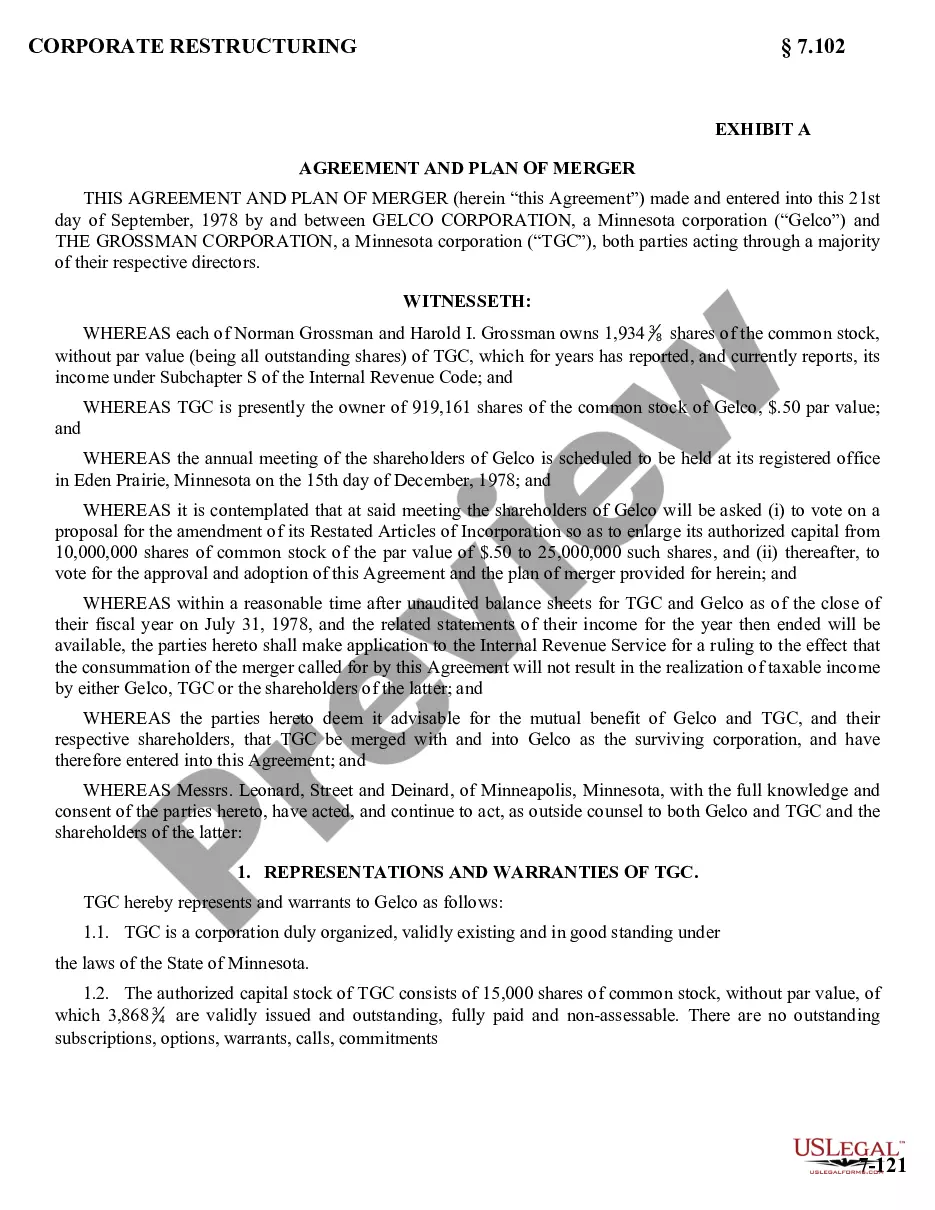

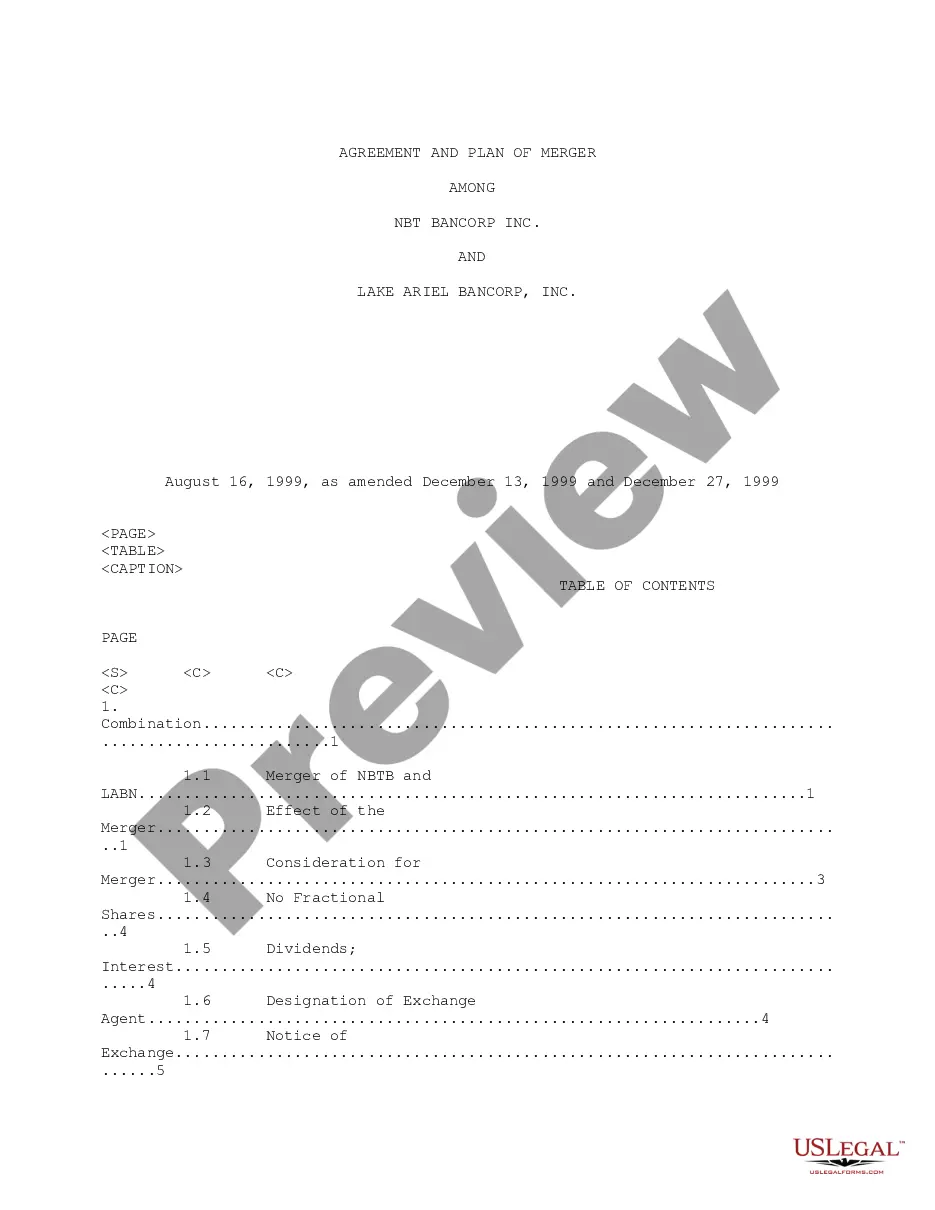

Share Merger Stock For Cash

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Proposed Merger With The Grossman Corporation?

The Share Merger Stock For Cash displayed on this page is a reusable formal template created by expert attorneys in accordance with federal and local statutes and regulations.

For over 25 years, US Legal Forms has offered individuals, businesses, and legal practitioners more than 85,000 confirmed, state-specific documents for any commercial and personal event. It’s the quickest, simplest, and most dependable method to acquire the paperwork you require, as the service ensures the utmost level of data security and anti-malware safeguarding.

Register with US Legal Forms to access verified legal templates for all of life's situations at your fingertips.

- Search for the document you require and examine it.

- Register and Log In.

- Obtain the editable template.

- Fill out and sign the documents.

- Download your documents again.

Form popularity

FAQ

In mergers and acquisitions (M&A), cash can be used for various purposes, such as paying off debt or reinvesting in the new company. If a share merger stock for cash occurs, shareholders receive cash payments, providing them with immediate value. This cash can influence the financial health of the resulting company, as it may enhance its liquidity. Staying informed about these dynamics can help you navigate your investment decisions.

Yes, cash received in a stock merger is generally considered taxable income. When you participate in a share merger stock for cash, you may incur capital gains tax on the profit you make from the sale of your shares. It's important to keep accurate records of your original investment and consult a tax professional to determine your tax obligations. Understanding these implications can help you plan your finances more effectively.

