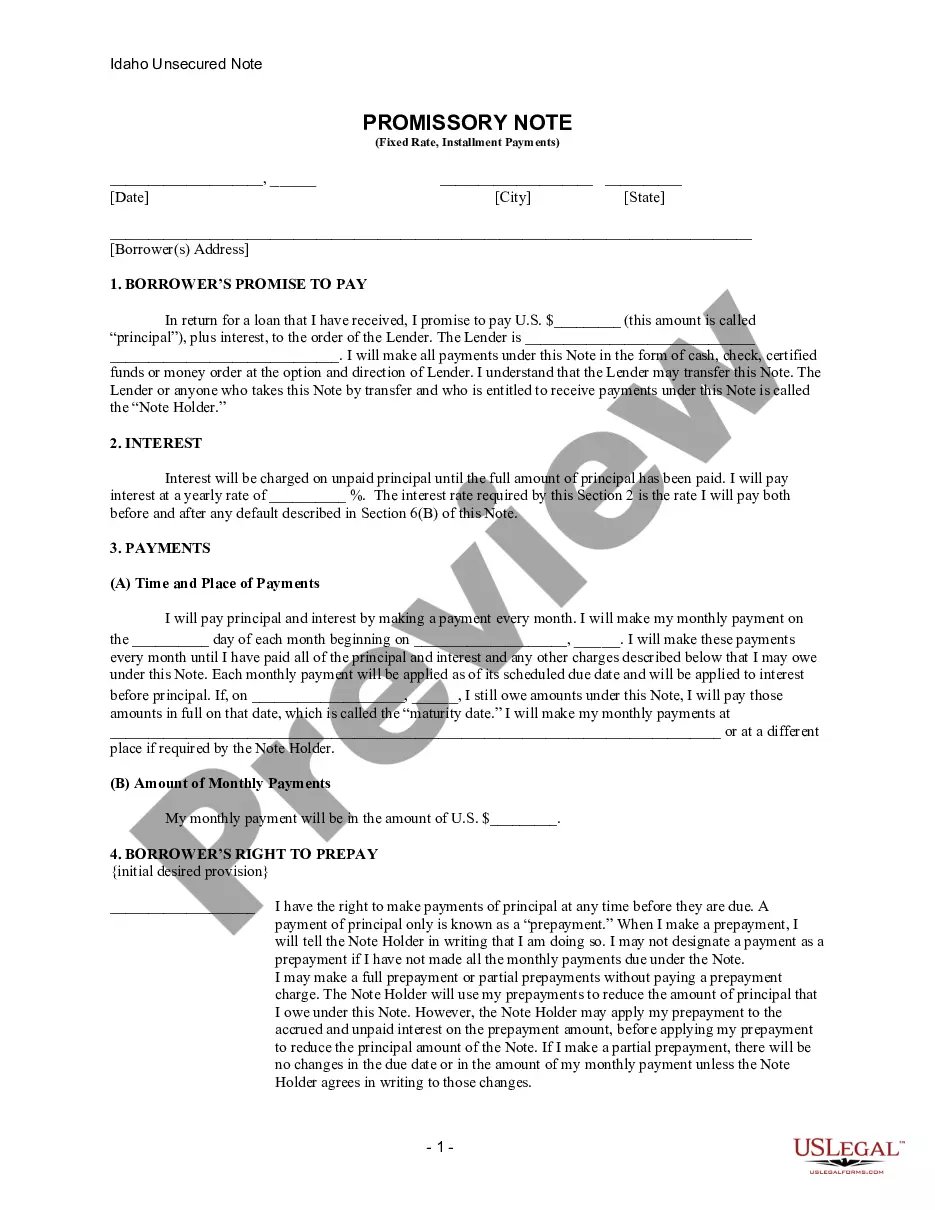

Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property

What is this form?

