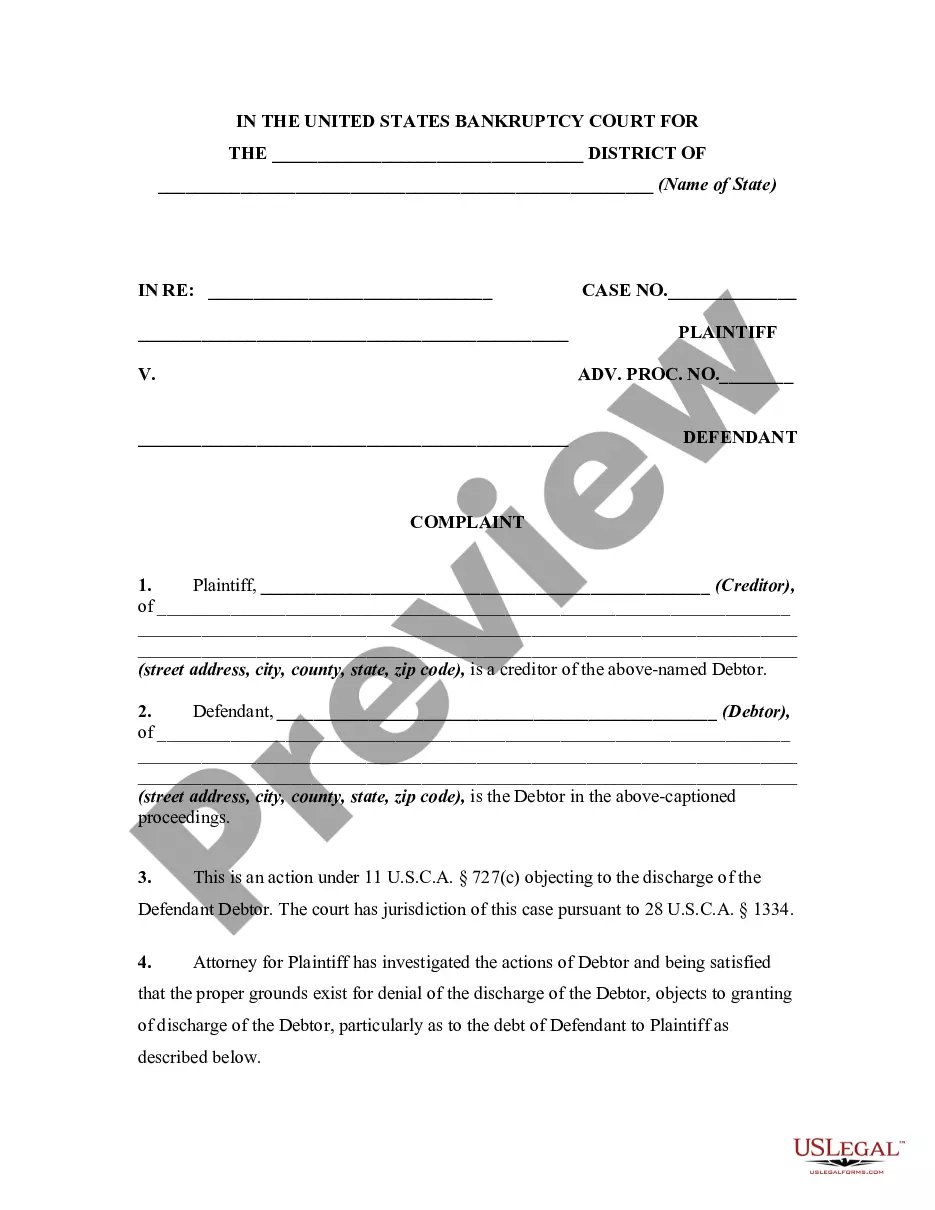

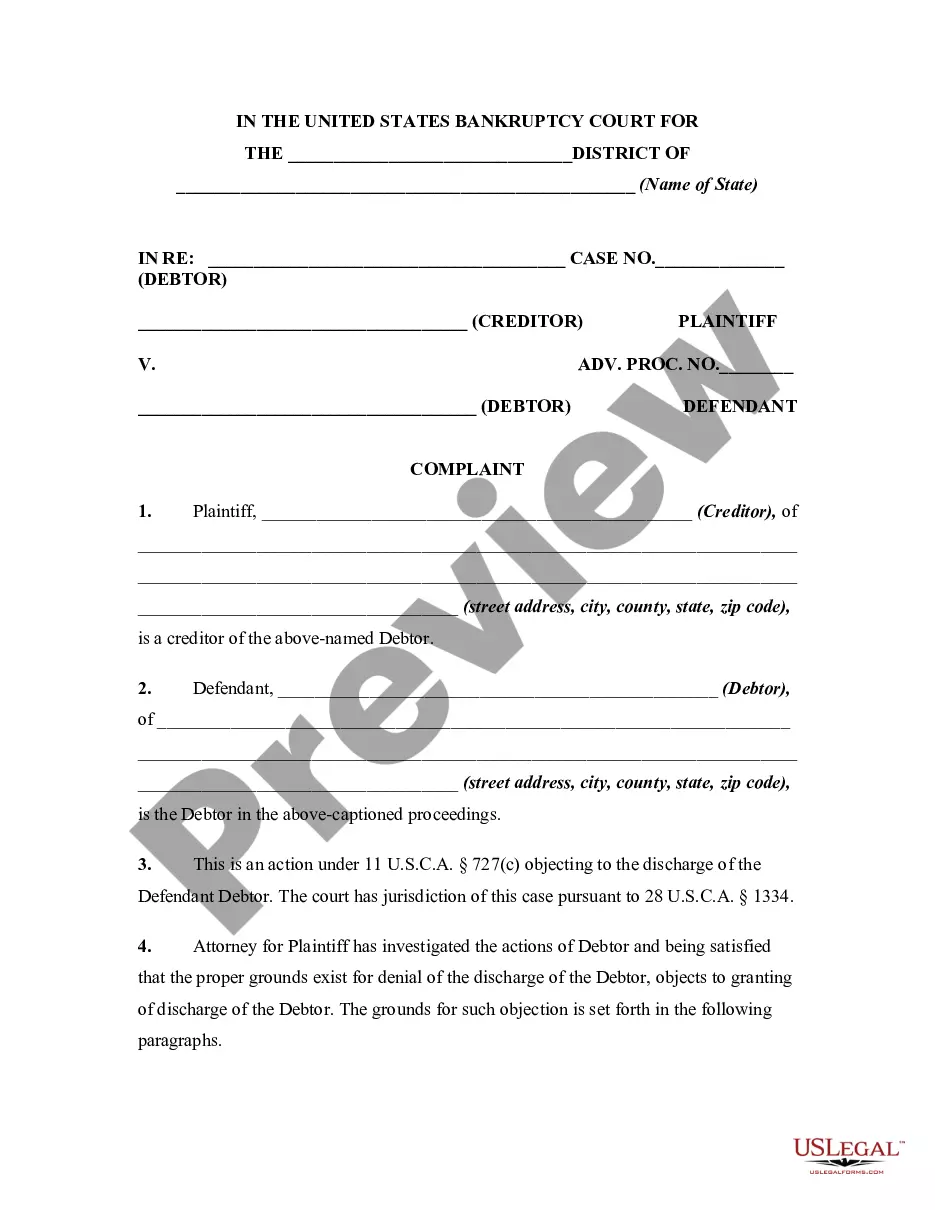

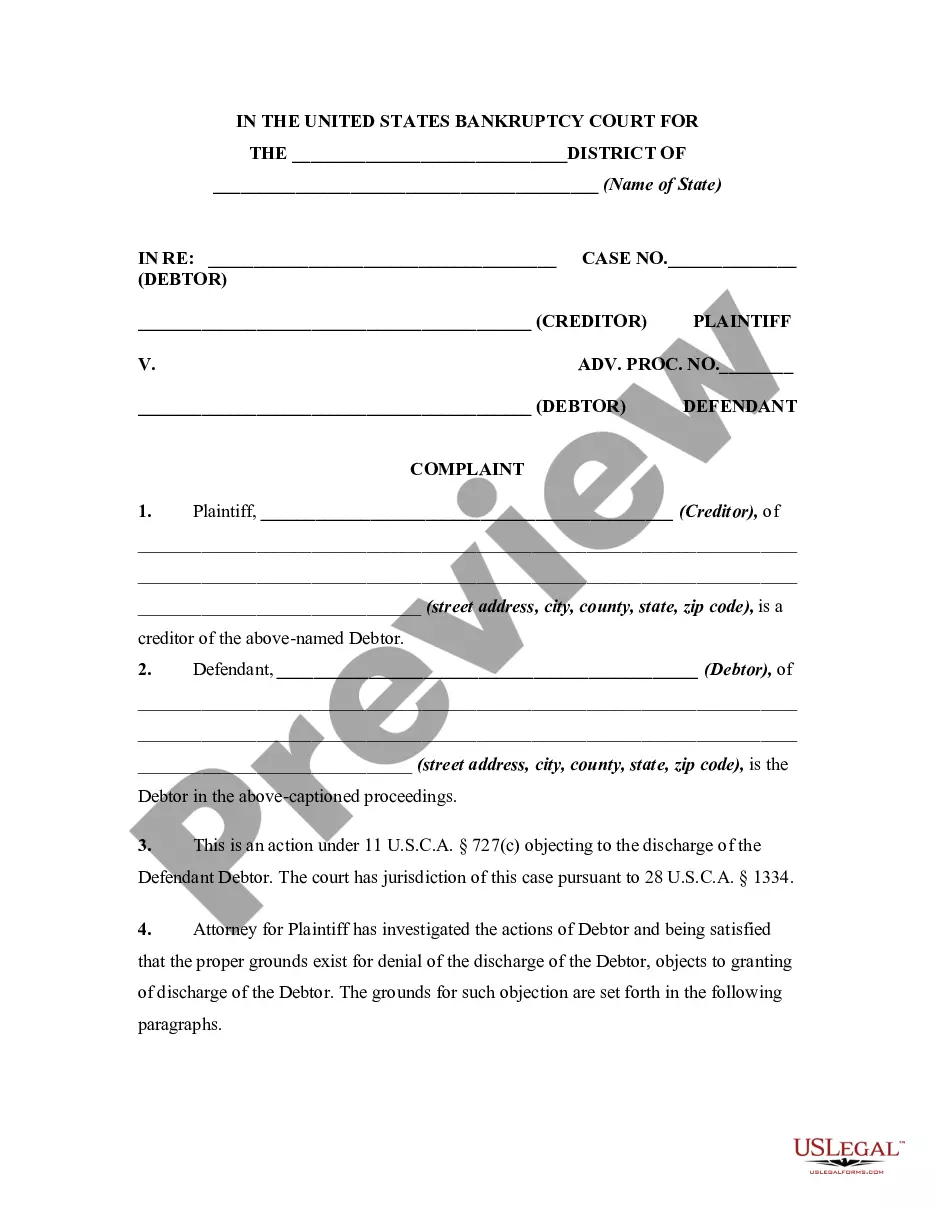

Bankruptcy For Property Taxes

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Complaint Objecting To Discharge In Bankruptcy Proceedings For Concealment By Debtor And Omitting From Schedules Fraudulently Transferred Property?

- Log in to your US Legal Forms account if you're a returning user, and select the required form template. Ensure that your subscription is active; if not, renew it based on your chosen plan.

