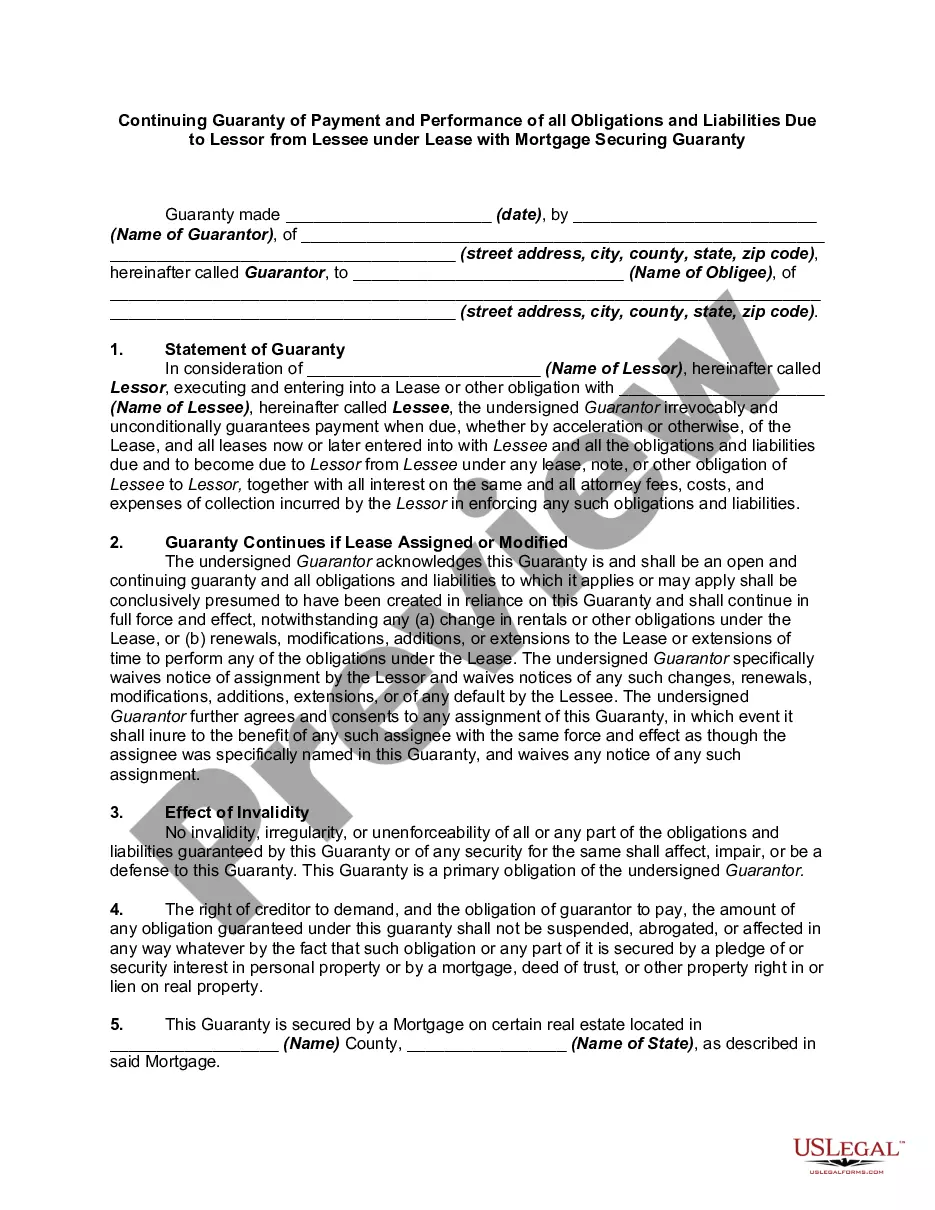

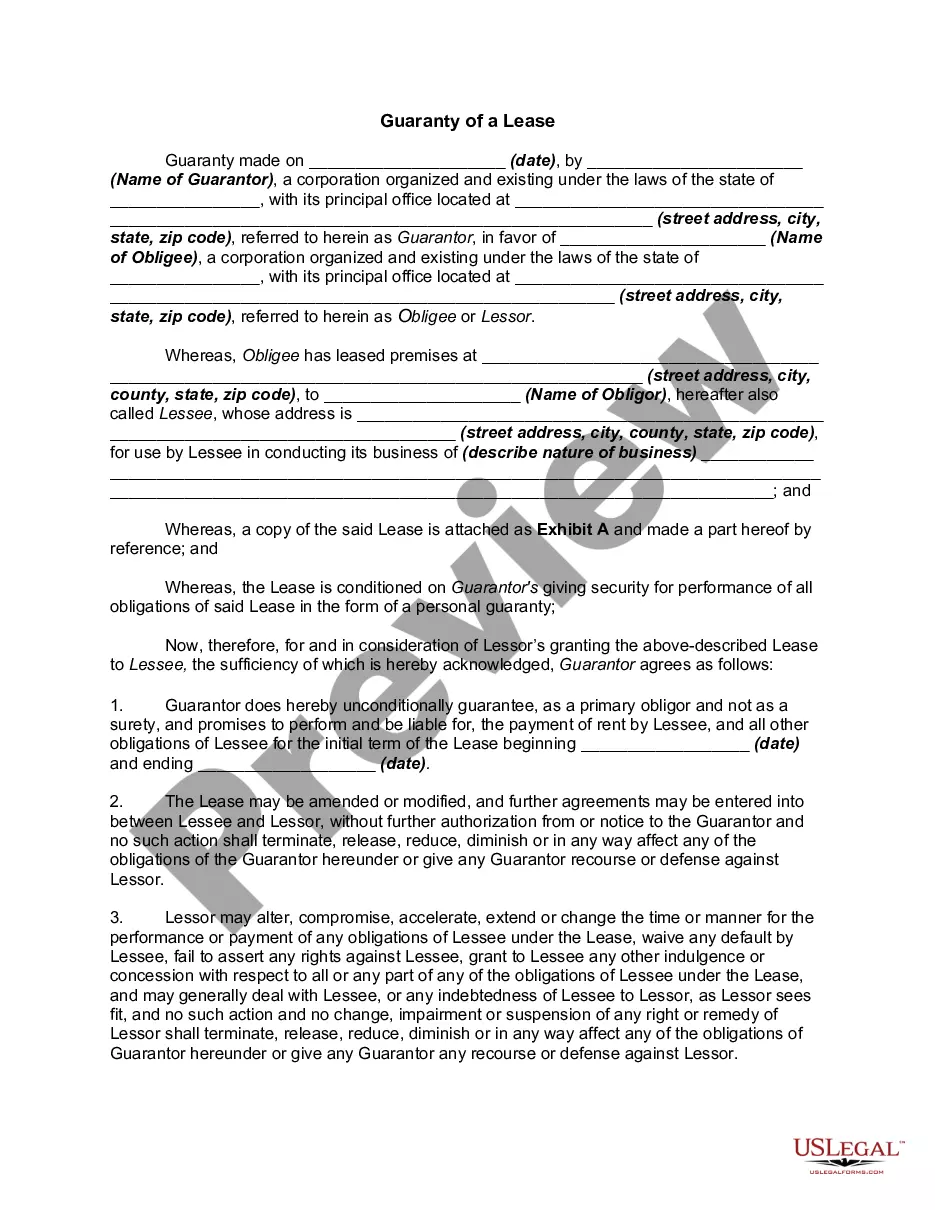

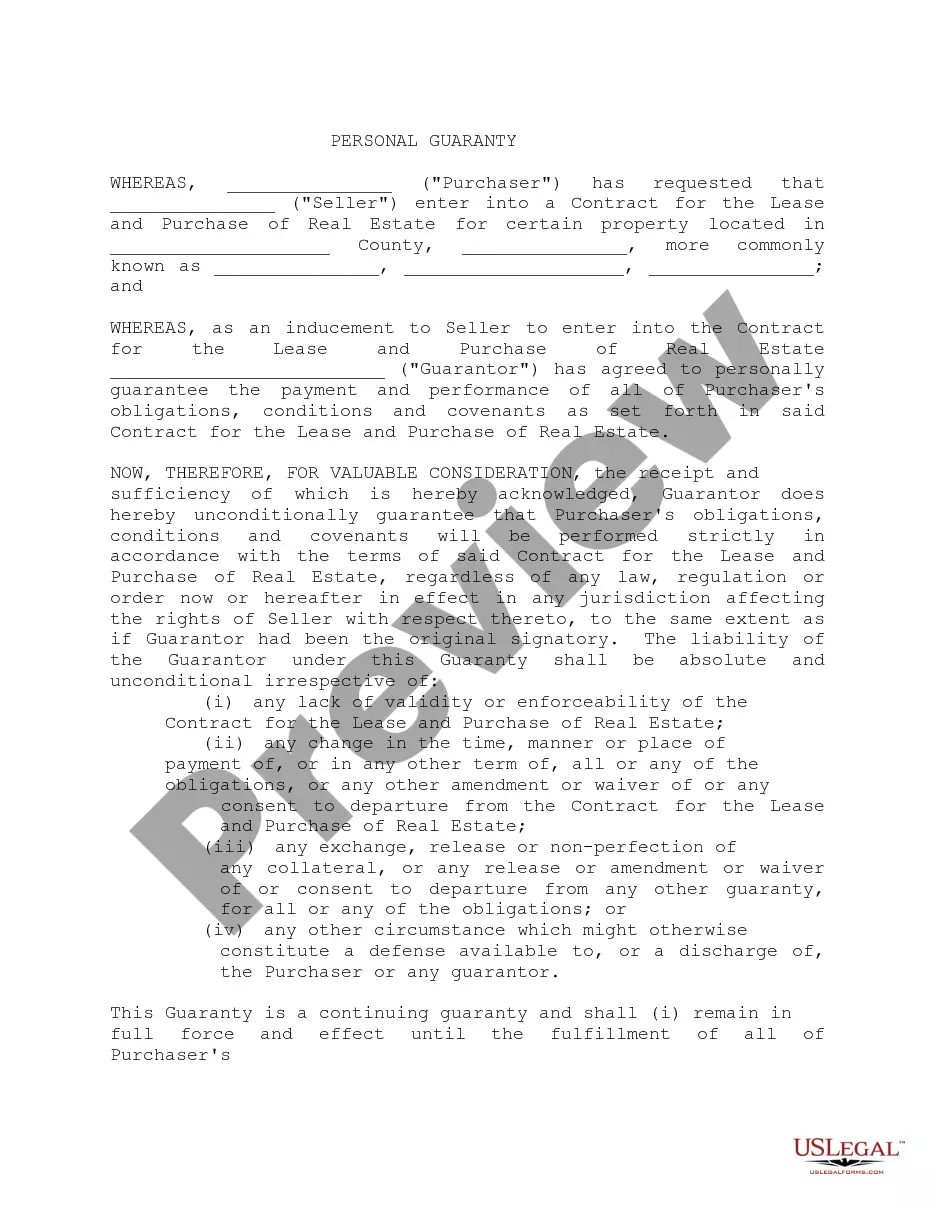

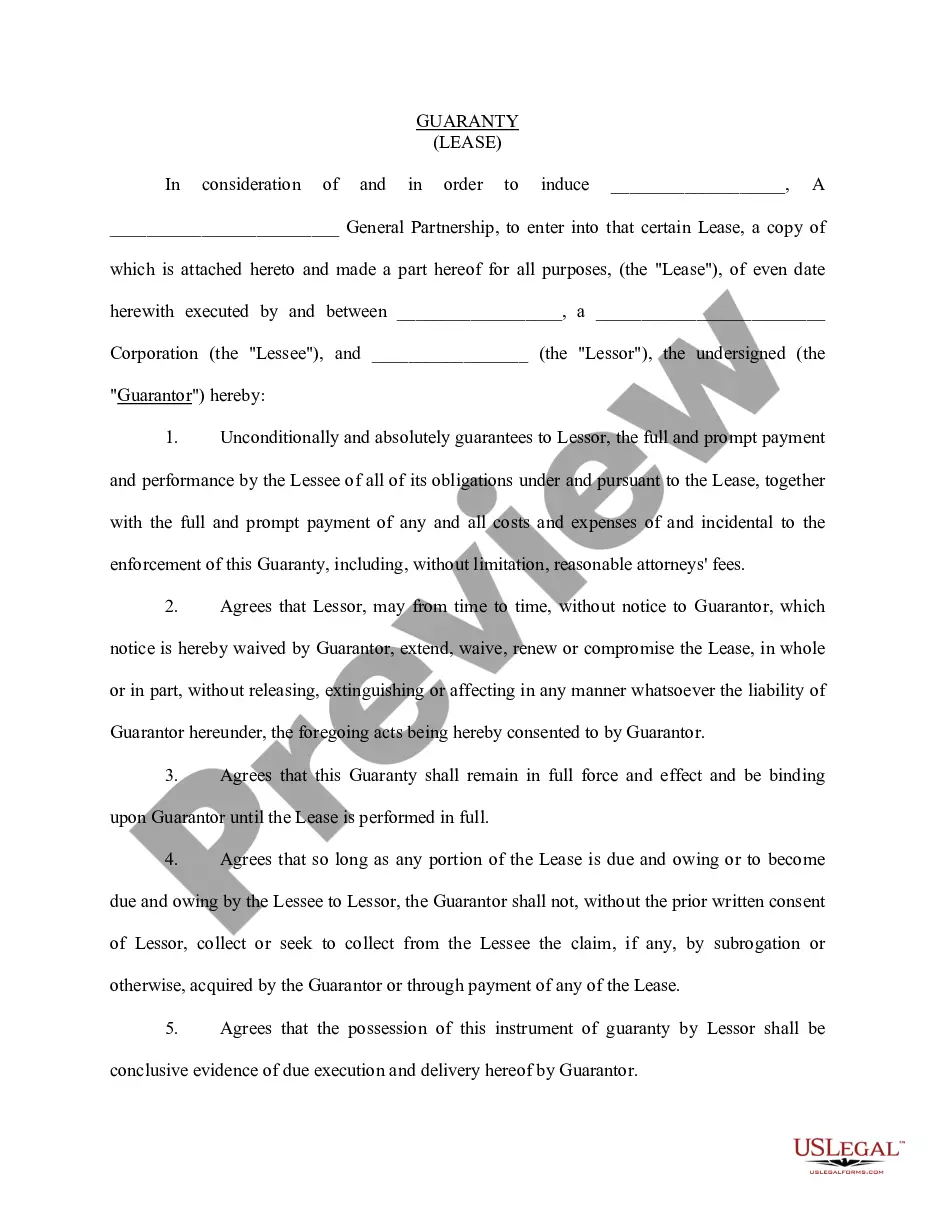

Mortgage Lease Purchase Without

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Mortgage Securing Guaranty Of Performance Of Lease?

It’s well-known that you cannot instantly turn into a legal expert, nor can you comprehend how to swiftly create a Mortgage Lease Purchase Without without a specialized education.

Drafting legal documents is an extensive process that demands specific training and expertise.

So why not leave the creation of the Mortgage Lease Purchase Without to the professionals.

Preview it (if this option is available) and read the accompanying description to determine whether the Mortgage Lease Purchase Without is suitable for you.

If you need another template, start your search again.

- With US Legal Forms, one of the largest collections of legal templates, you can find anything from court paperwork to templates for internal business correspondence.

