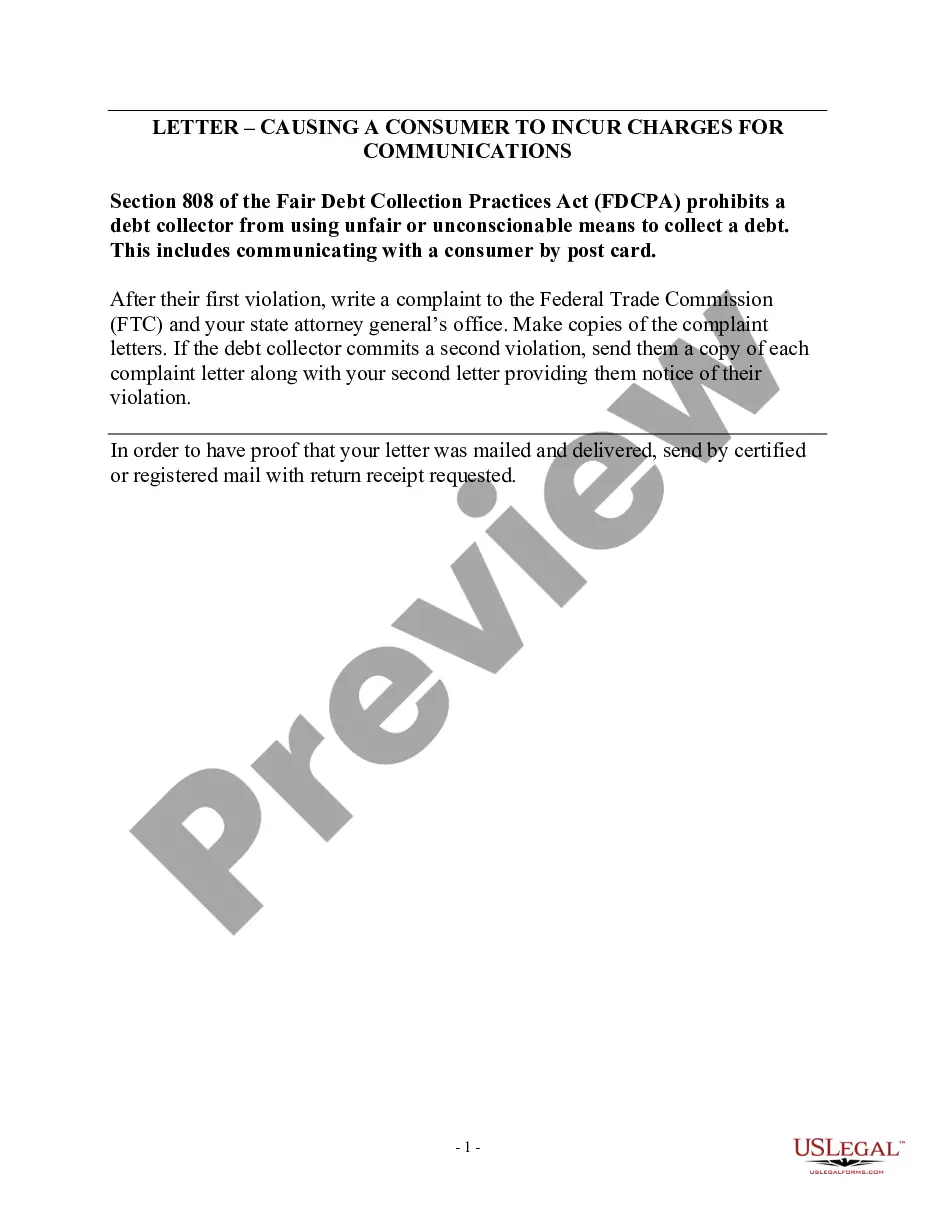

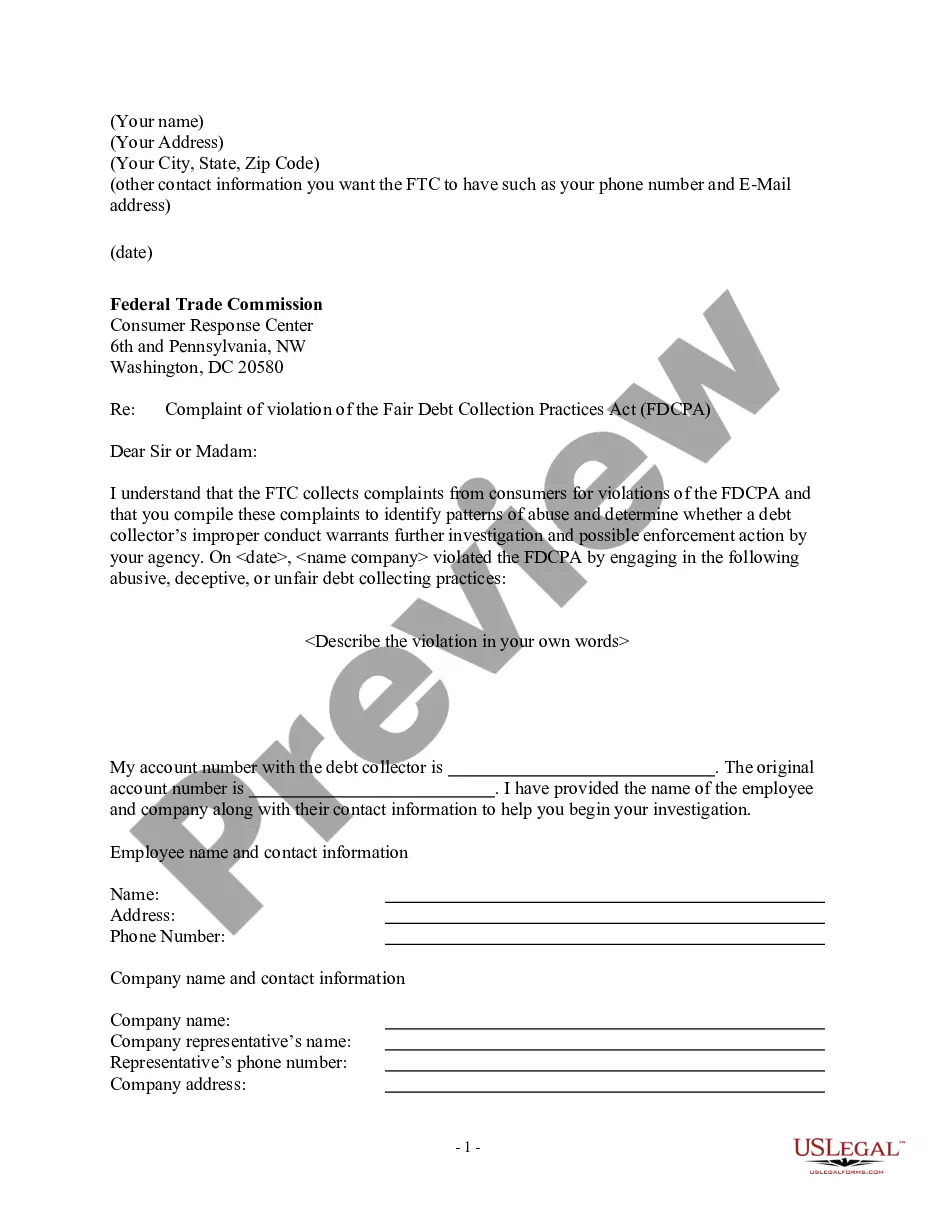

Collection Debt Fdcpa For 1977

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Notice Of Violation Of Fair Debt Act - Notice To Stop Contact?

Employing legal documents that adhere to federal and state regulations is vital, and the web provides a plethora of choices to select from.