- For first-time users, start by exploring the Preview mode to read the form description carefully. This ensures the selected document aligns with your specific legal requirements.

- If you need a different template, utilize the Search function at the top to locate the appropriate documents that meet your needs.

- Once you find your desired form, click on the Buy Now button and select your preferred subscription plan to access the library.

- Complete your purchase by entering your payment information, either via credit card or PayPal, to secure your subscription.

- After payment, download the form to your device. You can also find your document anytime in the My Forms section of your account.

By following these steps, you can efficiently obtain the necessary documents to assist with bankruptcy for property taxes. US Legal Forms stands out with its extensive library, providing over 85,000 customizable forms and access to expert assistance.

Don’t hesitate to take control of your financial future—start your journey with US Legal Forms today!

Form popularity

FAQ

In the context of bankruptcy for property taxes, tax-related debts emerge as some of the toughest to discharge. Federal taxes, especially if they are due within a certain window, frequently cannot be eliminated through bankruptcy. Additionally, debts like child support and alimony often add to the complexity. Understanding this landscape can guide you in making informed decisions about your financial future.

As you explore bankruptcy for property taxes, remember that certain debts will not go away through this process. Three significant examples include child support, tax obligations, and student loans. Each of these debts has specific legal stipulations that prevent them from being discharged. Hence, planning ahead and knowing what remains after bankruptcy is critical for your financial well-being.

When it comes to bankruptcy for property taxes, specific debts cannot be erased or reduced in the process. For example, secured debts linked to property, such as mortgages, typically stay with the property even if you file for bankruptcy. Moreover, federal tax debts, alimony, and most student loans present challenges as they often survive bankruptcy. It’s important to understand these types of debt when determining your financial strategy.

Understanding what debts cannot be discharged by bankruptcy is essential for anyone considering this route. Generally, debts related to property taxes are not dischargeable, meaning you will still owe them even after bankruptcy. Additionally, student loans, certain taxes, and child support obligations often remain after bankruptcy. Therefore, it is crucial to know these limitations when weighing your options.

Yes, it is possible to discharge some taxes in bankruptcy, but there are strict rules. Typically, income taxes may be discharged if they meet criteria such as age and proper filing. Property taxes have additional considerations, which impacts their dischargeability. Navigating these rules effectively may require utilizing a resource like US Legal Forms as part of your journey with bankruptcy for property taxes.

Discharging taxes through bankruptcy requires specific conditions to be met. You must file your bankruptcy case correctly and ensure your taxes meet the necessary requirements for discharge, such as being due for several years and filing your tax returns. A clear understanding of these rules can simplify the process. Using the US Legal Forms platform can guide you through the necessary procedures for bankruptcy for property taxes.

Certain debts remain non-dischargeable even after filing for bankruptcy. These include child support, alimony, student loans, and some tax obligations. Particularly, property tax debts may not be dischargeable under certain circumstances. Being informed about these exceptions helps you prepare better for bankruptcy for property taxes.

The 3 year rule refers to the time limit for discharging certain tax debts in bankruptcy. Typically, you can discharge income tax debts if they are at least three years old at the time of filing. However, this does not apply to property taxes, which follow different criteria. Timely understanding of these rules is essential for those looking into bankruptcy for property taxes.

The 240 day rule is a guideline concerning the discharge of property taxes during bankruptcy. Specifically, if you owe property taxes, they may be discharged if they are not due within 240 days of filing your bankruptcy petition. This rule aims to give taxpayers some relief and clarity as they navigate their financial situation. Understanding this can be crucial when considering bankruptcy for property taxes.

Bankruptcy may wipe out some taxes, but it is not a blanket solution for all tax debts. Specific requirements must be met, including the type of tax and how long ago it was due. In many cases, bankruptcy for property taxes can significantly reduce the financial burden and provide a manageable repayment solution. It is crucial to seek guidance from professionals familiar with tax law to navigate this complex area.