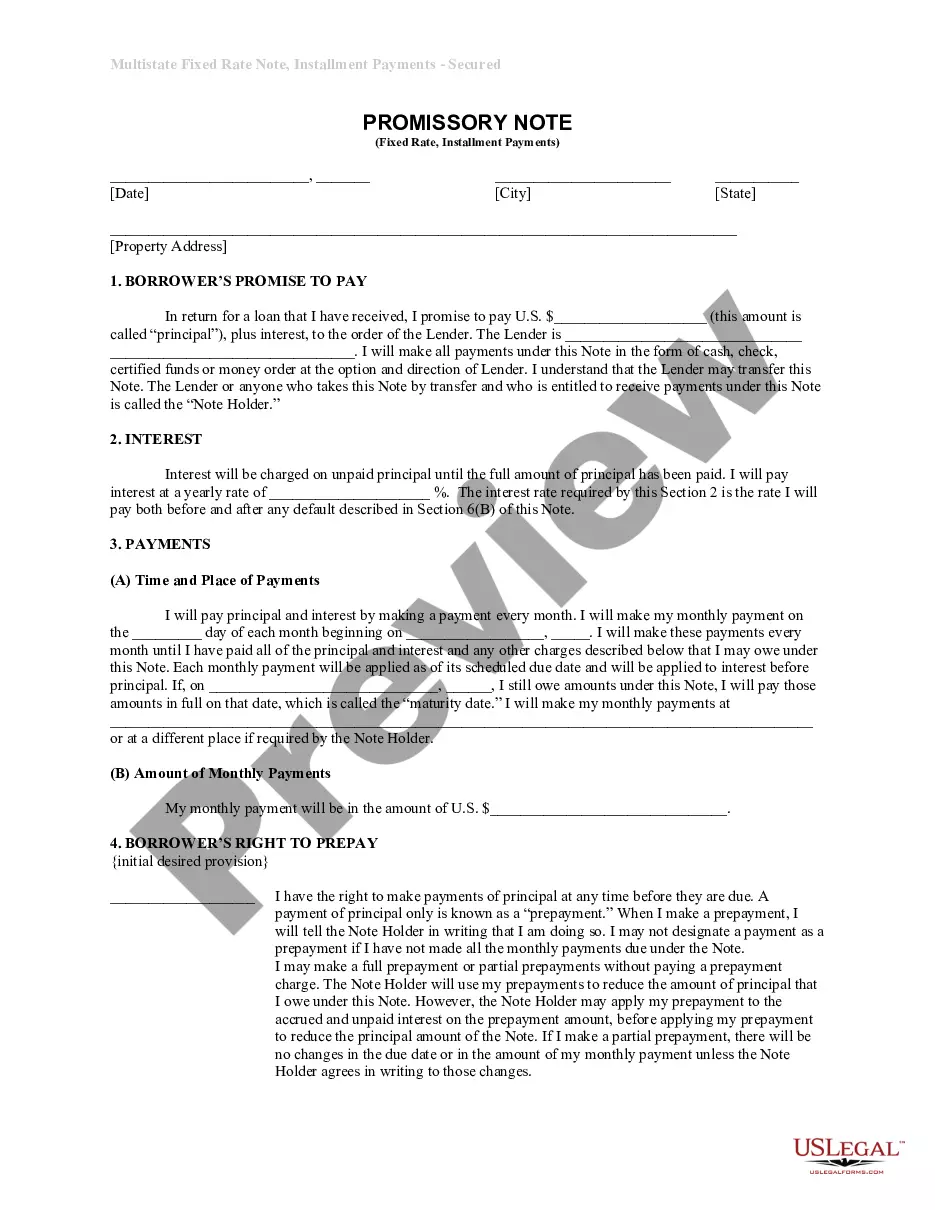

The Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document that outlines the terms of a loan where personal property serves as collateral. This form serves as a formal agreement between a borrower and lender, detailing repayment terms, interest rates, and the responsibilities of both parties. Unlike unsecured promissory notes, this form provides additional security to the lender through a lien on specified personal property.

