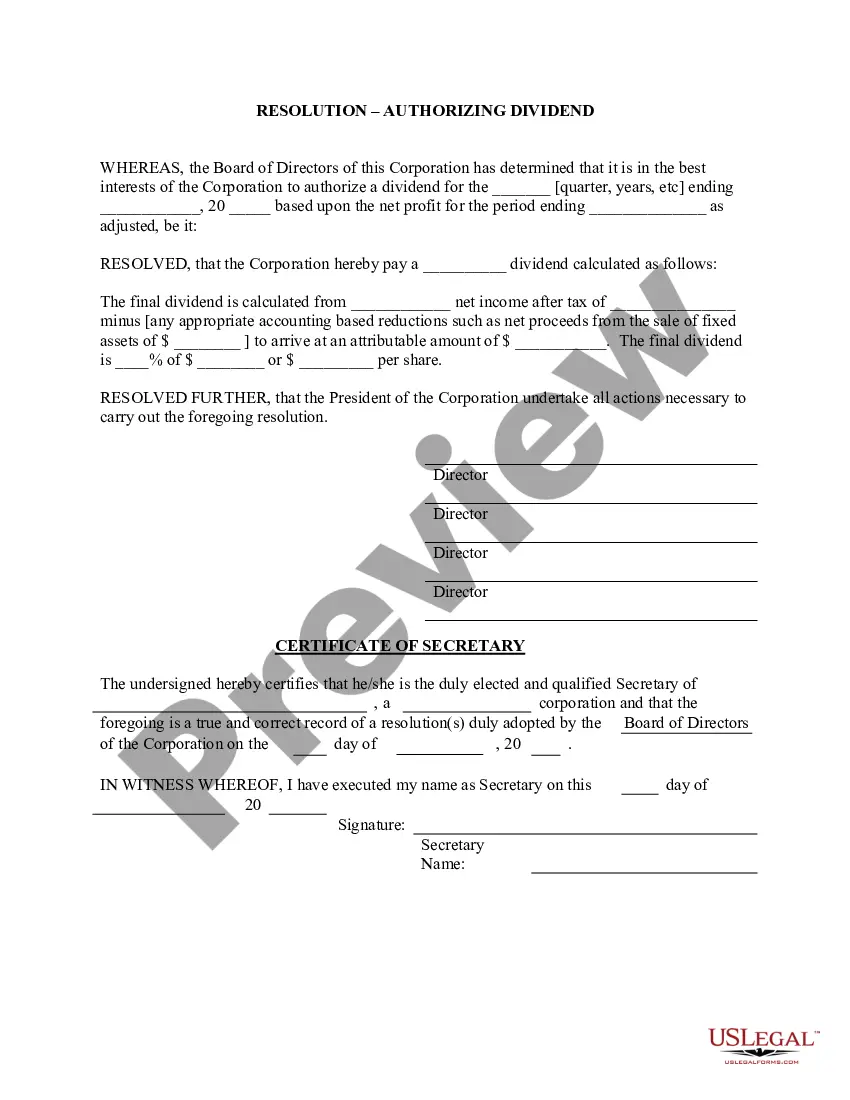

Dividend Corporation Shareholder Foreign

Description

How to fill out Dividend Policy - Resolution Form - Corporate Resolutions?

Drafting legal paperwork from scratch can often be a little overwhelming. Some cases might involve hours of research and hundreds of dollars spent. If you’re looking for a an easier and more affordable way of creating Dividend Corporation Shareholder Foreign or any other forms without jumping through hoops, US Legal Forms is always at your fingertips.

Our virtual collection of more than 85,000 up-to-date legal forms covers almost every aspect of your financial, legal, and personal affairs. With just a few clicks, you can quickly get state- and county-compliant forms diligently put together for you by our legal experts.

Use our platform whenever you need a trustworthy and reliable services through which you can quickly find and download the Dividend Corporation Shareholder Foreign. If you’re not new to our website and have previously created an account with us, simply log in to your account, select the template and download it away or re-download it at any time in the My Forms tab.

Not registered yet? No worries. It takes minutes to register it and explore the library. But before jumping directly to downloading Dividend Corporation Shareholder Foreign, follow these tips:

- Review the document preview and descriptions to make sure you are on the the form you are searching for.

- Check if form you select complies with the regulations and laws of your state and county.

- Pick the best-suited subscription option to purchase the Dividend Corporation Shareholder Foreign.

- Download the file. Then complete, sign, and print it out.

US Legal Forms has a good reputation and over 25 years of experience. Join us now and transform document execution into something simple and streamlined!

Form popularity

FAQ

Dividends are considered ?qualified? if they meet the following requirements: The dividends must have been paid by a U.S. corporation or a qualified foreign corporation. Investors must adhere to a minimum holding period.

A dividend paid by a U.S. corporation to a foreign shareholder is usually subject to a withholding tax. The amount of the withholding tax depends on whether the United States has tax treaties with the foreign shareholder's country, and on how much of the U.S. corporation the foreign shareholder owns.

In order to be considered ?qualified?, dividends received must meet three conditions: The dividends must have been paid by a U.S. corporation or a qualified foreign corporation. The dividends are not of those listed under ?Dividends that are not qualified dividends?. The holding period requirement is met.

Dividend received from a foreign company is taxable. It will be charged to tax under the head ?income from other sources.? Dividends received from a foreign company will be included in the total income of the taxpayer and will be charged to tax at the rates applicable to the taxpayer.

At the top of page F2 of the supplementay form SA106, the columns are marked 'A' Country or teritory code, 'B' Amount of income arising or received before any tax taken off and 'C' Foreign tax taken off or paid. Under the section for dividends from foreign companies, you would show the entries for A, B and C.