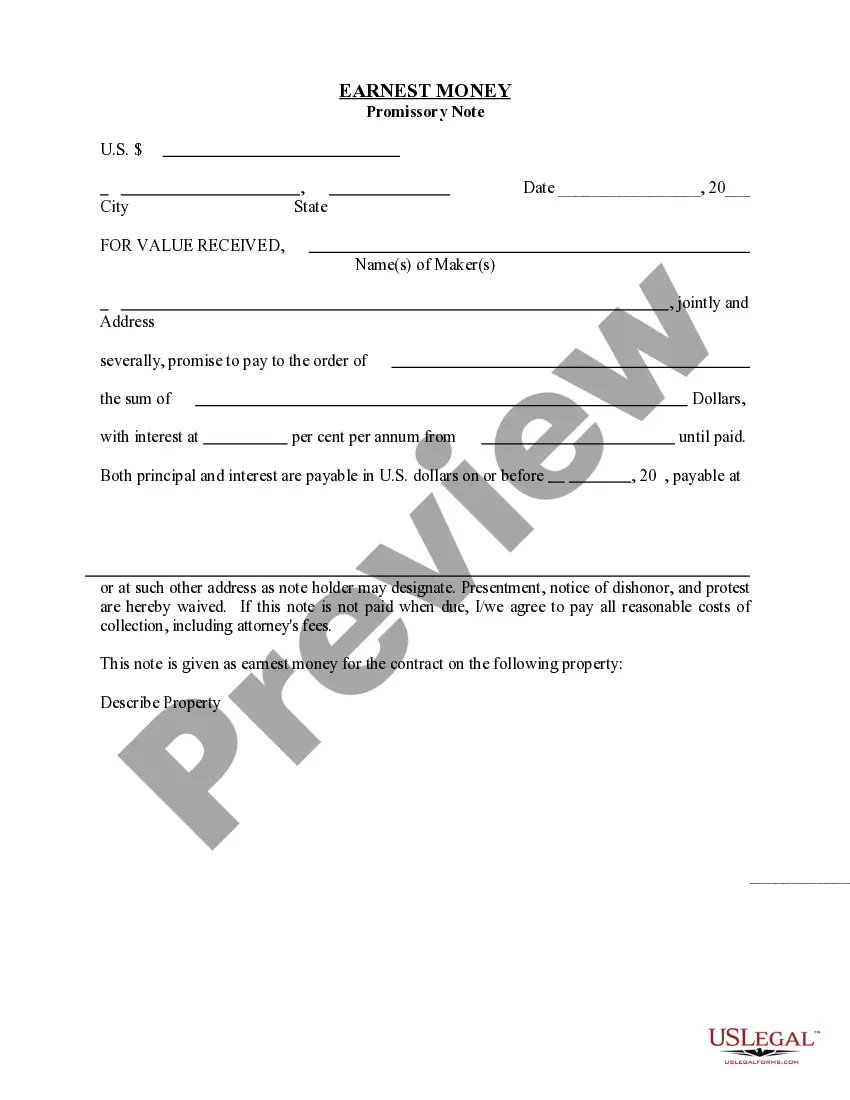

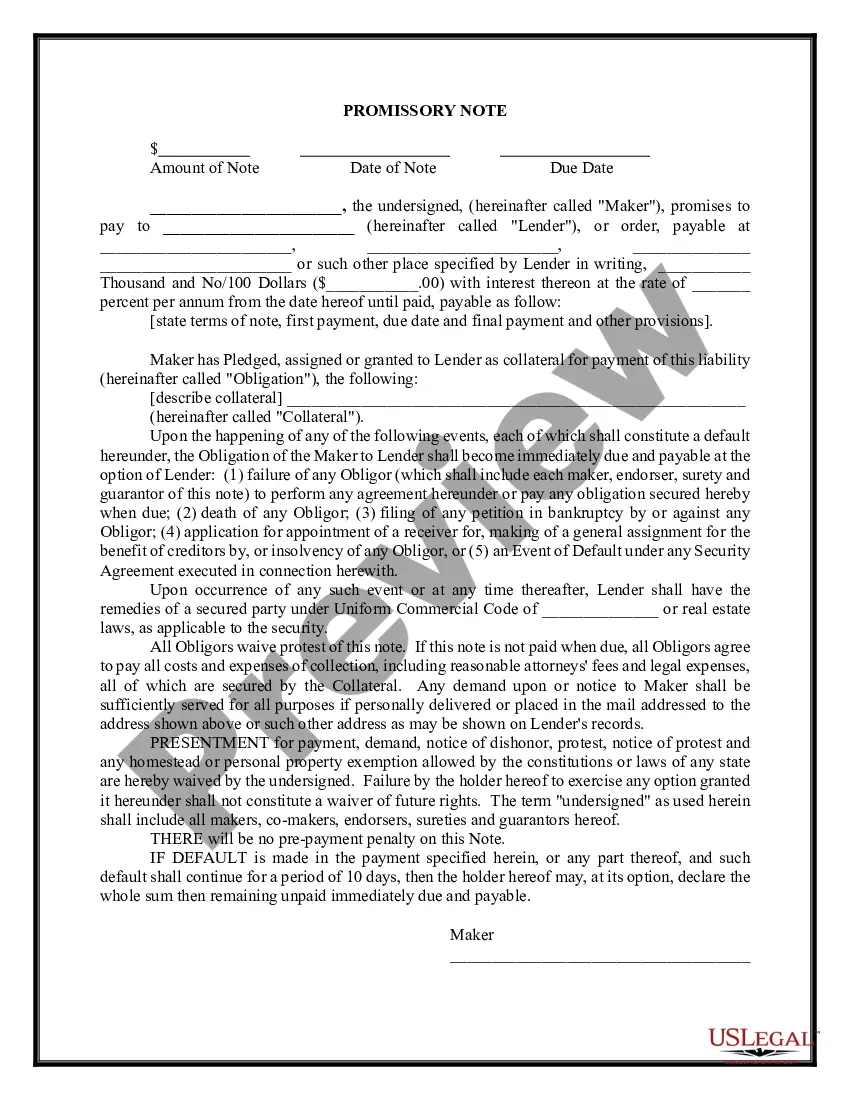

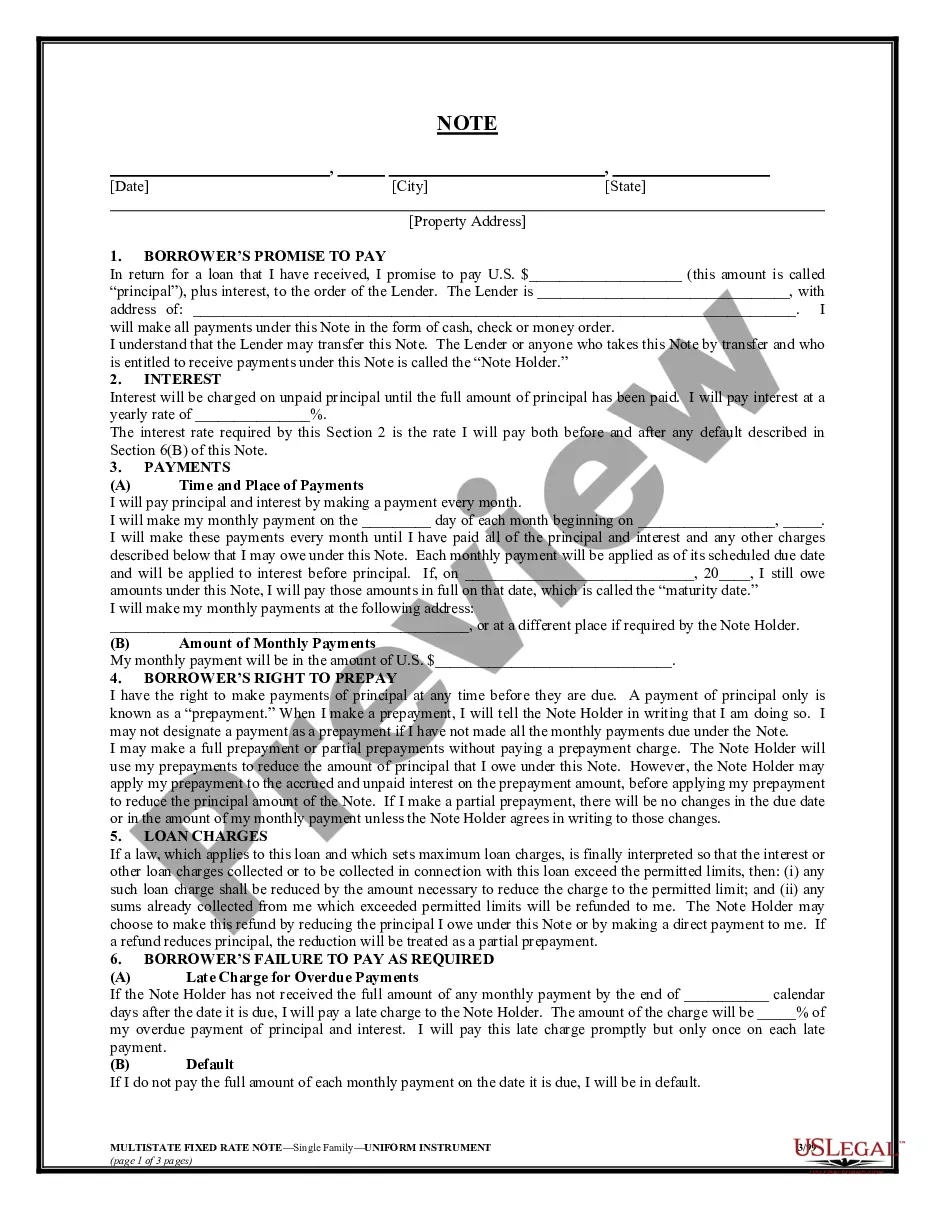

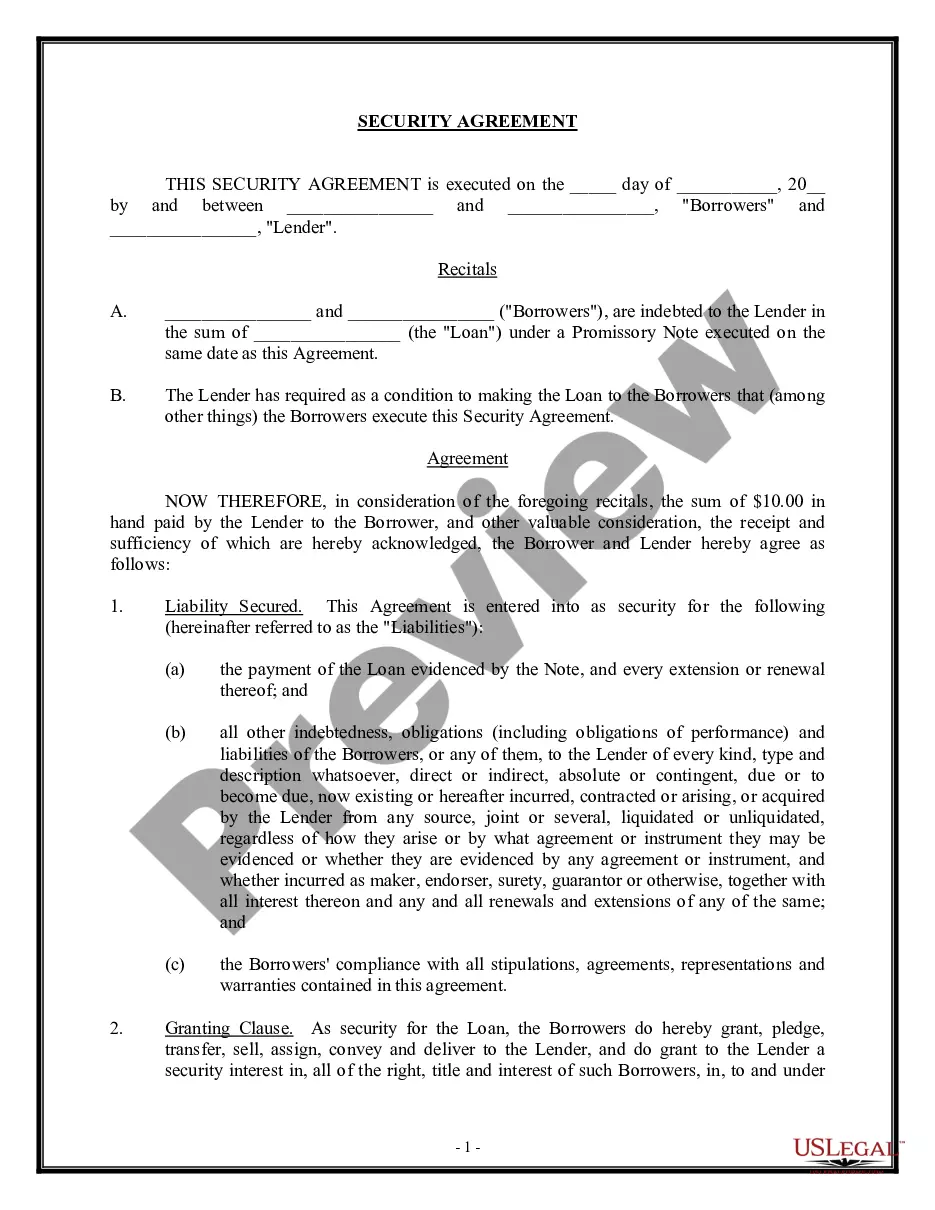

Mortgage Notes Example Within 1 Year

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Wisconsin Promissory Note Secure By A Mortgage?

The Mortgage Notes Sample Within 1 Year that you view on this site is a versatile legal template created by skilled attorneys in compliance with national and state laws.

For over 25 years, US Legal Forms has offered individuals, enterprises, and legal experts more than 85,000 authenticated, state-specific templates for various business and personal situations. It is the fastest, simplest, and most trustworthy method to acquire the documents you require, as the service ensures the highest level of data protection and anti-malware defense.

Select the format you desire for your Mortgage Notes Sample Within 1 Year (PDF, DOCX, RTF) and download the template to your device.