Main sections of this form

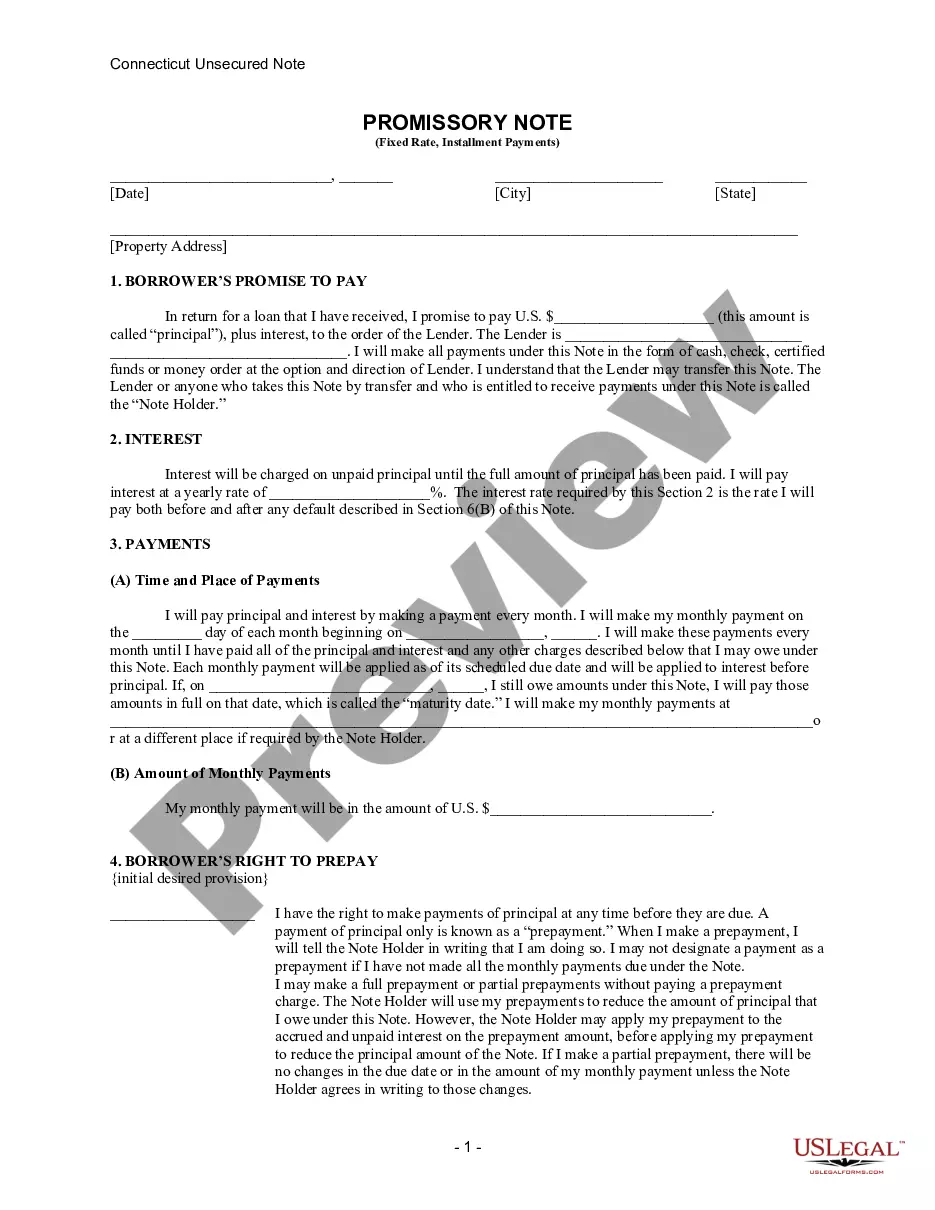

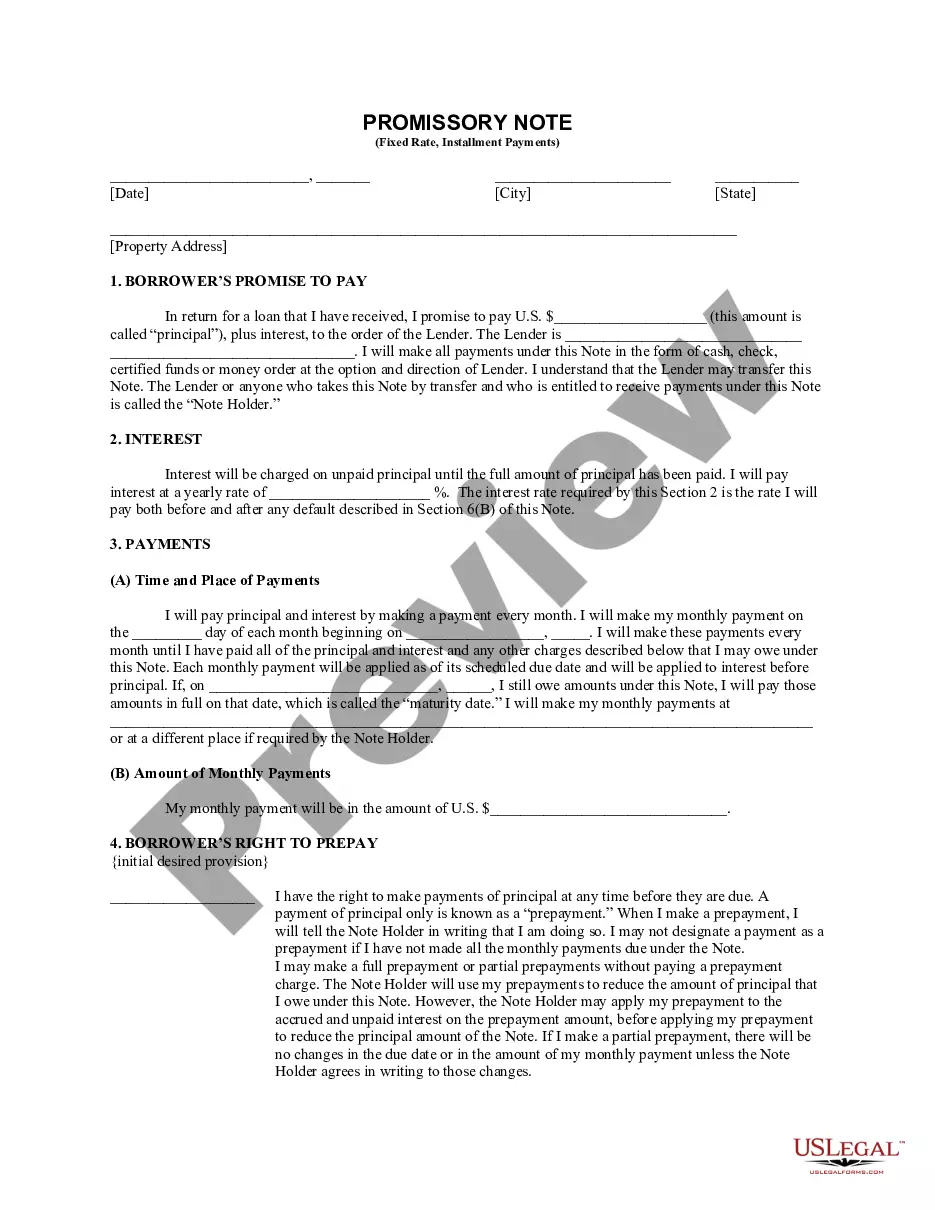

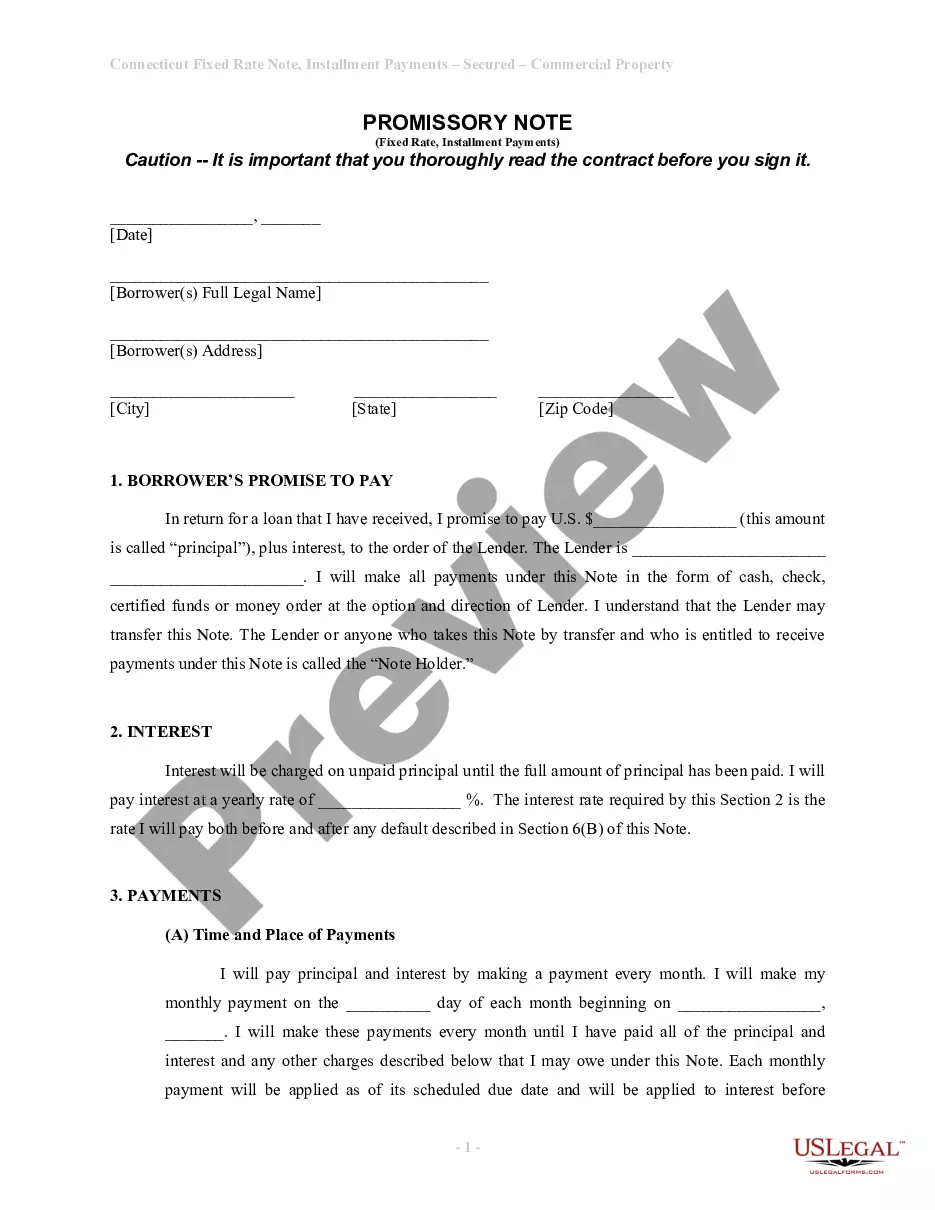

- Borrower's promise to pay the principal amount plus interest to the lender.

- Clear terms regarding interest rates and payment schedules.

- Provisions for late charges and default notifications.

- Details on the borrower's right to make early prepayments.

- Information on secured property and the requirements for enforcement.

Situations where this form applies

This form is necessary when a borrower intends to take out a loan secured by personal property. It is applicable in situations where the borrower wants to formalize their repayment obligation and the lender requires assurance of payment in the form of collateral. This form is suitable for loans in various scenarios, such as purchasing furniture, electronics, or vehicles, where the item can serve as collateral in the event of default.

