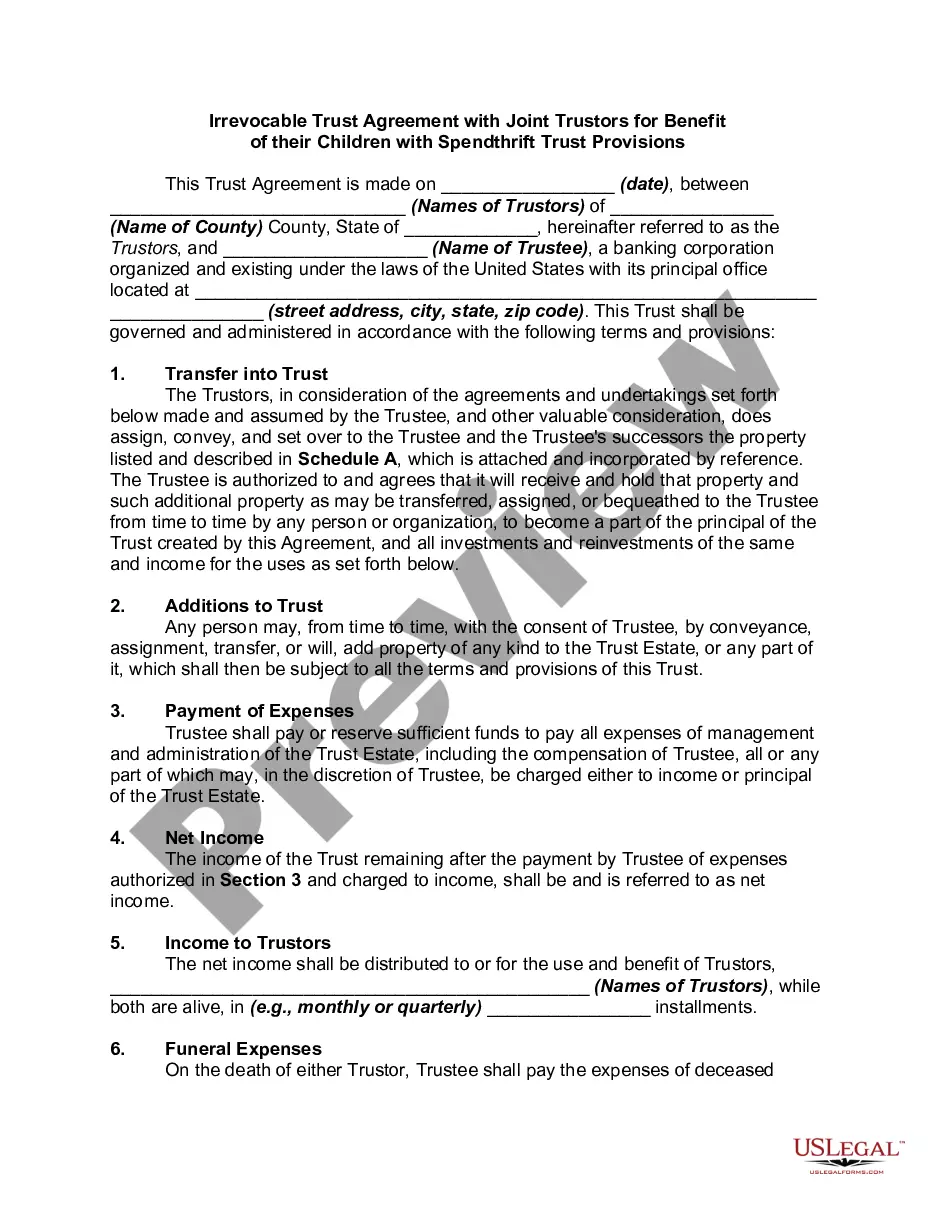

Irrevocable Trust Document For Lottery Winnings

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Irrevocable Trust Agreement For Benefit Of Trustor's Children And Grandchildren With Spendthrift Trust Provisions?

