This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

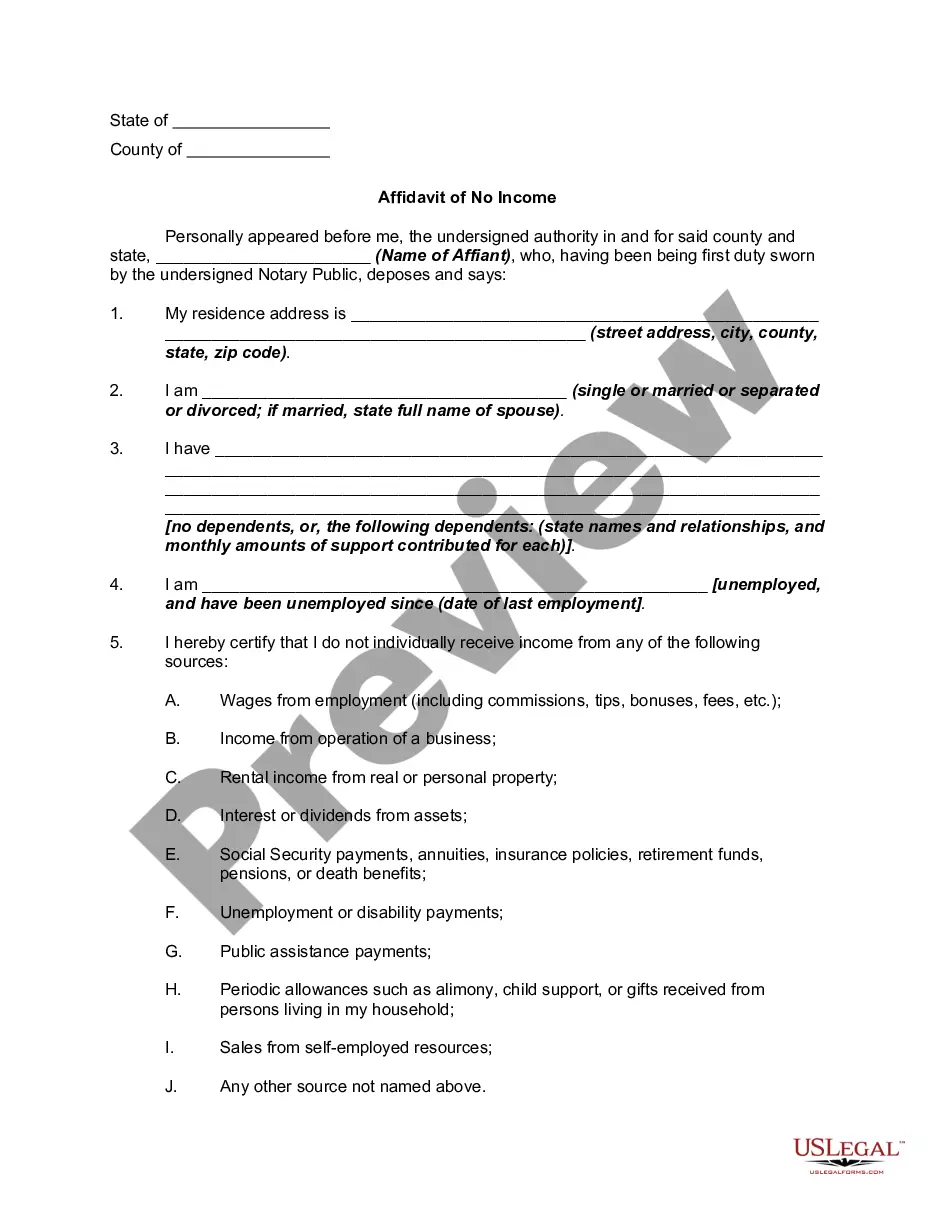

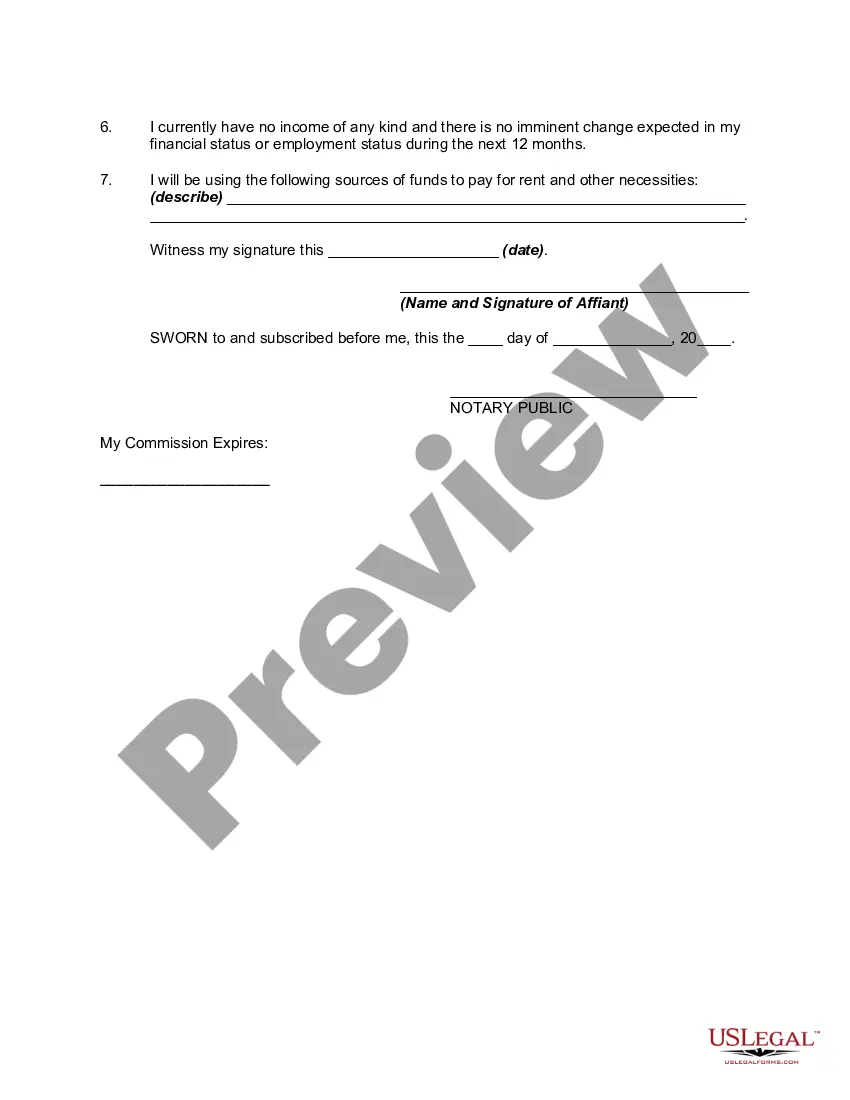

A Certificate of No Income from the Bureau of Internal Revenue (BIR) is an official document issued by the tax agency in certain countries, such as the Philippines, to certify that an individual or business has no reportable income or taxable transactions for a specific period. This certificate is usually required when applying for certain government benefits or when conducting transactions that require proof of income. Keywords: Certificate of No Income, BIR, Bureau of Internal Revenue, no reportable income, taxable transactions, official document, government benefits, proof of income. In the Philippines, there are two types of Certificates of No Income issued by the Bureau of Internal Revenue (BIR): 1. Certificate of No Income for Individuals: This certificate is obtained by individuals who have no taxable income and are not engaged in any business or profession that generates income. It verifies that the individual has no reportable income to the BIR within a specific period. 2. Certificate of No Income for Businesses: This certificate is obtained by businesses that have not engaged in any income-generating activities during a specific period and have no taxable transactions to report to the BIR. It confirms that the business has no income to declare and serves as proof of their non-taxable status. Both types of Certificates of No Income are essential for individuals and businesses seeking to establish their non-taxable status during a particular period. These certificates may be required for various purposes, including but not limited to social security benefits applications, loan applications, visa applications, and other transactions where proof of income is necessary. To obtain a Certificate of No Income from the BIR, individuals or businesses are typically required to provide supporting documents and follow the prescribed procedures set by the tax agency. These may include submission of notarized affidavits stating the absence of income, copies of previous tax returns, and other relevant documents as deemed necessary by the BIR. It is essential to note that the Certificate of No Income does not exempt individuals or businesses from their tax obligations if their financial circumstances change or if they engage in income-generating activities in the future. The certificate only serves as a declaration that no reportable income or taxable transactions were identified within the specified period covered by the certificate.