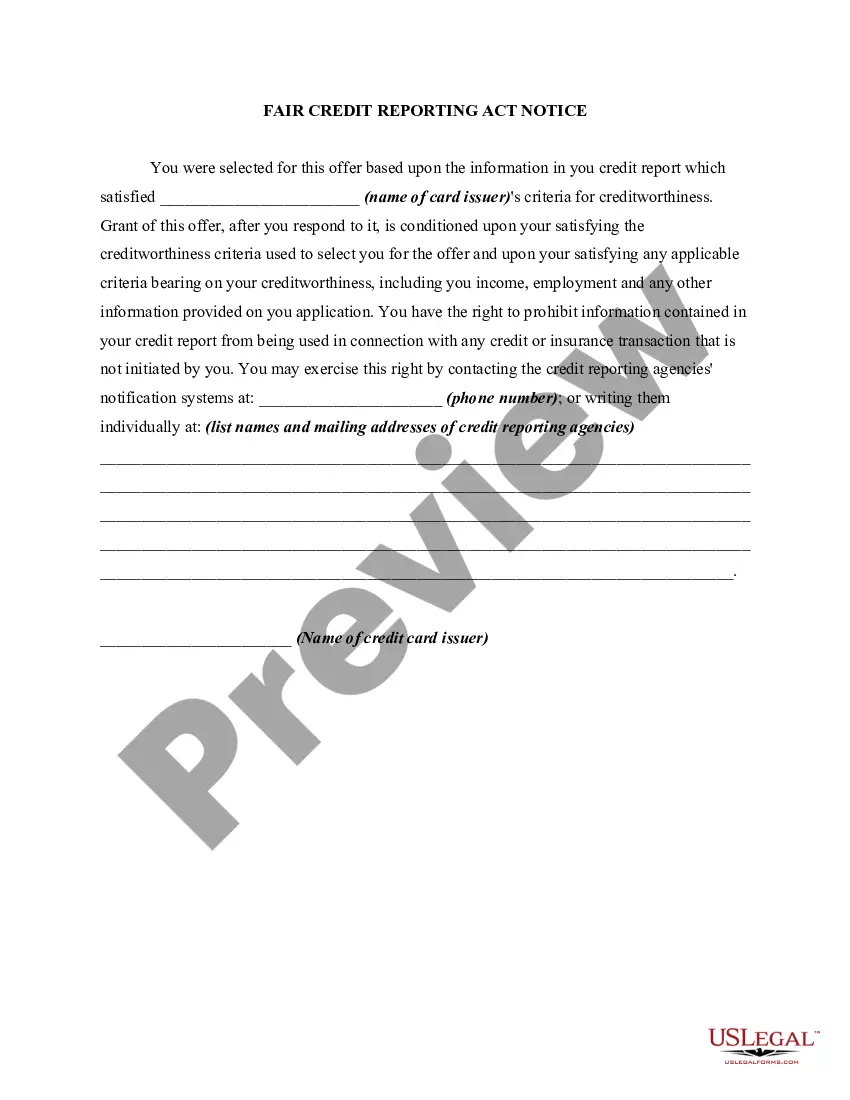

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Colorado Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

US Legal Forms - one of several biggest libraries of authorized types in the USA - delivers a variety of authorized document web templates you can down load or print. Making use of the web site, you will get 1000s of types for company and individual purposes, categorized by classes, says, or keywords and phrases.You can find the latest versions of types much like the Colorado Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency within minutes.

If you already have a subscription, log in and down load Colorado Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency from the US Legal Forms library. The Down load switch will appear on every form you perspective. You have access to all in the past acquired types within the My Forms tab of your bank account.

If you wish to use US Legal Forms for the first time, listed below are straightforward recommendations to help you started out:

- Be sure you have chosen the proper form for the city/county. Select the Preview switch to examine the form`s content. Read the form description to actually have chosen the proper form.

- When the form doesn`t suit your specifications, make use of the Look for discipline towards the top of the screen to discover the one that does.

- When you are satisfied with the shape, verify your choice by clicking the Get now switch. Then, pick the prices strategy you want and offer your qualifications to sign up for the bank account.

- Procedure the deal. Make use of your Visa or Mastercard or PayPal bank account to finish the deal.

- Choose the structure and down load the shape on your gadget.

- Make changes. Fill out, change and print and indication the acquired Colorado Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency.

Each and every format you included in your account does not have an expiration time and is yours forever. So, if you would like down load or print an additional backup, just visit the My Forms segment and click on about the form you need.

Obtain access to the Colorado Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency with US Legal Forms, probably the most considerable library of authorized document web templates. Use 1000s of expert and express-certain web templates that meet your small business or individual requires and specifications.

Form popularity

FAQ

Section 623(a)(5): Duty of furnishers to provide date of delinquency on charge-off, collection or similar accounts | Federal Trade Commission.

Section 1681a of the Fair Credit Reporting Act defines an ?investigative consumer report? as ?a consumer report or portion thereof in which information on a consumer's character, general reputation, personal characteristics, or mode of living is obtained through personal interviews with neighbors, friends, or ...

Reporting of Medical Debt: The three major credit bureaus (Equifax, Transunion, and Experian) will institute a new policy by March 30, 2023, to no longer include medical debt under a dollar threshold (the threshold will be at least $500) on credit reports.

Federal Legislative Activity in 2023 Amend Section 604(c) of the FCRA to address the treatment of pre-screening report requests. Section 604(c) governs the furnishing of reports in connection with credit or insurance transactions that are not initiated by the consumer.

Sections 623(a)(1)(A) and (a)(1)(C). If at any time a person who regularly and in the ordinary course of business furnishes information to one or more CRAs determines that the information provided is not complete or accurate, the furnisher must promptly provide complete and accurate information to the CRA.

Under Colorado law, a consumer reporting agency shall, upon written or verbal request and proper identification of any consumer, clearly, accurately, and in a manner that is understandable to the consumer, disclose to the consumer, in writing, all information in its files at the time of the request pertaining to the ...

(a) Every consumer reporting agency shall, upon request and proper identification of any consumer, clearly and accurately disclose to the consumer: (1) The nature and substance of all information (except medical information) in its files on the consumer at the time of the request.

Duty to Promptly Correct and Update Information. Section 623(a) of the FCRA also requires a person who regularly furnishes information to CRAs to promptly notify a CRA if the person determines the previously furnished information is not complete or accurate.