But what’s the use in squandering time searching for the fitting Collection Debt Fdcpa For 1977 template online if the US Legal Forms virtual library already has such documents compiled in one place.

US Legal Forms is the most extensive online legal repository with over 85,000 fillable documents crafted by legal professionals for any business and personal situation.

Review the template using the Preview option or through the document outline to confirm it suits your requirements.

- They are easy to navigate with all paperwork organized by state and intended use.

- Our specialists stay updated with legal modifications, so you can always trust that your documents are current and compliant when acquiring a Collection Debt Fdcpa For 1977 from our platform.

- Obtaining a Collection Debt Fdcpa For 1977 is straightforward and fast for both existing and new clients.

- If you already possess an account with an active subscription, Log In and download the document template you need in your chosen format.

- If you are a newcomer to our site, follow the guidelines below.

Form popularity

FAQ

The timeframe for when a debt becomes uncollectible commonly varies based on state law, but typically it ranges from three to six years. Post this period, debt collectors generally lose the legal right to sue you for the payment. Keep in mind that even uncollectible debt may still be reported on your credit history for up to seven years. Engage with a legal expert for advice tailored to your circumstances, especially around the FDCPA.

Filing a lawsuit under the FDCPA includes several crucial steps. Start by gathering evidence of any unfair debt collection practices, such as harassment or threats. Prepare your complaint, including the relevant facts and legal basis for your claim. It's advisable to consult with a legal professional familiar with FDCPA statutes to ensure that you follow the correct procedures.

To initiate a lawsuit under the Fair Debt Collection Practices Act (FDCPA), you need to gather evidence that supports your claim. Collect all documentation concerning the debt, including letters and call logs. Next, file a complaint in the appropriate court, ensuring that you meet the time limits for your case. Consulting with a legal professional can enhance your chances for a successful outcome.

Generally, after seven years, most debts cannot be pursued in court due to statutes of limitations. Debt collectors usually cannot sue for debts older than this timeframe, as specified by the FDCPA. That said, be cautious, as variations exist by state, and some collectors may attempt to bypass these rules. Always seek the advice of a legal expert to understand your rights fully.

Filing a complaint under the Fair Debt Collection Practices Act (FDCPA) is a clear process. First, document every interaction you have with the debt collector, noting dates and details. Next, you can submit your complaint to the Consumer Financial Protection Bureau (CFPB) either online or via mail, and it's also wise to contact your state attorney general. This action helps protect not only your rights but also helps enforce the FDCPA for others.

In general, if a debt is older than seven years, it may no longer be collected through legal means, including wage garnishment. This is due to the Fair Debt Collection Practices Act (FDCPA) and various state laws. However, if a judgment has been entered prior to the debt aging, garnishment could still apply. It is essential to consult a legal expert regarding your specific situation to navigate these complexities.

When communicating with a creditor, avoid making promises you cannot keep or admitting to a debt without verifying its accuracy. Do not disclose personal financial details that could be used against you or express panic, as it may weaken your negotiating position. It's vital to stay calm and informed, especially regarding the Collection debt fdcpa for 1977. Entering conversations armed with confidence will lead to better outcomes.

To outsmart a debt collector under the Collection debt fdcpa for 1977, you should first know your rights. Familiarize yourself with the Fair Debt Collection Practices Act, which protects consumers from abusive collection tactics. Maintain clear communication; keep all correspondence documented and organized. Use your knowledge to negotiate better terms or even dispute invalid debts effectively.

Disputing a debt over seven years old involves contacting the creditor or collection agency to formally challenge the debt's validity. You should provide any documents that support your claim. Utilizing platforms like US Legal Forms can assist you in creating the appropriate documentation to dispute ancient debts related to collection debt fdcpa for 1977.

The time frame for the FDCPA encompasses how long debt collectors have to comply with debt collection laws. This act is designed to protect consumers during the debt collection process, ensuring they are treated fairly. It is crucial to understand this time frame to effectively manage any encounters with collectors related to collection debt fdcpa for 1977.