The Unalterable Trust Document For Lottery Earnings you observe on this page is a versatile legal template crafted by expert attorneys in compliance with national and local laws and regulations.

For over 25 years, US Legal Forms has supplied individuals, businesses, and legal professionals with more than 85,000 verified, state-specific documents for any commercial and personal circumstance. It’s the fastest, most direct, and most reliable way to acquire the documents you require, as the service guarantees the utmost level of data protection and anti-virus security.

Use the same document again whenever necessary. Access the My documents section in your profile to redownload any previously saved forms. Join US Legal Forms to have verified legal templates for all of life's circumstances available at your fingertips.

- Look for the document you need and review it.

- Browse through the file you searched and preview it or check the form description to confirm it meets your requirements. If it does not, utilize the search function to find the correct one. Click Buy Now once you have located the template you require.

- Register and sign in.

- Select the payment plan that fits you and create an account. Use PayPal or a credit card for a swift transaction. If you already possess an account, Log In and examine your subscription to proceed.

- Obtain the fillable template.

- Choose the format you prefer for your Unalterable Trust Document For Lottery Earnings (PDF, DOCX, RTF) and download the document onto your device.

- Complete and sign the documentation.

- Print out the template to fill it in manually. Alternatively, use an online multi-functional PDF editor to swiftly and accurately complete and sign your form with a valid signature.

Form popularity

FAQ

If you win the lottery, the best trust to set up is an irrevocable trust document for lottery winnings. This type of trust allows you to protect your newfound wealth from taxes and creditors, while also ensuring that your assets are distributed according to your wishes. By placing your winnings in an irrevocable trust, you prevent yourself from making impulsive decisions that could affect your financial future. Utilizing a service like USLegalForms can simplify the process, helping you create a tailored irrevocable trust document for lottery winnings that fits your specific needs.

Remaining anonymous after winning the lottery largely depends on the laws of your state. Some jurisdictions allow winners to claim their prizes through a trust or legal entity, providing anonymity. By setting up an irrevocable trust document for lottery winnings, you can safely protect your identity while enjoying the financial benefits of your win.

The safest place to put lottery winnings is in a well-insured financial institution, like a bank or credit union, that offers FDIC insurance. You might also consider establishing an irrevocable trust document for lottery winnings, which provides an additional layer of protection and ensures your funds are managed according to your wishes in the long run.

If you win $1 million dollars, the IRS typically withholds 24% for federal taxes, which means you could owe around $240,000 upfront. However, the total tax obligation may be higher depending on your tax bracket. It’s wise to consult with a tax professional who can help you navigate the implications of your winnings, potentially utilizing an irrevocable trust document for lottery winnings to manage tax liabilities.

To claim lottery winnings with a trust, you need to establish a trust first, such as an irrevocable trust. This involves drafting the appropriate trust documents, which specify that the trust will receive the lottery payout. Once set up, you can present the trust documentation to the lottery officials during the claim process.

If you win the lottery, the first step is to stay calm and avoid making hasty decisions. You should secure your winning ticket and consider consulting a financial advisor or an attorney who specializes in trusts. This is the ideal time to explore creating an irrevocable trust document for lottery winnings, as it provides long-term protection for your assets.

An irrevocable trust document is a legal tool that allows you to transfer assets into a trust, which cannot be changed or revoked once established. This type of trust is particularly useful for lottery winners, as it can protect winnings from creditors and minimize tax implications. By using an irrevocable trust document for lottery winnings, you can secure your financial future more effectively. It's a proactive step towards managing your wealth.

To minimize taxes on lottery winnings, consider forming an irrevocable trust document for lottery winnings. This strategy can help you manage your estate and reduce the taxable amount significantly. Additionally, consulting with a tax professional can provide personalized advice tailored to your financial situation. Using the right legal tools, you can protect a larger portion of your winnings.