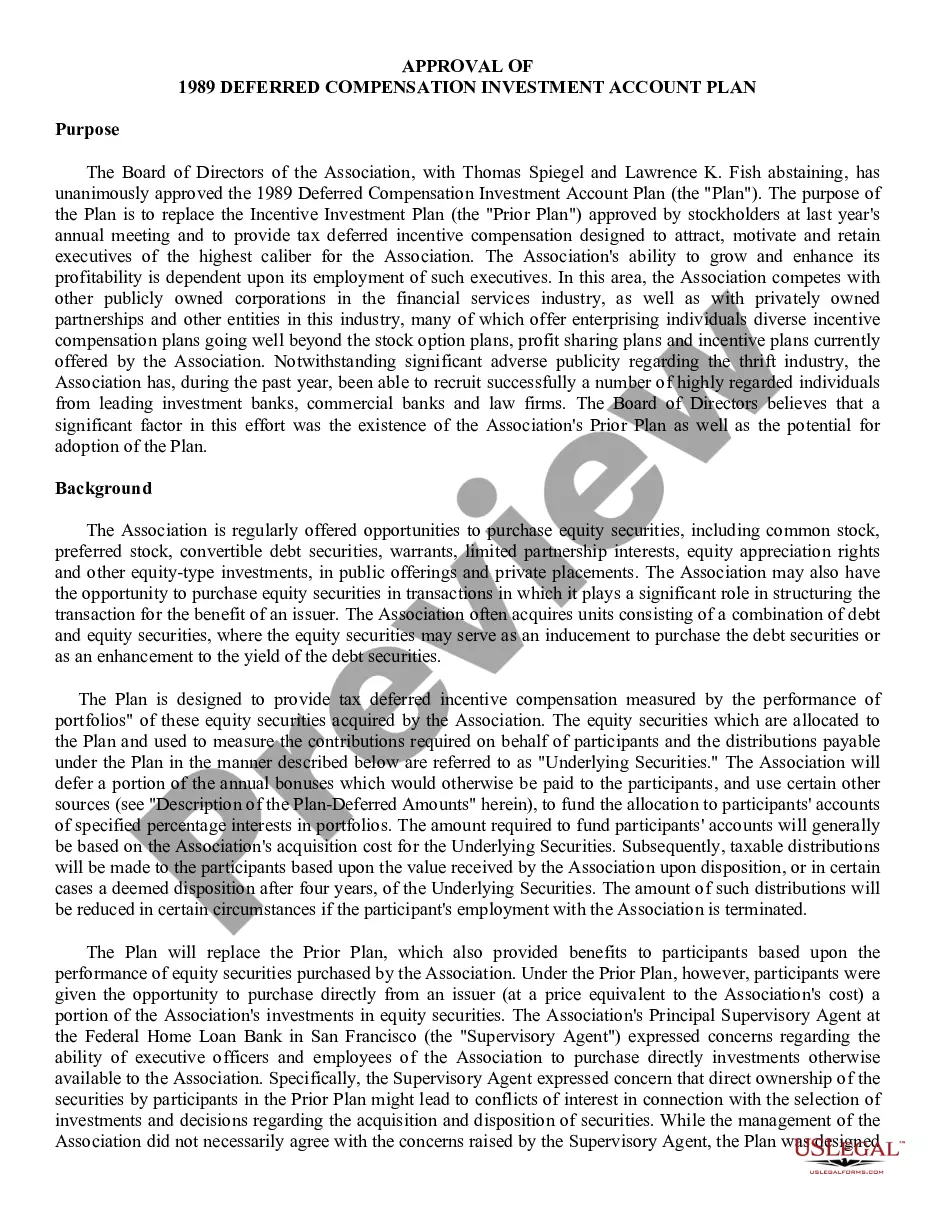

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Arizona Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

If you wish to complete, down load, or print legal file themes, use US Legal Forms, the greatest collection of legal types, that can be found on the web. Use the site`s easy and hassle-free lookup to find the files you want. A variety of themes for company and personal reasons are categorized by groups and claims, or search phrases. Use US Legal Forms to find the Arizona Deferred Compensation Investment Account Plan in a number of clicks.

Should you be already a US Legal Forms customer, log in in your profile and then click the Down load switch to get the Arizona Deferred Compensation Investment Account Plan. You can even access types you earlier acquired from the My Forms tab of your own profile.

If you use US Legal Forms the very first time, follow the instructions beneath:

- Step 1. Be sure you have selected the form for the proper area/land.

- Step 2. Utilize the Preview choice to look through the form`s articles. Don`t overlook to see the explanation.

- Step 3. Should you be unhappy together with the type, take advantage of the Search discipline on top of the monitor to locate other versions from the legal type web template.

- Step 4. Once you have found the form you want, go through the Buy now switch. Pick the prices strategy you prefer and add your qualifications to sign up for an profile.

- Step 5. Approach the transaction. You may use your bank card or PayPal profile to accomplish the transaction.

- Step 6. Find the structure from the legal type and down load it in your gadget.

- Step 7. Comprehensive, modify and print or sign the Arizona Deferred Compensation Investment Account Plan.

Each legal file web template you get is your own property eternally. You might have acces to every single type you acquired within your acccount. Click on the My Forms section and choose a type to print or down load yet again.

Remain competitive and down load, and print the Arizona Deferred Compensation Investment Account Plan with US Legal Forms. There are thousands of expert and status-specific types you can use for your personal company or personal requirements.

Form popularity

FAQ

You can request a loan by logging in to your DCP account, completing a Loan Application Form, or calling the Service Center at 844-523-2457.

Deferring income to retirement might help avoid high state income taxes (ex: California, New York, etc) if you're planning to move to a low-tax state. The biggest risk of deferred compensation plans is they're not guaranteed; if your company goes bankrupt, you might receive none of the income you deferred.

There are primarily two different plans available to ASRS members who work for employers that are not a state agency or state university: a 457(b) Plan, and a 403(b) plan.

457(b) vs 403(b) On the whole, 457(b) plans have a lot in common with 403(b) plans. They are both employer-sponsored retirement savings accounts, they have the same standard contribution limits, and they use similar types of investment accounts to grow funds for retirement.

The 457 plan is a retirement savings plan and you generally cannot withdraw money while you are still employed. When you leave employment, you may withdraw funds; leave them in place; transfer them to a 457, 403(b) or 401(k) of a new employer; or roll them into an Individual Retirement Account (IRA).

You can take out small or large sums anytime, or you can set up automatic, periodic payments. If your plan allows it, you may be able to have direct deposit which allows for fast transfer of funds. Unlike a check, direct deposit typically doesn't include a hold on the funds from your account.

You can take penalty-free withdrawals from your 457 account at any age after you leave your job. Most other types of retirement-savings plans assess a 10% penalty if you withdraw money before age 55 or 59½, depending on when you leave your job.

457(b) Assets can be withdrawn without penalty at any age upon separation from service from the plan sponsor, or age 70½ if still working.