Distribution

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

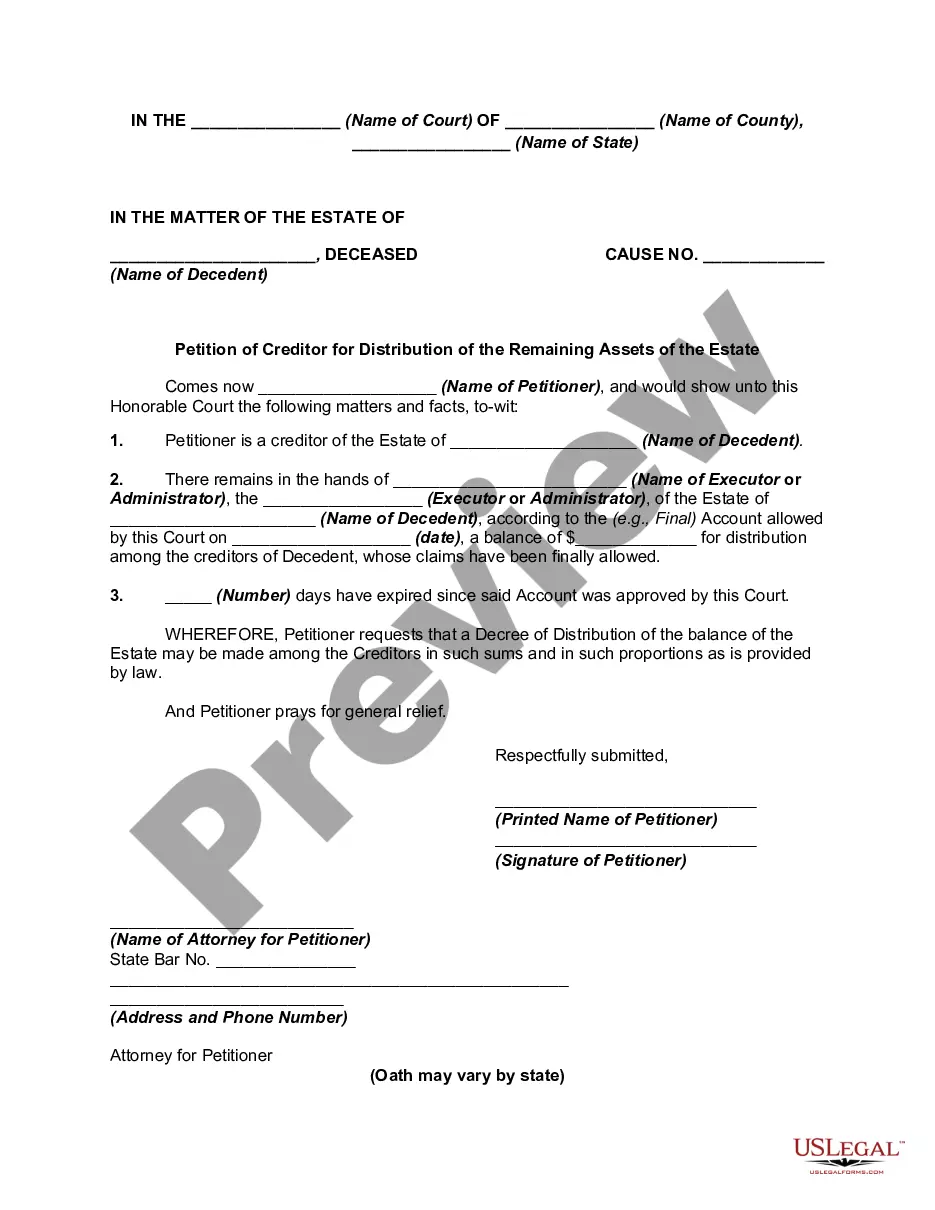

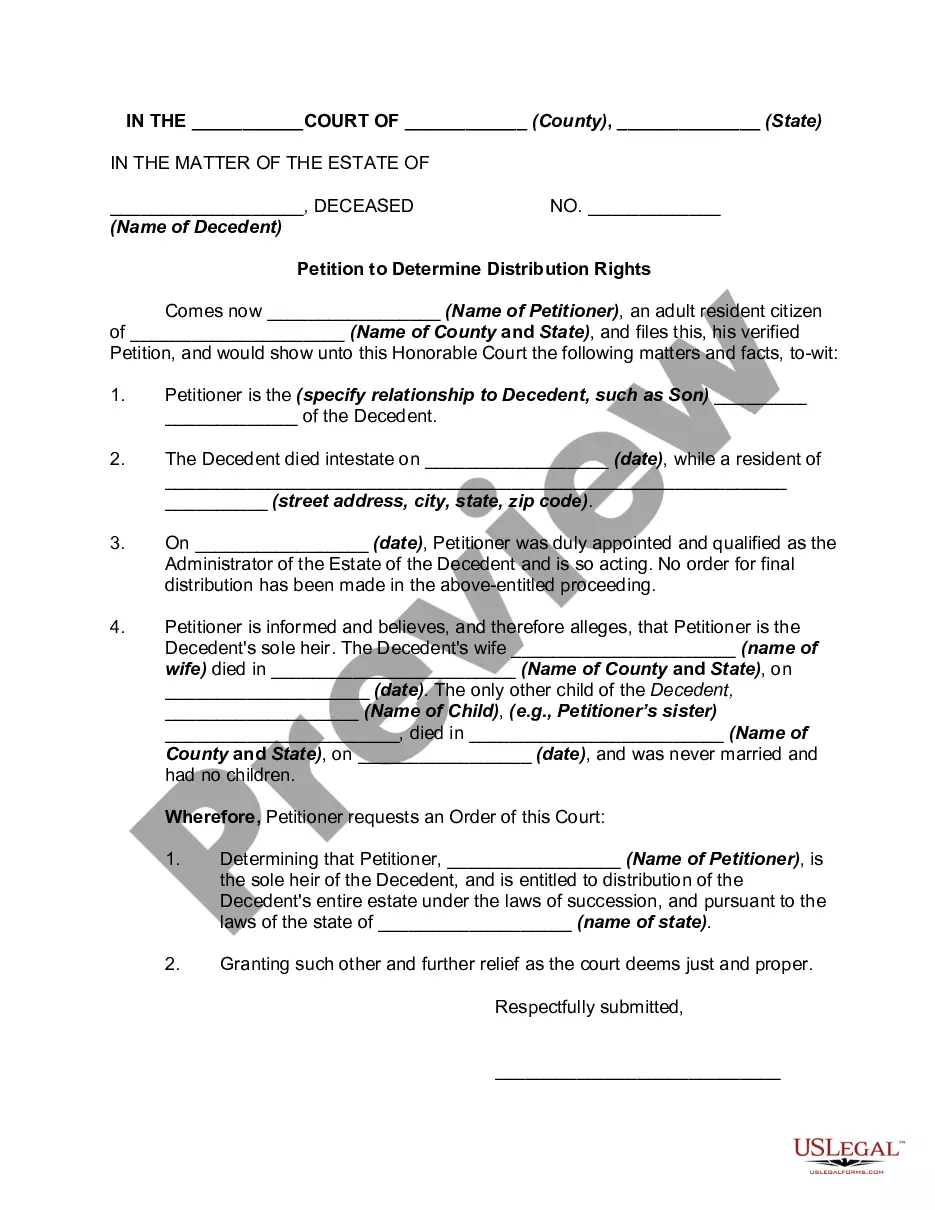

How to fill out Petition For Partial And Early Distribution Of Estate?

- Log in to your account if you are an existing user, ensuring your subscription is active. If your subscription has lapsed, renew it per your payment plan.

- For new users, begin by browsing the extensive library. Use the Preview mode to review the form descriptions, ensuring they meet your specific requirements and comply with local jurisdiction standards.

- If you cannot find the right form, utilize the Search feature to refine your search. This helps you locate a suitable template that fits your needs.

- Once you identify the correct document, click on the Buy Now button, select your preferred subscription plan, and create an account for access.

- Complete the payment process by entering your credit card information or using PayPal to finalize your subscription.

- After purchase, download the form to your device. You can also access previous downloads anytime in the My Forms section of your profile.

By leveraging US Legal Forms, you not only gain access to a robust collection of templates but also can consult with premium experts for assistance in form completion, ensuring accuracy and compliance.

Start navigating the world of legal documents efficiently with US Legal Forms today—your reliable partner in legal distribution.

Form popularity

FAQ

You do need to report distributions, especially if they are taxable. Reporting ensures that you comply with IRS regulations and accurately reflect your income. It's best to consult tax guidelines or use a platform like USLegalForms to assist you in navigating these requirements effectively.

The IRS distribution rule generally mandates that distributions from retirement accounts and investment vehicles are subject to taxation. The specifics can vary based on your account type and your age at the time of distribution. Familiarizing yourself with these rules can save you from unpleasant surprises during tax season.

To report a distribution on your tax return, you will typically include it on Form 1040 or your respective tax form. You will enter the total distribution amount under the appropriate line for taxable income. Make sure to reference the information from your Form 1099 to accurately report these figures.

