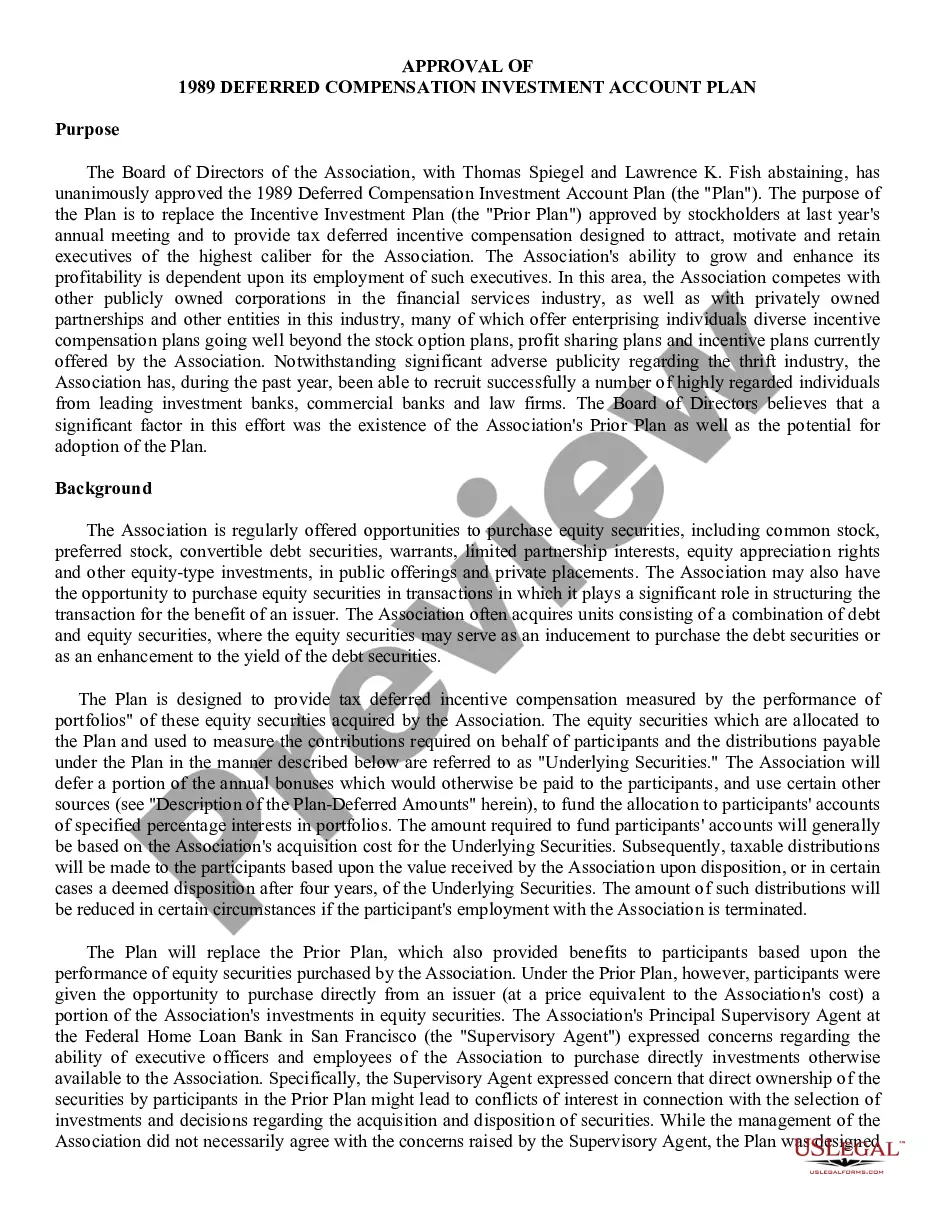

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

California Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

Finding the right legal file format might be a struggle. Of course, there are plenty of themes accessible on the Internet, but how can you obtain the legal kind you need? Utilize the US Legal Forms site. The assistance delivers a huge number of themes, such as the California Deferred Compensation Investment Account Plan, that you can use for organization and personal requirements. Each of the forms are inspected by specialists and fulfill federal and state needs.

If you are currently registered, log in to your bank account and click on the Acquire option to get the California Deferred Compensation Investment Account Plan. Make use of bank account to appear throughout the legal forms you have acquired earlier. Proceed to the My Forms tab of your bank account and acquire another backup from the file you need.

If you are a whole new consumer of US Legal Forms, here are simple recommendations that you should stick to:

- First, make certain you have chosen the proper kind for your personal town/area. You can look through the form making use of the Review option and read the form description to guarantee it is the best for you.

- In the event the kind is not going to fulfill your preferences, make use of the Seach discipline to get the right kind.

- Once you are positive that the form is proper, go through the Get now option to get the kind.

- Pick the costs program you want and type in the essential details. Design your bank account and pay money for an order using your PayPal bank account or credit card.

- Select the document formatting and down load the legal file format to your gadget.

- Complete, change and print and signal the attained California Deferred Compensation Investment Account Plan.

US Legal Forms may be the largest local library of legal forms in which you can discover various file themes. Utilize the service to down load skillfully-produced papers that stick to express needs.

Form popularity

FAQ

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, 401(k) retirement plans, and employee stock options.

Key Differences Deferred compensation plans tend to offer better investment options than most 401(k) plans, but are at a disadvantage regarding liquidity. Typically, deferred compensation funds cannot be accessed, for any reason, before the specified distribution date.

Employer Contributions. 457(b)s only allow $22,500 in contributions from any source in 2023 ($23,000 in 2024), whereas 403(b)s allows total contributions of $66,000, including $22,500 from an employee.

A 457(b) plan's annual contributions and other additions (excluding earnings) to a participant's account cannot exceed the lesser of: 100% of the participant's includible compensation, or. the elective deferral limit ($22,500 in 2023; $20,500 in 2022; $19,500 in 2020 and in 2021).

The Bottom Line. If you have a qualified plan and have passed the vesting period, your deferred compensation is yours, even if you quit with no notice on very bad terms. If you have a non-qualified plan, you may have to forfeit all of your deferred compensation by quitting depending on your plan's specific terms.

When you defer receiving income, you also defer paying federal and state taxes on that income until it's paid out to you. This can be especially appealing if you're currently in a high tax bracket and expect to be in a lower tax bracket in the future.

Deferring income to retirement might help avoid high state income taxes (ex: California, New York, etc) if you're planning to move to a low-tax state. The biggest risk of deferred compensation plans is they're not guaranteed; if your company goes bankrupt, you might receive none of the income you deferred.

A 401(k) has an edge when it comes to regular contributions, since employer matches don't count against your annual contribution limit. But if you have a 457 plan, you could benefit from the special catch-up contribution provision which you don't get with a 401(k).