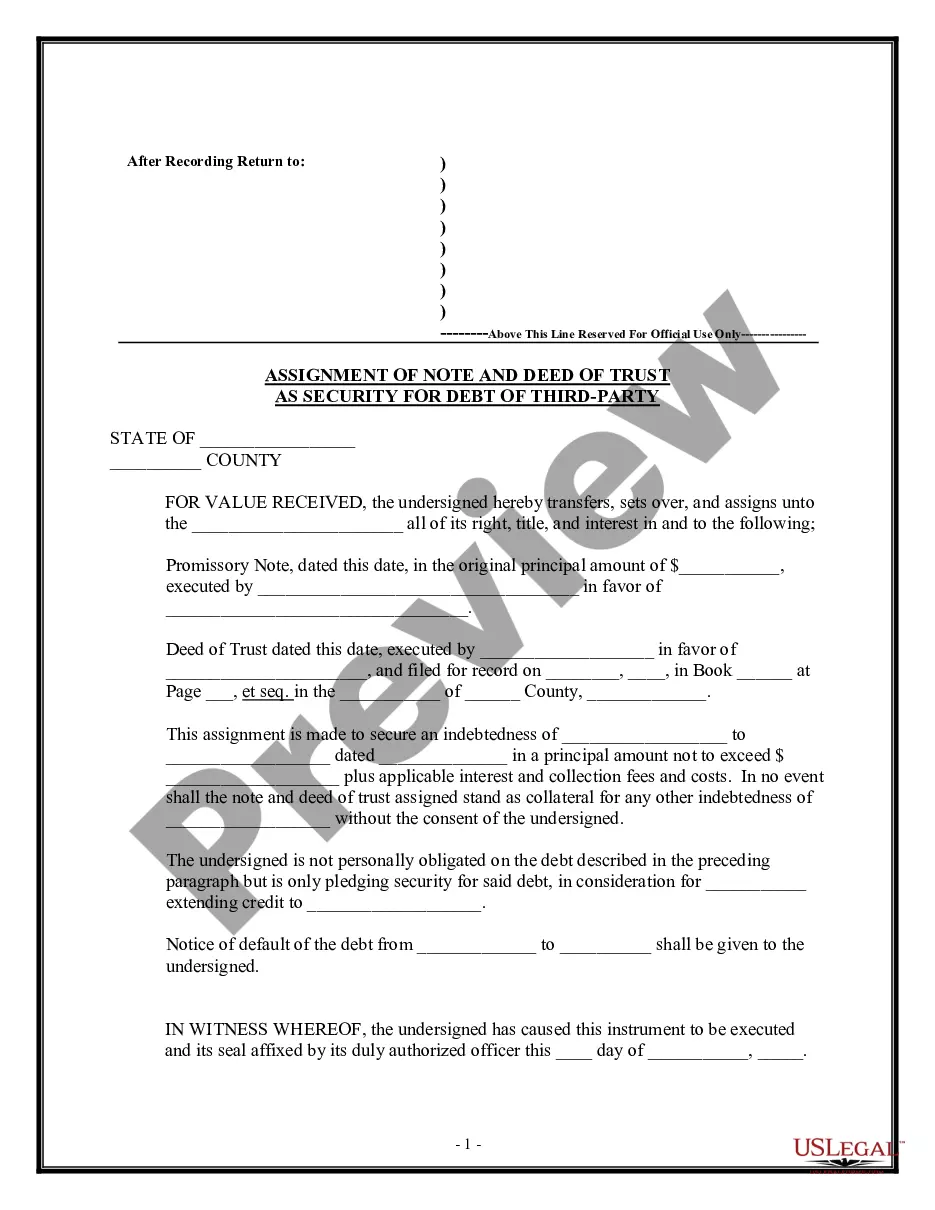

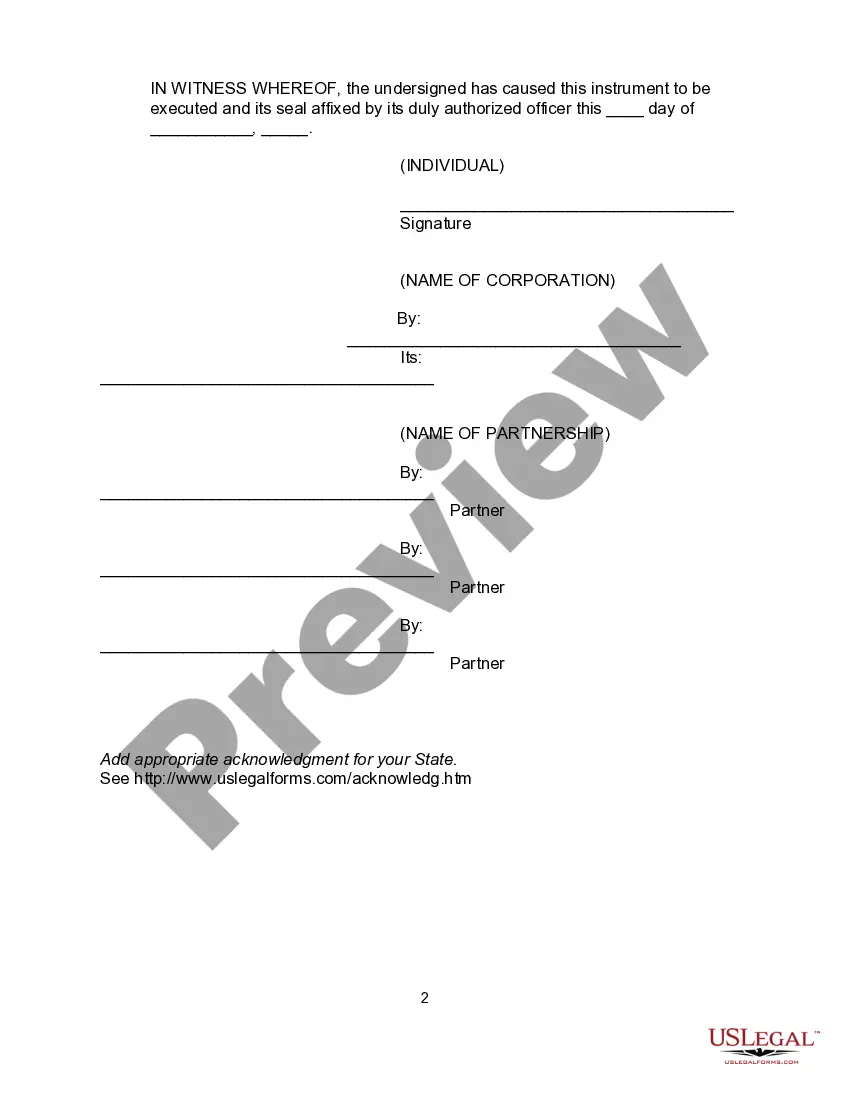

Assignment Of Debt Form For Taxes

Description

How to fill out Assignment Of Debt Form For Taxes?

There's no longer a need to squander hours searching for legal documents to adhere to your local state laws.

US Legal Forms has consolidated all of them in one location and optimized their accessibility.

Our site offers over 85,000 templates for various business and personal legal situations categorized by state and usage area.

Use the search field above to look for another sample if the current one does not meet your needs.

- All forms are expertly crafted and verified for authenticity, so you can be confident in acquiring an up-to-date Assignment Of Debt Form For Taxes.

- If you are acquainted with our platform and already possess an account, ensure your subscription is active before accessing any templates.

- Log In to your account, select the document, and click Download.

- You can also return to all previously saved documents whenever necessary by accessing the My documents tab in your profile.

- If this is your first time using our platform, the process will require a few additional steps to complete.

- Here's how new users can find the Assignment Of Debt Form For Taxes in our database.

- Carefully read the page content to confirm it includes the sample you need.

- To do this, utilize the form description and preview options if available.

Form popularity

FAQ

In general, you must report any taxable amount of a canceled debt as ordinary income from the cancellation of debt on Form 1040, U.S. Individual Income Tax Return, Form 1040-SR, U.S. Tax Return for Seniors or Form 1040-NR, U.S. Nonresident Alien Income Tax Return as "other income" if the debt is a nonbusiness debt, or

According to the IRS, if a debt is canceled, forgiven or discharged, you must include the canceled amount in your gross income, and pay taxes on that income, unless you qualify for an exclusion or exception. Creditors who forgive $600 or more are required to file Form 1099-C with the IRS.

When it is taxable nonbusiness debt, you'll use the copy of the 1099-C to use to report it on Schedule 1 of Form 1040 as other income.

In most situations, if you receive a Form 1099-C from a lender, you'll have to report the amount on that form to the Internal Revenue Service as taxable income.

If you receive a 1099-C, you may have to report the amount shown as taxable income on your income tax return. Because it's considered income, the canceled debt has tax consequences and may lower any tax refund you were due. The canceled or forgiven amount is entered as other income on Form 1040 or 1040-SR.