- Search for the document you are looking for and review it.

- Browse the template you found and preview it or examine the form description to confirm it meets your needs. If it doesn't, utilize the search function to find the correct one. Click Buy Now once you have found the template you require.

- Subscribe and Log In.

- Select the pricing option that works for you and set up an account. Use PayPal or a credit card for a swift payment. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the editable template.

Form popularity

FAQ

Product liability is a doctrine that gives plaintiffs a cause of action if they encounter a defective consumer item. This doctrine can fall under negligence, but it is generally associated with strict liability, meaning that defendants can be held liable regardless of their intent or knowledge.

In order to succeed on a claim for strict product liability, a plaintiff must show that: (1) the product was defective (2) when it left the defendant's hand, and that (3) the defect caused the plaintiff's injury.

There are three types of product defects that incur liability in manufacturers and suppliers: Design Defects. Design defects are inherent, as they exist before the product is manufactured. ... Manufacturing Defects. Manufacturing defects occur during the construction or production of the item. ... Defects in marketing.

So, for example, if your vehicle veered off the roadway because of a faulty steering, you would have a product liability claim only if you can show evidence that your accident and resulting injuries were caused by the steering defect, not because of a mistake you made.

In a product liability claim, a person claiming breach of this duty (the plaintiff) must prove on the balance of probabilities that 1) a defect in the defendant's product or the defendant's failure to provide instructions or to warn of foreseeable harm caused injury to that person; and 2) that defect or failure to ...

What Do You Need to Prove in a Strict Product Liability Claim? The product was unreasonably unsafe at the time it was sold. The seller expected that consumers would use the product without any further modifications. The product was used as intended.

The Key Elements Of A Product Liability Claim The Product Caused Your Injury. The first element of a product defect claim is that the product is linked to your injury. ... The Product Is Defective. ... The Product Defect Resulted In Your Injury. ... You Used The Product As Intended. ... Get In Touch With Our Experienced Legal Team.

Product liability law includes automobiles, workplace machinery, and more. Under Virginia law, a product must be reasonably safe for its intended purposes and for its reasonably foreseeable uses. However, products are not required to be designed or produced with features representing the ultimate in safety.