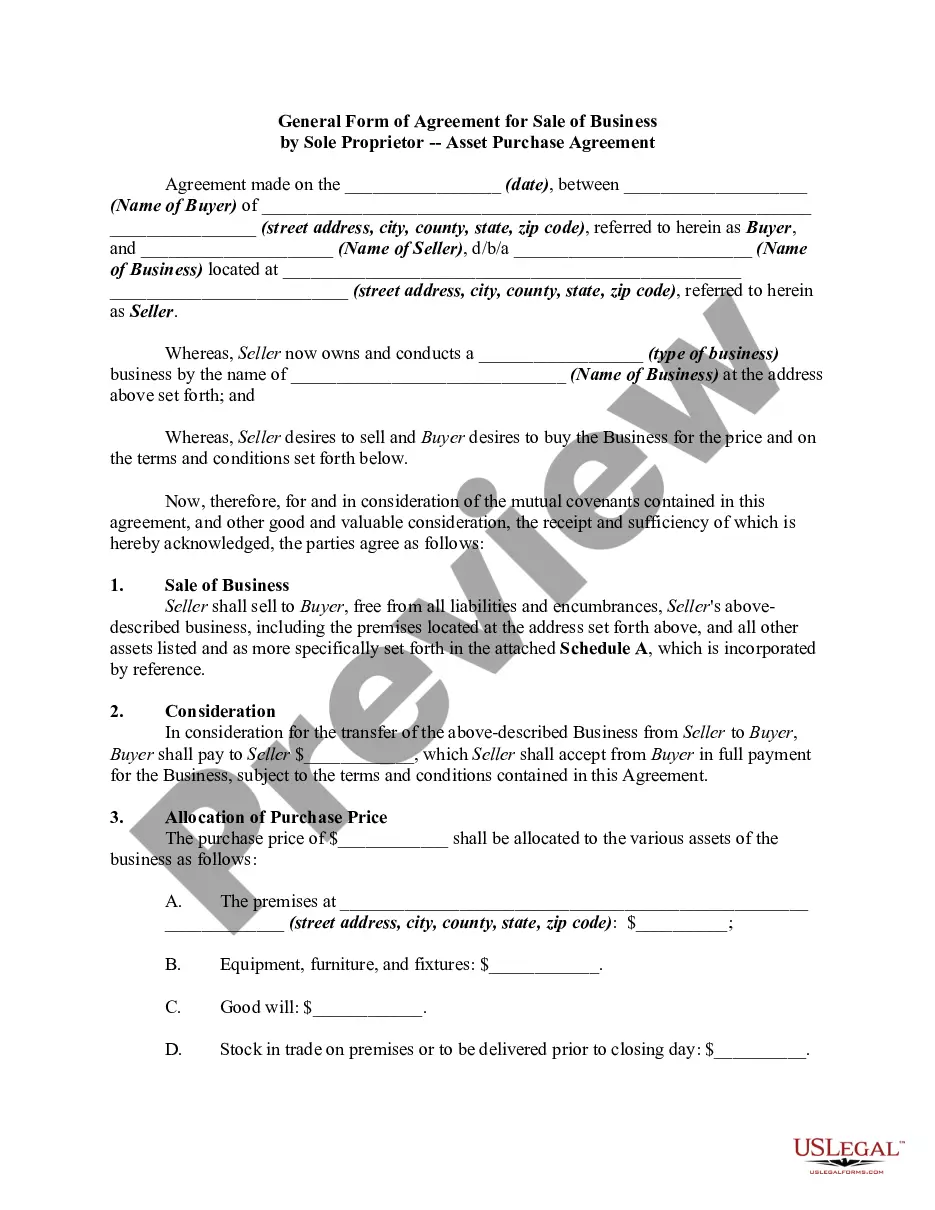

This form is an Asset Purchase Agreement. The buyer agrees to purchase from the seller certain assets which are listed in the agreement. The form also provides a listing of certain assets which will be excluded from the sale. The form must be signed in the presence of a notary public.

Alabama Asset Purchase Agreement - Business Sale

Category:

State:

Multi-State

Control #:

US-00418

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Asset Purchase Agreement - Business Sale?

Are you currently in a circumstance where you need documents for both business or personal purposes almost every day? There are numerous legal document templates available online, but finding reliable ones is not simple. US Legal Forms provides a vast array of template options, including the Alabama Asset Purchase Agreement - Business Sale, designed to meet federal and state requirements.

If you are already familiar with the US Legal Forms site and have an account, simply Log In. Then, you can download the Alabama Asset Purchase Agreement - Business Sale template.

If you do not have an account and wish to start using US Legal Forms, follow these steps.

Access all the document templates you have purchased in the My documents menu. You can download an additional copy of the Alabama Asset Purchase Agreement - Business Sale whenever needed. Simply select the desired document to download or print the template.

Use US Legal Forms, the most extensive collection of legal templates, to save time and avoid mistakes. The service provides professionally crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- Obtain the document you need and ensure it is for the correct state/region.

- Utilize the Review option to examine the document.

- Read the details to ensure you have chosen the right document.

- If the document isn't what you are looking for, use the Search field to find the document that suits your needs and requirements.

- Once you find the right document, click Get now.

- Select the pricing plan you prefer, complete the required information to create your account, and pay for your order using your PayPal or credit card.

- Choose a suitable file format and download your copy.

Form popularity

FAQ

The result reflects whether your company made a profit or took a loss on the sale of the property.Step 1: Debit the Cash Account.Step 2: Debit the Accumulated Depreciation Account.Step 3: Credit the Property's Asset Account.Step 4: Determine the Property's Book Value.Step 5: Credit or Debit the Disposal Account.

Sale of Business AssetsReport the sale of your business assets on Form 8594 and Form 4797, and attach these forms to your final tax return. Form 8594 is the Asset Acquisition Statement, which the buyer and seller must complete and submit to the IRS.

In an asset purchase, the buyer will only buy certain assets of the seller's company. The seller will continue to own the assets that were not included in the purchase agreement with the buyer. The transfer of ownership of certain assets may need to be confirmed with filings, such as titles to transfer real estate.

An asset purchase agreement is an agreement between a buyer and a seller to purchase property, like business assets or real property, either on their own or as part of a merger-acquisition.

An asset purchase involves the purchase of the selling company's assets -- including facilities, vehicles, equipment, and stock or inventory. A stock purchase involves the purchase of the selling company's stock only.

An asset sale involves the purchase of some or all of the assets owned by a company. Examples of common assets which are sold include; plant and equipment, land, buildings, machinery, stock, goodwill, contracts, records and intellectual property (including domain names and trademarks).

In an asset sale, you retain the legal entity of the business and only sell the business' assets. For example, say you run a rental car company owned by Harry Smith Pty Ltd. You decide that you need to sell 50% of your fleet to upgrade your vehicles and want to sell those vehicles in one transaction to one buyer.

In an asset sale, a firm sells some or all of its actual assets, either tangible or intangible. The seller retains legal ownership of the company that has sold the assets but has no further recourse to the sold assets. The buyer assumes no liabilities in an asset sale.

The bill of sale is typically delivered as an ancillary document in an asset purchase to transfer title to tangible personal property. It does not cover intangible property (such as intellectual property rights or contract rights) or real property.

Your company will also still exist after an asset sale, and administratively you will still need to take steps to dissolve the company and deal with any remaining liabilities and assets. Unlike a stock sale, 100% of the interests of a company can usually be transferred without the consent of all of the stockholders.