Alabama Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Retail Charge Account Agreement Initial Disclosure Statement?

Discovering the right legitimate file design could be a struggle. Needless to say, there are plenty of layouts available on the net, but how would you discover the legitimate develop you need? Utilize the US Legal Forms web site. The assistance delivers 1000s of layouts, for example the Alabama Retail Charge Account Agreement Initial Disclosure Statement, that you can use for enterprise and private demands. All of the varieties are examined by experts and meet up with state and federal demands.

When you are already signed up, log in for your account and then click the Acquire option to have the Alabama Retail Charge Account Agreement Initial Disclosure Statement. Utilize your account to appear throughout the legitimate varieties you have acquired in the past. Proceed to the My Forms tab of your own account and have an additional backup in the file you need.

When you are a whole new customer of US Legal Forms, allow me to share basic guidelines so that you can adhere to:

- Initial, make sure you have selected the appropriate develop to your town/region. You can look through the shape making use of the Preview option and browse the shape explanation to guarantee it will be the best for you.

- In the event the develop will not meet up with your expectations, utilize the Seach industry to get the right develop.

- Once you are sure that the shape is proper, click the Acquire now option to have the develop.

- Choose the prices strategy you desire and enter the needed information. Make your account and pay for the order with your PayPal account or Visa or Mastercard.

- Opt for the data file structure and obtain the legitimate file design for your system.

- Total, edit and printing and indication the attained Alabama Retail Charge Account Agreement Initial Disclosure Statement.

US Legal Forms will be the biggest catalogue of legitimate varieties where you can see numerous file layouts. Utilize the company to obtain expertly-produced paperwork that adhere to condition demands.

Form popularity

FAQ

The Truth in Lending Act (TILA) helps protect consumers from unfair credit practices by requiring creditors and lenders to pre-disclose to borrowers certain terms, limitations, and provisions?such as the APR, duration of the loan, and the total costs?of a credit agreement or loan.

Created to protect people from predatory lending practices, Regulation Z, also known as the Truth in Lending Act, requires that lenders disclose borrowing costs, interest rates and fees upfront and in clear language so consumers can understand all the terms and make informed decisions.

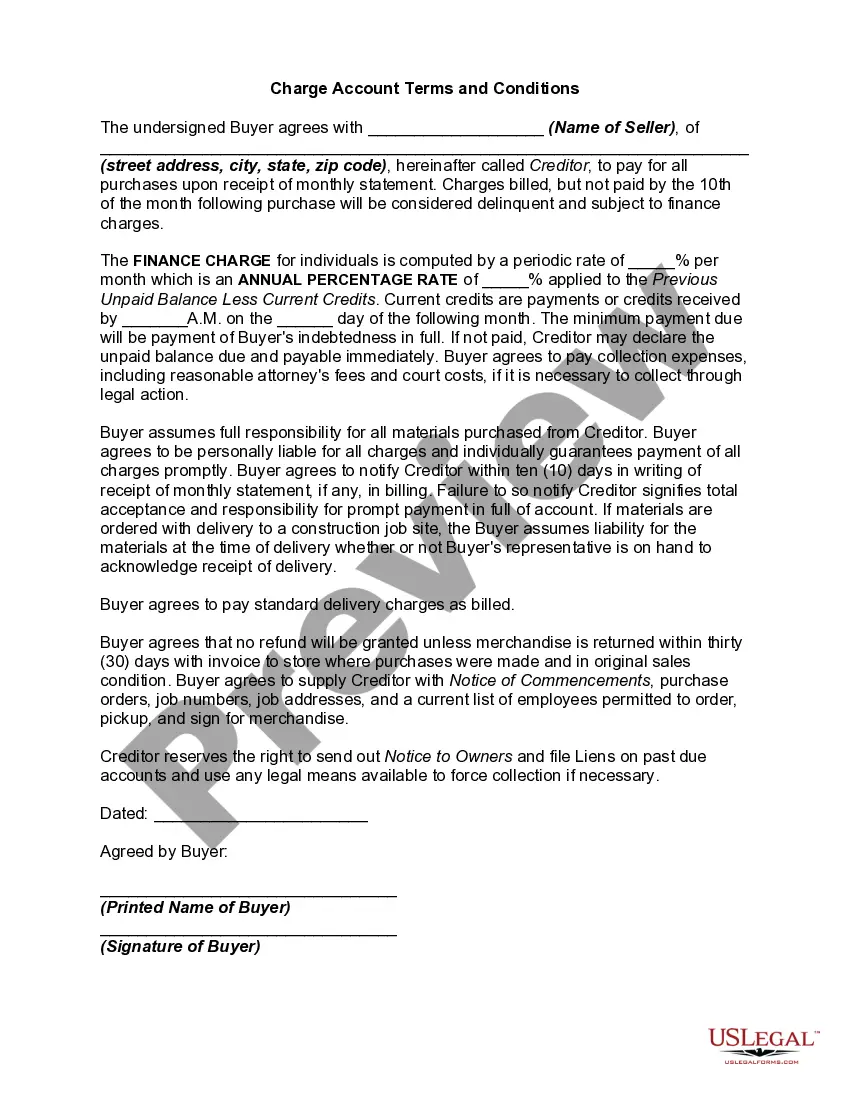

Creditors must name the balance computation method used for each feature of the account and state that an explanation of the balance computation method(s) is provided in the account-opening disclosures. v. Creditors must state that consumers' billing rights are provided in the account-opening disclosures.

What Is Disclosure? Federal regulations require the disclosure of all relevant financial information by publicly-listed companies. In addition to financial data, companies are required to reveal their analysis of their strengths, weaknesses, opportunities, and threats.

TILA disclosures include the number of payments, the monthly payment, late fees, whether a borrower can prepay the loan without penalty and other important terms. TILA disclosures is often provided as part of the loan contract, so the borrower may be given the entire contract for review when the TILA is requested.

Credit card disclosure must include a list of fees associated with your card. Some common credit card fees include annual fees, cash advance fees, foreign transaction fees, often called a "currency conversion" fee. Other fees include late payment fees, over-the-limit fees, and returned payment fees.

Total of payments, Payment schedule, Prepayment/late payment penalties, If applicable to the transaction: (1) Total sales cost, (2) Demand feature, (3) Security interest, (4) Insurance, (5) Required deposit, and (6) Reference to contract.

The CARD Act became part of the Truth in Lending Act, and it compels credit card issuers to disclose all rates, limit fees and limit the cardholder's liability for fraudulent transactions, among other protections.