Who needs this form

- Borrowers seeking to secure a loan with personal property

- Lenders who require collateral to mitigate financial risk

- Individuals or businesses entering into loan agreements in Connecticut

- Parties who wish to outline clear payment and interest terms

How to prepare this document

- Identify the parties involved: Enter the names and addresses of both the borrower and lender.

- Specify loan details: Fill in the principal amount, interest rate, and payment frequency.

- Enter payment terms: Include the start date of payments and the proposed maturity date.

- Describe secured property: Clearly describe the assets that will serve as collateral.

- Collect signatures: Ensure that both parties sign and date the form to validate the agreement.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it is recommended to check with a legal professional to ensure compliance with any specific legal requirements pertaining to your situation.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to clearly define the secured property.

- Ignoring the specific interest rate limitations mandated by Connecticut law.

- Omitting crucial details such as payment due dates and late fees.

- Not obtaining signatures from both parties prior to execution.

Why use this form online

- Convenient access to legally vetted forms that can be downloaded and printed.

- Editability to customize terms and conditions that suit the specific agreement.

- Reliable templates that meet state requirements, reducing legal risks.

Legal use & context

- This form creates a legally binding obligation for the borrower to repay the loan.

- It provides legal security for the lender through the collateral described.

- Users should ensure compliance with state laws governing secured loans.

Key takeaways

- The promissory note formalizes the loan agreement with personal property as collateral.

- It outlines essential terms including repayment schedule, interest rates, and default consequences.

- Completion of the form requires careful attention to detail to avoid common errors.

- This form is specifically designed for users in Connecticut.

Looking for another form?

Form popularity

FAQ

A security agreement serves as a document where personal property is used as security for a promissory note. In this context, the Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property details both the borrower's obligations and the lender's rights. By outlining specific personal property as collateral, this agreement provides clarity and security for both parties involved in the transaction.

Yes, a promissory note can be secured by real property, but that typically involves real estate rather than personal property. For Connecticut Installments Fixed Rate Promissory Notes Secured by Personal Property, the focus is usually on tangible assets like vehicles or equipment. However, using real property as collateral offers different benefits and obligations, and understanding these differences is crucial for anyone entering such an agreement.

The document that creates a lien and acts as security for a promissory note is typically a security agreement. This agreement outlines the borrowing terms and specifies how a Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property is backed by the borrower’s assets. By signing this document, the borrower allows the lender to claim the specified personal property in case of default. It's essential to have this agreement properly drafted to protect both parties.

Yes, a well-drafted promissory note can hold up in court, especially if it follows state-specific guidelines. The Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property provides a clear structure that supports its validity. When disputes arise, courts often rely on the documentation of the note to enforce the obligations outlined in it.

Yes, promissory notes are generally enforceable in court when they meet certain legal requirements. A Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property is particularly strong because it outlines payment terms and collateral clearly. However, the enforceability may depend on factors such as proper signatures and the note's adherence to state laws.

Typically, a promissory note does not need to be filed with any government agency; however, it's advisable to keep it in a safe location. If your note is secured by real property, you should file the related mortgage or deed of trust with the local county recorder’s office. This filing protects your interest and makes the promissory note enforceable against third parties. For specifics, consider consulting the resources available through US Legal Forms.

To secure a promissory note with real property, the borrower must designate the real estate as collateral. This often involves drafting a mortgage or deed of trust that outlines the terms. The Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property will clearly state the property involved. If you need assistance, platforms like US Legal Forms offer templates to help you navigate this process easily.

Yes, promissory notes are generally legally enforceable as long as they meet specific requirements. For a Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property to be valid, it must clearly outline the terms agreed upon by both parties. Courts recognize these notes as valid contracts, provided they comply with state laws. This enforceability makes promissory notes, when completed correctly, a reliable method for securing loans and obligations.

An installment note and a promissory note are closely related, but they are not identical. An installment note, including the Connecticut Installments Fixed Rate Promissory Note Secured by Personal Property, specifies a payment schedule, often involving regular payments over time. In contrast, a promissory note can be a broader term that may not require structured payments. Understanding this distinction can help you choose the right financial instrument for your needs.