Yes, distributions typically count as income. When you receive a distribution, it is usually taxable and must be reported on your tax return. This means including it in your total income for the year. However, certain types of distributions may have special tax treatments, so understanding the specifics is essential.

Distributions are reported to the IRS using Form 1099-DIV or Form 1099-MISC, depending on the type of distribution. These forms provide details about the amount distributed and the recipient's information. You receive this form from the financial institution or company issuing the distribution. It’s important to keep this document for your tax records.

When you turn 70, you must start taking required minimum distributions (RMDs) from your IRA to comply with IRS regulations. The amount you need to withdraw depends on your account balance and life expectancy factor determined by IRS tables. It's essential to calculate these distributions carefully to avoid penalties, and platforms like uslegalforms can help you navigate the rules and ensure compliance.

To avoid a significant tax deduction on your 401k withdrawal, consider using a rollover option that transfers funds to an IRA. This method avoids immediate taxation and allows for continued growth of your retirement funds. Additionally, ensure you meet certain criteria, such as age or hardship, which may provide tax benefits during your withdrawal process.

Determining the taxable amount of your IRA distribution involves a few key steps. First, identify whether your IRA is traditional or Roth, as this impacts taxation. For traditional IRAs, your contributions may have been tax-deductible, so distributions are generally taxable. You can calculate the taxable portion by considering your total contributions and prior distributions, ensuring you comply with IRS rules.

The percentage a distribution deal takes can vary widely depending on factors like product type, market conditions, and the terms of your agreement. Generally, distributors may take between 15% to 30% of sales, but this can differ based on negotiation and the value the distributor brings to the partnership. Understanding these percentages in advance can help you structure a competitive deal.

To secure a distribution deal, start by demonstrating the potential of your product to the right audience. Create marketing materials, and provide samples to influential distributors. Attend networking events and build relationships with key players, and don’t hesitate to utilize platforms like US Legal Forms to streamline your contracting process.