After a merger, your stock shares may be converted into shares of the new company or exchanged for cash. If the merger involves a share merger stock for cash, you will typically receive cash instead of new shares. It's essential to understand the terms of the merger agreement to know how your investment will be affected. You may want to consult with a financial advisor for personalized guidance.

A cash and stock merger occurs when one company offers both cash and shares in exchange for the target company's shares. For example, when Facebook acquired WhatsApp, it offered a combination of cash and Facebook stock to WhatsApp shareholders. This approach can appeal to shareholders who prefer immediate cash while also allowing them to invest in the acquiring company. Understanding these structures is vital when considering a share merger stock for cash strategy.

A notable real-life example of a merger is the acquisition of Disney by Pixar in 2006. This merger combined Disney's extensive distribution network with Pixar's innovative animation technology. The partnership allowed both companies to pool their resources and expertise, resulting in successful film releases. Analyzing such mergers can provide insights into the potential benefits of a share merger stock for cash.

Mergers generally fall into two categories: horizontal and vertical. A horizontal merger occurs between companies in the same industry, like when two airlines combine to enhance market share. On the other hand, a vertical merger involves companies at different stages of production, such as a manufacturer merging with a supplier. Each type can impact how a share merger stock for cash is structured.

In a stock for stock merger, one company exchanges its shares for the shares of another company. For instance, if Company A acquires Company B, shareholders of Company B might receive shares of Company A in exchange for their shares. This type of arrangement allows shareholders to maintain an equity stake in the merged entity, rather than receiving cash. Understanding these transactions can be crucial, especially when considering a share merger stock for cash option.