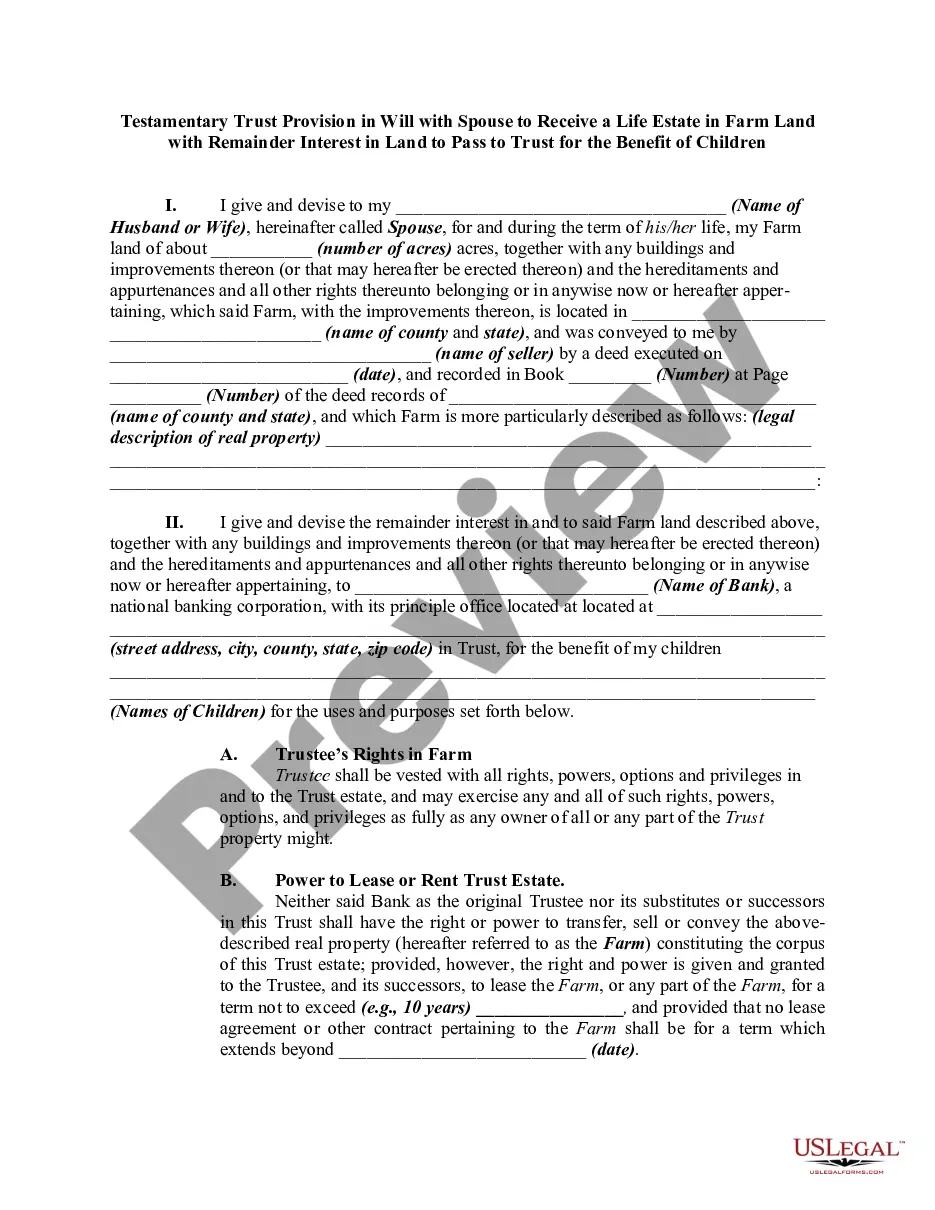

Testamentary Trust Form

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

In general, you cannot obtain a letter of testamentary without going through probate. The letter serves as official permission from the court to act on behalf of the deceased's estate. However, some states may recognize small estate affidavits, which can help you bypass probate for smaller estates. Utilizing a testamentary trust form can also facilitate the process if you plan to manage assets in a trust.

You can obtain a letter of testamentary through your local probate court. Typically, you will need to file the necessary documents, including a testamentary trust form, to initiate the process. Once approved, the court will issue the letter, allowing you to administer the estate accordingly. You may also consider using platforms like US Legal Forms, which provide guidance and templates to streamline your application.

The primary documents needed for a testamentary trust include your will, the trust document, and identifying information for the trustee and beneficiaries. Additionally, documentation regarding the assets allocated to the trust is crucial. Using a testamentary trust form can streamline gathering these documents and ensure you don’t overlook any important details.

To establish a testamentary trust, you need to create a will that includes specific provisions for the trust. This will usually involve deciding on the beneficiaries, the trustee, and the assets that will fund the trust. You can use a testamentary trust form to guide you through this process, making it easier to capture all necessary information.

Yes, a testamentary trust is generally required to file a tax return if it earns income. This is because the trust is treated as a separate legal entity for tax purposes. Be sure to consult a tax professional to avoid any complications when filing, and ensure that your testamentary trust form accounts for potential tax liabilities.

One significant mistake parents make is failing to clearly define the terms of the trust in the testamentary trust form. This lack of clarity can lead to confusion and conflict among beneficiaries. It's essential to communicate your intentions clearly and consider professional guidance to ensure that your wishes are fulfilled.

To create a testamentary trust, you typically need a valid will that outlines the trust's terms, the trust document itself, and any necessary identification for the trustee and beneficiaries. It's also wise to gather any documents related to the assets that will fund the trust. You may find a testamentary trust form helpful in ensuring you include all required details.

Testamentary trusts may encounter several challenges, including potential delays in asset distribution and added administrative costs. Because these trusts take effect only after your death, beneficiaries may face waiting periods that can pose financial burdens. Additionally, tax implications can complicate the management of trust assets. Utilizing a well-designed testamentary trust form can address these issues, ensuring smoother administration and clearer expectations.

One significant risk associated with testamentary trusts is the possibility of disputes among beneficiaries. Conflicting interpretations of the trust's terms can lead to misunderstandings and legal challenges. Furthermore, if the appointed trustee fails in their duties, it may endanger the trust's purpose. Therefore, using a clear testamentary trust form can help minimize these risks by setting explicit guidelines.

In a testamentary trust, the trust itself holds ownership of the assets, managed by the appointed trustee. The beneficiaries of the trust have a beneficial interest in those assets but do not own them outright until the terms of the trust are met. This arrangement provides a structured approach to asset distribution. You can establish this structure efficiently through a well-prepared testamentary trust form.