- We recognize how vital compliance and adherence to federal and state regulations are.

- This is why, on our site, all forms are location-specific and current.

- Let’s begin with our platform and acquire the document you need in just a few minutes.

- Locate the document you require using the search bar at the top of the page.

Form popularity

FAQ

The journal entry for a lease typically includes a debit to the right-of-use asset and a credit to the lease liability. This entry properly reflects your obligations and assets related to the lease. If you prefer a clear and easy process, using the US Legal Forms platform can help streamline your understanding of a mortgage lease purchase without confusion.

Accounting for a lease buyout involves recognizing the total buyout amount as an expense in your financial records. You will need to adjust both the asset and liability on your balance sheet to reflect this action. If you are exploring a mortgage lease purchase without complications, track these transactions carefully to maintain accurate records.

Common excuses to break a lease include job relocation, financial hardship, or health issues. It's best to consult your lease agreement for any specific clauses that allow for termination. If you're dealing with a mortgage lease purchase without flexibility, consider discussing your circumstances with your landlord to negotiate a potential solution.

To record a lease in accounting, you must recognize the lease liability and the right-of-use asset. Calculate the present value of future lease payments to determine the liability amount. This approach ensures you showcase the mortgage lease purchase without skipping essential financial reporting details.

Renting out your house without telling your mortgage lenders could jeopardize the agreement, leading to penalties in the form of costs and fees. If you find that the terms of your mortgage no longer meet your needs, homeowners are able to break or renegotiate their mortgage contract before the end of the term.

For example, a tenant and landlord may agree to a five-year lease with a five-year option to renew. At the end of the first five years, the tenant is given the chance to continue the lease for another five years. If you think you may renew, be sure to bring up extension provisions with your landlord.

The CRA obtains information about rental income through various means, such as data matching with property records and information received from third parties, including banks and financial institutions. They may also conduct audits and investigations to ensure compliance with reporting requirements.

The lease purchase also buys time for a potential buyer to repair their credit and save up for a down payment toward a conventional mortgage prior to the expiration of the option. The length of the option can be negotiated and a longer term gives the buyer more time to get things in order.

Option to Buy: Lease Purchase Agreement: In a lease purchase agreement, the tenant is typically obligated to buy the property at the end of the lease term. Unlike the lease-to-own agreement, the tenant does not have the option to walk away without buying the property.